Вам также может понравиться

- CK Food Link Calendar Summer 2012Документ2 страницыCK Food Link Calendar Summer 2012krobinetОценок пока нет

- Kentucky at The Thames 1813Документ17 страницKentucky at The Thames 1813krobinetОценок пока нет

- A Cultural Plan For Chatham-KentДокумент56 страницA Cultural Plan For Chatham-KentkrobinetОценок пока нет

- Transcom 2011 FinancesДокумент27 страницTranscom 2011 FinanceskrobinetОценок пока нет

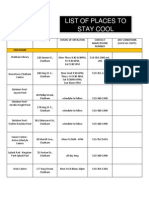

- Stay Cool Chatham-KentДокумент4 страницыStay Cool Chatham-KentkrobinetОценок пока нет

- CKHA Imagine 2Документ2 страницыCKHA Imagine 2krobinetОценок пока нет

- Chatham-Kent Transportation Master PlanДокумент83 страницыChatham-Kent Transportation Master PlankrobinetОценок пока нет

- John D. Bradley Convention CentreДокумент4 страницыJohn D. Bradley Convention CentrekrobinetОценок пока нет

- CK Housing Study Update 2012Документ218 страницCK Housing Study Update 2012krobinetОценок пока нет

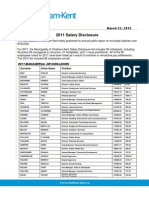

- Chatham-Kent Salary Disclosures 2011Документ12 страницChatham-Kent Salary Disclosures 2011krobinetОценок пока нет

- Transfer of Capitol Theatre To St. Clair CollegeДокумент17 страницTransfer of Capitol Theatre To St. Clair CollegekrobinetОценок пока нет

- Chatham Cultural Centre Master PlanДокумент128 страницChatham Cultural Centre Master PlankrobinetОценок пока нет

- Chatham-Kent Parks & Rec PlanДокумент19 страницChatham-Kent Parks & Rec PlankrobinetОценок пока нет

- Chatham-Kent 2012 Service Reduction OptionsДокумент4 страницыChatham-Kent 2012 Service Reduction OptionskrobinetОценок пока нет

- CK Transit Service Review 2011Документ98 страницCK Transit Service Review 2011krobinetОценок пока нет

- CK 2010 Audited FinancialsДокумент39 страницCK 2010 Audited FinancialskrobinetОценок пока нет

- Ckha !imagineДокумент4 страницыCkha !imaginekrobinetОценок пока нет

- CK Heritage Act DesignationsДокумент45 страницCK Heritage Act DesignationskrobinetОценок пока нет

- CK Tecumseh MonumentДокумент22 страницыCK Tecumseh MonumentkrobinetОценок пока нет

- GPO Platform: It's TimeДокумент16 страницGPO Platform: It's Timemthornton4590Оценок пока нет

- Chatham CondoДокумент1 страницаChatham CondokrobinetОценок пока нет

- Change That Puts People FirstДокумент48 страницChange That Puts People FirstontarionewdemocratОценок пока нет

- Navistar Announces Chatham ClosureДокумент2 страницыNavistar Announces Chatham ClosurekrobinetОценок пока нет

- The Ontario Liberal Plan 2011-2015Документ60 страницThe Ontario Liberal Plan 2011-2015OntarioLiberalPartyОценок пока нет

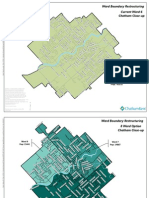

- Proposed Chatham-Kent Ward ChangesДокумент3 страницыProposed Chatham-Kent Ward ChangeskrobinetОценок пока нет

- CK Community Governance Task Force Final ReportДокумент40 страницCK Community Governance Task Force Final ReportkrobinetОценок пока нет

- PCPO (Progressive Conservative Party of Ontario) (Changebook) Platform, Election 2011Документ44 страницыPCPO (Progressive Conservative Party of Ontario) (Changebook) Platform, Election 2011Melonie A. FullickОценок пока нет

- Capitol Theatre Q&AДокумент4 страницыCapitol Theatre Q&AkrobinetОценок пока нет

- Capitol Theatre Audit FormatДокумент3 страницыCapitol Theatre Audit FormatkrobinetОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- HSM OffshoreДокумент2 страницыHSM OffshorePrabhakar TiwariОценок пока нет

- Assignment 3Документ6 страницAssignment 3salebanОценок пока нет

- Kees BerendsДокумент5 страницKees BerendsJavier LopezОценок пока нет

- MST For Road CuttingДокумент13 страницMST For Road CuttinginbОценок пока нет

- LF-50-205 (Bar Chair) - Shop DrawingДокумент2 страницыLF-50-205 (Bar Chair) - Shop DrawingAgung SetiawanОценок пока нет

- BSc (Hons) Quantity Surveying Construction Management RolesДокумент8 страницBSc (Hons) Quantity Surveying Construction Management RolesKusal HettiarachchiОценок пока нет

- PROJECT DELIVERY METHODS - Case Study PDFДокумент6 страницPROJECT DELIVERY METHODS - Case Study PDFRexy SusantoОценок пока нет

- Project Management for Construction: Understanding the Owners' PerspectiveДокумент21 страницаProject Management for Construction: Understanding the Owners' PerspectivePrem Kumar DharmarajОценок пока нет

- LCS: Bedell Law Firm ReportДокумент248 страницLCS: Bedell Law Firm ReportdocuristОценок пока нет

- Bre586 Construction ITДокумент2 страницыBre586 Construction ITjasminetsoОценок пока нет

- HB Construction CoordinatorsДокумент31 страницаHB Construction CoordinatorsespinozcristianОценок пока нет

- Iare Construction Management Lecture NotesДокумент51 страницаIare Construction Management Lecture Notescoolvin4uОценок пока нет

- Ce Laws - Section-1Документ13 страницCe Laws - Section-1Kai de LeonОценок пока нет

- CM 310A Syllabus and Schedule Ver. AДокумент4 страницыCM 310A Syllabus and Schedule Ver. AgarrettdjamesОценок пока нет

- 22-Execution Plan-Epc-250 MW Power PlantДокумент28 страниц22-Execution Plan-Epc-250 MW Power PlantP Eng Suraj Singh100% (1)

- Axonometric and Oblique ProjectionДокумент4 страницыAxonometric and Oblique ProjectionUsama TahirОценок пока нет

- Construction Project Management Lecture NotesДокумент257 страницConstruction Project Management Lecture NotesIllyanna Fox100% (9)

- 5.2 Scope of Work & Tie-In Point - NewДокумент14 страниц5.2 Scope of Work & Tie-In Point - Newandrieysyah2525Оценок пока нет

- Hendrickson BookДокумент314 страницHendrickson BookSoenarto SoendjajaОценок пока нет

- Planning in ConstructionДокумент25 страницPlanning in ConstructionAdan Ceballos MiovichОценок пока нет

- Support For CRC & CPL Building PDFДокумент32 страницыSupport For CRC & CPL Building PDFhungОценок пока нет

- Building Industry ComponentsДокумент22 страницыBuilding Industry ComponentsJoshua OmolewaОценок пока нет

- Final Report MOU ContractДокумент50 страницFinal Report MOU Contractsumanshailendra0% (1)

- Construction Quality Control Manager in Baltimore MD Resume Mary Kathleen WilsonДокумент3 страницыConstruction Quality Control Manager in Baltimore MD Resume Mary Kathleen WilsonMaryKathleenWilsonОценок пока нет

- Method Statement For CW INTAKE SCREEN WASH WATER SYSTEM FLUSHING BL.1 5 PDFДокумент8 страницMethod Statement For CW INTAKE SCREEN WASH WATER SYSTEM FLUSHING BL.1 5 PDFFredie UnabiaОценок пока нет

- Ivy Belchez Architectural Services ScopeДокумент6 страницIvy Belchez Architectural Services ScopeIVYMARIE BELCHEZОценок пока нет

- Nolasco Builders Company ProfileДокумент52 страницыNolasco Builders Company ProfilePatricia SahagunОценок пока нет

- Construction Contracts DocuementsДокумент48 страницConstruction Contracts DocuementsChristian AntonioОценок пока нет

- Procurement Mthds AssignmentДокумент16 страницProcurement Mthds AssignmentEkwubiri Chidozie100% (2)

- Project Organization and ManagementДокумент12 страницProject Organization and ManagementJ. VinceОценок пока нет