Академический Документы

Профессиональный Документы

Культура Документы

2 Final Body

Загружено:

sabujymailИсходное описание:

Авторское право

Доступные форматы

Поделиться этим документом

Поделиться или встроить документ

Этот документ был вам полезен?

Это неприемлемый материал?

Пожаловаться на этот документАвторское право:

Доступные форматы

2 Final Body

Загружено:

sabujymailАвторское право:

Доступные форматы

Chapter: 1 Introduction

1.1 Origin of the Report: The report entitled Grameen Bank-A Bank for Landless People is prepared which is mandatory requirement MBA Program under East West University, which aims to reflect the professional view of the real world. 1.2 Objective of the Report: The objective of this report is to know about the various activities and services provided by the Grameen Bank to landless people to fight against the poverty and development of socio economic condition of the poor, who have been keeping outside the banking sector. To know about the Grameen Banks mission, vision and their contribution in national economy. 1.3 Scope of the Report: This report is mainly focuses on the Grameen Bank-A Bank of Landless People in the context of Bangladesh. The propose study covers different aspect of the Grameen Bank activities and social responsibilities. As Bangladesh is a least developing country the role of Grameen Bank is most essential for developing the landless people. 1.4 Historical Background: The origin of Grameen Bank can be traced back to 1976 when Professor Muhammad Yunus, Head of the Rural Economics Program at the University of Chittagong, launched an action research project to examine the possibility of designing a credit delivery system to provide banking services targeted at the rural poor. The Grameen Bank Project (Grameen means "rural" or "village" in Bangla language) came into operation with the following objectives: 1. Extend banking facilities to poor men and women; 2. Eliminate the exploitation of the poor by money lenders; 3. Create opportunities for self-employment for the vast multitude of unemployed people in rural Bangladesh;

Page 1 of 35

4. Bring the disadvantaged, mostly the women from the poorest households, within the fold of an organizational format which they can understand and manage by themselves; and 5. Reverse the age-old vicious circle of "low income, low saving & low investment", into virtuous circle of "low income, injection of credit, investment, more income, more savings, more investment, more income".

1.5 Grameen Bank's Mission Grameen Bank claims to be different from conventional banks in that it provides loans to the poor, who are otherwise seen as not credit-worthy. It is believed that those who are poverty stricken around the world have vast untapped potent ional for innovation and productivity if only given the resources to work. And this entrepreneurship can lift a person, family and society up from poverty and into a self-sufficient, productive work-force. Additionally, Grameen promotes establishing women as the financial hub of society. According to Grameen, women have been proven to be the more responsible members of society and, therefore, a greater tool for development.

1.6 Decision of Grameen Bank: 1. We shall follow and advance the four principles of Grameen Bank --- Discipline, Unity, Courage and Hard work in all walks of out lives 2. Prosperity we shall bring to our families

3. 3.0 We shall not live in dilapidated houses. We shall repair our houses and work towards constructing new houses at the earliest 4. We shall grow vegetables all the year round. We shall eat plenty of them and sell the surplus 5. During the plantation seasons, we shall plant as many seedlings as possible 6. We shall plan to keep our families small. We shall minimize our expenditures. We shall look after our health 7. We shall educate our children and ensure that they can earn to pay for their education 8. We shall always keep our children and the environment clean 9. We shall build and use pit-latrines

Page 2 of 35

10. We shall drink water from tubewells. If it is not available, we shall boil water or use alum 11. We shall not take any dowry at our sons' weddings, neither shall we give any dowry at our daughters wedding. We shall keep our centre free from the curse of dowry. We shall not practice child marriage 12. We shall not inflict any injustice on anyone, neither shall we allow anyone to do so 13. We shall collectively undertake bigger investments for higher incomes 14. We shall always be ready to help each other. If anyone is in difficulty, we shall all help him or her 15. If we come to know of any breach of discipline in any centre, we shall all go there and help restore discipline 16. We shall take part in all social activities collectively

1.7 Indicators of Grameen Bank Every year GB staffs evaluate their work and check whether the socio-economic situation of GB members is improving. GB evaluates poverty level of the borrowers using ten indicators. A member is considered to have moved out of poverty if her family fulfills the following criteria: 1. The family lives in a house worth at least Tk. 25,000 (twenty five thousand) or a house with a tin roof, and each member of the family is able to sleep on bed instead of on the floor. 2. Family members drink pure water of tube-wells, boiled water or water purified by using alum, arsenic-free, purifying tablets or pitcher filters. 3. All children in the family over six years of age are all going to school or finished primary school. 4. Minimum weekly loan installment of the borrower is Tk. 200 or more. 5. Family uses sanitary latrine. 6. Family members have adequate clothing for every day use, warm clothing for winter, such as shawls, sweaters, blankets, etc, and mosquito-nets to protect themselves from mosquitoes. 7. Family has sources of additional income, such as vegetable garden, fruit-bearing trees, etc, so that they are able to fall back on these sources of income when they need additional money. 8. The borrower maintains an average annual balance of Tk. 5,000 in her savings accounts. 9. Family experiences no difficulty in having three square meals a day throughout the year, i. e. Page 3 of 35

no member of the family goes hungry any time of the year. 10. Family can take care of the health. If any member of the family falls ill, family can afford to take all necessary steps to seek adequate healthcare.

1.8 Essential Features of the Savings and Loan Delivery System 1 Exclusive Focus on the Poorest of the Poor 2 Borrowers Organized into Small Homogenous Groups 3 Loan Conditions Specially Tailored for the Poor 4 Undertaking Social Development Programs to Address Basic Needs of the Poor 5 Designs and Development of a Credit Conducive Organization and Management System Capable of Servicing the Poor 6 Expansion of the Loan Portfolio to Meet Diverse Development Needs of the Poor 7 Strategic Market Orientated Credit Policies 8 The Organizational Structures and Functions

1.9 Methodology: This report was created by accumulating data from various sources. Namely, books, websites and annual reports. The books and websites were used for the presentation of financial instruments related information. Annual reports were used for institute profiles and content analysis.

Page 4 of 35

Chapter 2: An overview of Grameen Bank

2.1 Introduction Grameen Bank (GB) has reversed conventional banking practice by removing the need for collateral and created a banking system based on mutual trust, accountability, participation and creativity. GB provides credit to the poorest of the poor in rural Bangladesh, without any collateral. At GB, credit is a cost effective weapon to fight poverty and it serves as a catalyst in the over all development of socio-economic conditions of the poor who have been kept outside the banking orbit on the ground that they are poor and hence not bankable. Professor Muhammad Yunus, the founder of "Grameen Bank" and its Managing Director, reasoned that if financial resources can be made available to the poor people on terms and conditions that are appropriate and reasonable, "these millions of small people with their millions of small pursuits can add up to create the biggest development wonder." As of October, 2011, it has 8.349 million borrowers, 97 percent of whom are women. With 2,565 branches, GB provides services in 81,379 villages, covering more than 97 percent of the total villages in Bangladesh. Grameen Bank's positive impact on its poor and formerly poor borrowers has been documented in many independent studies carried out by external agencies including the World Bank, the International Food Research Policy Institute (IFPRI) and the Bangladesh Institute of Development Studies (BIDS).

2.2 Brief History of Grameen Bank:

The action research demonstrated its strength in Jobra (a village adjacent to Chittagong University) and some of the neighboring villages during 1976-1979. With the sponsorship of the central bank of the country and support of the nationalized commercial banks, the project was extended to Tangail district (a district north of Dhaka, the capital city of Bangladesh) in 1979. With the success in Tangail, the project was extended to several other districts in the country. In October 1983, the Grameen Bank Project was transformed into an independent bank by government legislation. Today Grameen Bank is owned by the rural poor whom it serves. Borrowers of the Bank own 90% of its shares, while the remaining 10% is owned by the government.

Page 5 of 35

2.3 Founder of the Grameen Bank: Professor Muhammad Yunus is the founder and Managing Director of Grameen Bank which currently operates 2,564 branches providing credit to 8.29 million poor people residing in 81,367 villages in Bangladesh. He originated the concept of Grameen Bank, i.e. banking without collateral for the poorest of the poor. Professor Yunus studied economics in the Vanderbilt University, USA and received his Ph.D. in Economics in 1970. He taught economics in the Middle Tennessee University from 1969 to 1972. Returning to Bangladesh in 1972, he joined the University of Chittagong as Head of the Economics Department. He started the Grameen Bank Project in 1976. It was transformed into a formal bank in 1983. The Grameen Bank offers small loans for self employment for the rural poor, especially poor women. 2.4 Biography of Dr. Muhammad Yunus Muhammad Yunus was born in 28th June, 1940 in the village of Bathua, in Hathazari, Chittagong, the business centre of what was then Eastern Bengal. He was the third of 14 children of whom five died in infancy. His father was a successful goldsmith who always encouraged his sons to seek higher education. But his biggest influence was his mother, Sufia Khatun, who always helped any poor that knocked on their door. This inspired him to commit himself to eradication of poverty. His early childhood years were spent in the village. In 1947, his family moved to the city of Chittagong, where his father had the jewelery business.

In 1974, Professor Muhammad Yunus, a Bangladeshi economist from Chittagong University, led his students on a field trip to a poor village. They interviewed a woman who made bamboo stools, and learnt that she had to borrow the equivalent of 15p to buy raw bamboo for each stool made. After repaying the middleman, sometimes at rates as high as 10% a week, she was left with a penny profit margin. Had she been able to borrow at more advantageous rates, she would have been able to amass an economic cushion and raise herself above subsistence level.

Realizing that there must be something terribly wrong with the economics he was teaching, Yunus took matters into his own hands, and from his own pocket lent the equivalent of ? 17 to 42 basketweavers. He found that it was possible with this tiny amount not only to help them survive, but also to create the spark of personal initiative and enterprise necessary to pull themselves out of poverty.

Page 6 of 35

Against the advice of banks and government, Yunus carried on giving out 'micro-loans', and in 1983 formed the Grameen Bank, meaning 'village bank' founded on principles of trust and solidarity. In Bangladesh today, Grameen has 2,564 branches, with 19,800 staff serving 8.29 million borrowers in 81,367 villages. On any working day Grameen collects an average of $1.5 million in weekly installments. Of the borrowers, 97% are women and over 97% of the loans are paid back, a recovery rate higher than any other banking system. Grameen methods are applied in projects in 58 countries, including the US, Canada, France, The Netherlands and Norway. 2.5 What is Microcredit ? The word "micro credit" did not exist before the seventies. Now it has become a buzz-word among the development practitioners. In the process, the word has been imputed to mean everything to everybody. No one now gets shocked if somebody uses the term "micro credit" to mean agricultural credit, or rural credit, or cooperative credit, or consumer credit, credit from the savings and loan associations, or from credit unions, or from money lenders. When someone claims micro credit has a thousand year history, or a hundred year history, nobody finds it as an exciting piece of historical information. I think this is creating a lot of misunderstanding and confusion in the discussion about micro credit. We really don't know who is talking about what. I am proposing that we put labels to various types of micro credit so that we can clarify at the beginning of our discussion which micro credit we are talking about. This is very important for arriving at clear conclusions, formulating right policies, designing appropriate institutions and methodologies. Instead of just saying "micro credit" we should specify which category of micro credit. A broad classification of micro credit : A) Traditional informal micro credit (such as, moneylender's credit, pawn shops, loans from friends and relatives, consumer credit in informal market, etc.) B) Micro credit based on traditional informal groups (such as, tontin, su su, ROSCA, etc.) C) Activity-based micro credit through conventional or specialized banks (such as, agricultural credit, livestock credit, fisheries credit, handloom credit, etc.) D) Rural credit through specialized banks. E) Cooperative micro credit (cooperative credit, credit union, savings and loan associations, savings Page 7 of 35

banks, etc.) F) Consumer micro credit. G) Bank-NGO partnership based micro credit. H) Grameen type micro credit or Grameen credit. I) Other types of NGO micro credit. J) Other types of non-NGO non-collateralized micro credit. This is a very quick attempt at classification of micro credit just to make a point. The point is? Every time we use the word "micro credit" we should make it clear which type (or cluster of types) of micro credit we are talking about. Otherwise we'll continue to create endless confusion in our discussion. Needless to say that the classification I have suggested is only tentative. We can refine this to allow better understanding and better policy decisions. Classification can also be made in the context of the issue under discussion. I am arguing that we must discontinue using the term "micro credit" or "microfinance" without identifying its category. Micro credit data are compiled and published by different organizations. We find them useful. I propose that while publishing these data we identify the category or categories of micro credit each organization provides. Then we can prepare another set of important information? Number of poor borrowers, and their gender composition, loan disbursed, loan outstanding, balance of savings, etc. under each of these categories, countrywide, regionwise, and globally. These sets of information will tell us which category of micro credit is serving how many poor borrowers, their gender break-up, their growth during a year or a period, loans disbursed, loans outstanding, savings, etc. The categories which are doing better, more support can go in their direction. The categories which are doing poorly may be helped to improve their performance. For policy-maters this will be enormously helpful. I urge Microcredit Summit Campaign secretariat to present the information that they already collect on number of clients, number of the poorest among them, number of poorest clients that are women, number of clients that have crossed the poverty line? broken down for each of the categories of micro credit. This will help donors to select the categories they would like to support. This sorting out is very important for the donors, as well as the policymakers.

Page 8 of 35

2.6 Grameen credit Whenever I use the word "micro credit" I actually have in mind Grameen type microcredit or Grameen credit. But if the person I am talking to understands it as some other category of micro credit my arguments will not make any sense to him. Let me list below the distinguishing features of Grameen credit. This is an exhaustive list of such features. Not every Grameen type programme has all these features present in the programme. Some programmes are strong in some of the features, while others are strong in some other features. But on the whole they display a general convergence to some basic features on the basis of which they introduce themselves as Grameen replication programmes or Grameen type programmes.

General features of Grameencredit are : a) It promotes credit as a human right. b) Its mission is to help the poor families to help themselves to overcome poverty. It is targeted to the poor, particularly poor women. c) Most distinctive feature of Grameencredit is that it is not based on any collateral, or legally enforceable contracts. It is based on "trust", not on legal procedures and system. d) It is offered for creating self-employment for income-generating activities and housing for the poor, as opposed to consumption. e) It was initiated as a challenge to the conventional banking which rejected the poor by classifying them to be "not creditworthy". As a result it rejected the basic methodology of the conventional banking and created its own methodology. f) It provides service at the door-step of the poor based on the principle that the people should not go to the bank, bank should go to the people. g) In order to obtain loans a borrower must join a group of borrowers. h) Loans can be received in a continuous sequence. New loan becomes available to a borrower if her previous loan is repaid.

Page 9 of 35

i) All loans are to be paid back in installments (weekly, or bi-weekly). j) Simultaneously more than one loan can be received by a borrower. k) It comes with both obligatory and voluntary savings programmes for the borrowers. l) Generally these loans are given through non-profit organizations or through institutions owned primarily by the borrowers. If it is done through for-profit institutions not owned by the borrowers, efforts are made to keep the interest rate at a level which is close to a level commensurate with sustainability of the programme rather than bringing attractive return for the investors. Grameencredit's thumb-rule is to keep the interest rate as close to the market rate, prevailing in the commercial banking sector, as possible, without sacrificing sustain-ability. In fixing the interest rate market interest rate is taken as the reference rate, rather than the moneylenders' rate. Reaching the poor is its non-negotiable mission. Reaching sustainability is a directional goal. It must reach sustainability as soon as possible, so that it can expand its outreach without fund constraints. Grameen credit is based on the premise that the poor have skills which remain unutilized or underutilized. It is definitely not the lack of skills which make poor people poor. Grameen believes that the poverty is not created by the poor, it is created by the institutions and policies which surround them. In order to eliminate poverty all we need to do is to make appropriate changes in the institutions and policies, and/or create new ones. Grameen believes that charity is not an answer to poverty. It only helps poverty to continue. It creates dependency and takes away individual's initiative to break through the wall of poverty. Unleashing of energy and creativity in each human being is the answer to poverty. Grameen brought credit to the poor, women, the illiterate, the people who pleaded that they did not know how to invest money and earn an income. Grameen created a methodology and an institution around the financial needs of the poor, and created access to credit on reasonable term enabling the poor to build on their existing skill to earn a better income in each cycle of loans. If donors can frame category wise micro credit policies they may overcome some of their discomforts. General policy for micro credit in its wider sense is bound to be devoid of focus and sharpness.

Page 10 of 35

2.7 Owner of the Bank: 2.7.1 Owned by the Poor Grameen Bank Project was born in the village of Jobra, Bangladesh, in 1976. In 1983 it was transformed into a formal bank under a special law passed for its creation. It is owned by the poor borrowers of the bank who are mostly women. It works exclusively for them. Borrowers of Grameen Bank at present own 95 percent of the total equity of the bank. Remaining 5 per cent is owned by the government. Beggars as Members i. Existing rules of Grameen Bank do not apply to beggar members; they make up their own rules.

ii. All loans are interest-free. Loans can be for very long term, to make repayment installments very small. For example, for a loan to buy a quilt or a mosquito-net, or an umbrella, many borrowers are paying Tk 2.00 (3.4 cents US) per week. iii. Beggar members are covered under life insurance and loan insurance programmes without paying any cost. iv. Groups and centers are encouraged to become patrons of the beggar members. v. Each member receives an identity badge with Grameen Bank logo. She can display this as she goes about her daily life, to let everybody know that she is a Grameen Bank member and this national institution stands behind her. vi. Members are not required to give up begging, but are encouraged to take up an additional income-generating activity like selling popular consumer items door to door, or at the place of begging. vii. Objective of the programme is to provide financial services to the beggars to help them find a dignified livelihood send their children to school and graduate into becoming regular Grameen Bank members. We wish to make sure that no one in the Grameen Bank villages has to beg for survival.

Page 11 of 35

Chapter Three Grameen Bank at a Glance

3.1.0 Nobel Peace Prize, 2006 October 13, 2006 was the happiest day for Bangladesh. It was a great moment for the whole nation. Announcement came on that day that Grameen Bank and I received the Nobel Peace Prize, 2006. It was a sudden explosion of pride and joy for every Bangladeshi. All Bangladeshi's felt as if each of them received the Nobel Peace Prize. We were happy that the world has given recognition through this prize, that poverty is a threat to peace. Grameen Bank, and the concept and methodology of micro-credit that it has elaborated through its 30 years of work, have contributed to enhancing the chances of peace by reducing poverty. Bangladesh is happy that it could contribute to the world a concept and an institution which can help bring peace to the world.

Following is a brief introduction to Grameen Bank. 3.2.0 Owned by the Poor Grameen Bank Project was born in the village of Jobra, Bangladesh, in 1976. In 1983 it was transformed into a formal bank under a special law passed for its creation. It is owned by the poor borrowers of the bank who are mostly women. It works exclusively for them. Borrowers of Grameen Bank at present own 95 percent of the total equity of the bank. Remaining 5 per cent is owned by the government. 3.3.0 No Collateral, No Legal Instrument, No Group-Guarantee or Joint Liability Grameen Bank does not require any collateral against its micro-loans. Since the bank does not wish to take any borrower to the court of law in case of non-repayment, it does not require the borrowers to sign any legal instrument. Although each borrower must belong to a five-member group, the group is not required to give any guarantee for a loan to its member. Repayment responsibility solely rests on the individual borrower, while the group and the centre oversee that everyone behaves in a responsible way and none gets into repayment problem. There is no form of joint liability, i.e. group members are not responsible to pay on behalf of a defaulting member.

Page 12 of 35

3.4.0

97 per cent Women Total number of borrowers is 8.35 million, 96 per cent of them are women.

3.5.0

Branches Grameen Bank has 2,565 branches. It works in 81,379 villages. Total staff is 22,124

3.6.0

Over Tk 684 billion Disbursed Total amount of loan disbursed by Grameen Bank, since inception, is Tk 684.13 billion (US $ 11.35 billion). Out of this, Tk 610.81 billion (US $ 10.11 billion) has been repaid. Current amount of outstanding loans stands at TK 73.32 billion ( US $ 968.31 million). During the past 12 months ( from November10 to October'11) Grameen Bank disbursed Tk. 107.30 billion (US $ 1480.53 million). Monthly average loan disbursement over the past 12 month was Tk 8.94 billion (US $ 123.38 million). Projected disbursement for year 2011 is Tk 110.00 billion (US$ 1557.63 million), i.e. monthly disbursement of Tk 9.17 billion (US $ 129.80 million). End of the year outstanding loan is projected to be at Tk. 78.00 billion (US $ 1105 million).

3.7.0

Recovery Rate Over 97 per cent Loan recovery rate is 96.67 per cent.

3.8.0

100 per cent Loans Financed From Banks Deposits Grameen Bank finances 100 per cent of its outstanding loan from its deposits. Over 56 per cent of its deposits come from banks own borrowers. Deposits amount to 145 per cent of the outstanding loans. If we combine both deposits and own resources it becomes 160 per cent of loans outstanding.

3.9.0

Borrower-Deposits Keep Growing Besides building financial strength of the poor women by encouraging them to build up significant amount of personal savings, borrower deposit is also a very important element in Grameen Bank. Forty-two per cent of the branches have borrower deposits equal to 75 per cent or more of outstanding loans of the branches. One-fifth of the branches have more borrower-deposits than the amount of loans outstanding. In some branches borrower-deposits are as high as 50 per cent above the

Page 13 of 35

outstanding loans. In eight zones, out of forty, borrower deposits are equal or more than the outstanding loans in zones. 3.10.0 No Donor Money, No Loans In 1995, GB decided not to receive any more donor funds. Since then, it has not requested any fresh funds from donors. Last installment of donor fund, which was in the pipeline, was received in 1998. GB does not see any need to take any donor money or even take loans from local or external sources in future. GB's growing amount of deposits will be more than enough to run and expand its credit programme and repay its existing loans. 3.11.0 Earns Profit Ever since Grameen Bank came into being, it has made profit every year except in 1983, 1991, and 1992. It has published its audited balance-sheet every year, audited by two internationally reputed audit firms of the country. All these reports are available on CD, and some on our web-site : www.grameen.com. 3.12.0 Revenue and Expenditure Total revenue generated by Grameen Bank in 2010 was Tk 17.74 billion (US $ 252.05 million). Total expenditure was Tk 16.98 billion (US $ 241.29 million). Interest payment on deposits of Tk 9.23 billion (US $ 131.09 million) was the largest component of expenditure (54 per cent). Expenditure on salary, allowances, pension benefits amounted to TK. 4.64 billion (US $ 65.92 million), which was the second largest component of the total expenditure (27 per cent). Grameen Bank made a profit of Tk 757.24 million (US $ 10.76 million) in 2010. 3.13.0 30% Dividend for 2010 Grameen Bank has declared 30% cash dividend for the year 2010. This is the highest cash dividend declared by any bank in Bangladesh in 2010.Highest record of dividend declared by Grameen Bank was in 2006.It was 100%.The bank has also created a Dividend Equalization Fund to ensure distribution of dividends without much fluctuation in successive years .Receiving of dividends each year greatly inspires our shareholders, 97% of whom are our borrowers.

Page 14 of 35

3.14.0 Low Interest Rates Government of Bangladesh has fixed interest rate for government-run microcredit programmes at 11 per cent at flat rate. It amounts to about 22 per cent at declining basis. Grameen Bank's interest rate is lower than governmentrate. Recently MRA has fixed the maximum interest rate for microcredit at 27% on declining balance method and instructed the NGO-MFIs to implement this capped interest rate within June 2011.MRA found in a recent survey the effective interest rate of NGO-MFIs on General Loan ranges from 25% to 33% and the modal value is 29%.On the contrary Grameen Bank's highest interest rate is 20%. Microfinance Transparency an internationally reputed pricing certification agency also verified the pricing of Grameen Bank loan products and found that GB actually charges the same interest as it publicly claims. There are four interest rates for loans from Grameen Bank : 20% for income generating loans, 8% for housingloans, 5% for student loans, and 0% (interest-free) loans for Struggling Members (beggars). All interests are simple interest, calculated on declining balance method. This means, if a borrower takes an income-generating loan of say, Tk 1,000, and pays back the entire amount within a year in weekly instalments, she'll pay a total amount of Tk 1,100, i.e. Tk 1,000 as principal, plus Tk 100 as interest for the year, equivalent to 10% flat rate. 3.15.0 Deposit Rates Grameen Bank offers very attractive rates for deposits. Minimum interest offered is 8.5 per cent. Maximum rate is 12 per cent. 3.16.0 Beggars As Members Begging is the last resort for survival for a poor person, unless he/she turns into crime or other forms of illegal activities. Among the beggars there are disabled, blind, and retarded people, as well as old people with ill health. Grameen Bank has taken up a special programme in 2002, called Struggling Members Programme exclusively for the beggars. Over 111,296 beggars have joined the programme. Total amount disbursed stands today at Tk. 162.60 million. Of this amount of Tk. 130.89 million (80% of the amount disbursed) has Page 15 of 35

already been paid off. 19,678 beggars have left begging and are making a living as door-to-door sales persons. Among them 10,185 beggars have joined Grameen Bank groups as main-stream borrowers. Beggers members have voluntarily opened their personal savings accounts. Cumulative deposit in these savings accounts amounts to BDT 22.41 million; present balance stands at BDT 8.08 million. Basic features of the programme are : 1) Existing rules of Grameen Bank do not apply to beggar members; they make up their own rules.

2)

All loans are interest-free. Loans can be for very long term, to make repayment instalments very small. For example, for a loan to buy a quilt or a mosquito-net, or an umbrella, many borrowers are paying Tk 2.00 (3.4 cents US) per week.

3) Beggar members are covered under life insurance and loan insurance programmes without paying any cost.

4) Groups and centres are encouraged to become patrons of the beggar members.

5) Each member receives an identity badge with Grameen Bank logo. She can display this as she goes about her daily life, to let everybody know that she is a Grameen Bank member and this national institution stands behind her.

6) Members are not required to give up begging, but are encouraged to take up an additional income-generating activity like selling popular consumer items door to door, or at the place of begging. Objective of the programme is to provide financial services to the beggars to help them find a dignified livelihood, send their children to school and graduate into becoming regular Grameen Bank members. We wish to make sure that no one in the Grameen Bank villages has to beg for survival.

Page 16 of 35

3.17.0 Housing For the Poor Grameen Bank introduced housing loan in 1984. It became a very attractive programme for the borrowers. This programme was awarded Aga Khan International Award for Architecture in 1989. Maximum amount given for housing loan is Tk 25,000 (US $ 354) to be repaid over a period of 5 years in weekly instalments. Interest rate is 8 per cent. 690,737 houses have been constructed with the housing loans averaging Tk 13,059 (US $ 181.50). A total amount of Tk 9.02 billion (US $ 211.21 million) has been disbursed for housing loans. During the past 12 months (from Nov.'10 to October11) 4,482 houses have been built with housing loans amounting to Tk 52.43 million (US $ 0.69 million). 3.18.0 Micro-enterprise Loans Many borrowers are moving ahead in businesses faster than others for many favourable reasons,such as, proximity to the market, presence of experienced male members in the family, etc. Grameen Bank provides larger loans, called micro-enterprise loans, for these fast moving members. There is no restriction on the loan size. So far 3,590923 members took micro-enterprise loans. A total of Tk 105.96 billion(US$ 1540.58 million) has been disbursed under this category of loans. Average loan size is Tk 29,507 (US $ 389.69), maximum loan taken so far is Tk 1.6 million (US $ 23,209). This was used in purchasing a truck which is operated by the husband of the borrower. Power-tiller, irrigation pump, transport vehicle, and river-craft for transportation and fishing are popular items for micro-enterprise loans. 3.19.0 Scholarships Scholarships are given, every year, to the high performing children of Grameen borrowers, with priority on girl children, to encourage them to stay ahead to their classes. Upto October'11, scholarships amounting to Tk 205.03 million (US$ 3.00 million) have been awarded to 1,33031 children. During 2011, US$ 592,849 will be awarded to about 24,611 children, at various levels of school and college education. 3.20.0 Education Loans Students who succeed in reaching the tertiary level of education are given higher education loans, covering tuition, maintenance, and other school expenses. By October11, 49,588 students received higher education loans, of them 46,885 students are studying at various universities; 577 are studying in medical schools, 894 are studying to become engineers, 1232 are studying in other professional institutions.

Page 17 of 35

3.21.0 Grameen Network Grameen Bank does not own any share of the following companies in the Grameen network. Nor has it given any loan or received any loan from any of these companies. They are all independent companies, registered under Companies Act of Bangladesh, with obligation to pay all taxes and duties, just like any other company in the country. 1) Grameen Phone Ltd. 2) Grameen Telecom 3) Grameen Communications 4) Grameen Cybernet Ltd. 5) Grameen Solutions Ltd. 6) Grameen Information Highways Ltd. 7) Grameen Bitek Ltd. 8) Grameen Krishi Foundation 9) Grameen Motsho (Fisheries) Foundation 10) Grameen Uddog (Enterprise) 11) Grameen Shamogree (Products) 12) Grameen Knitwear Ltd. 13) Grameen Shikkha (Education) 14) Grameen Capital Management Ltd. 15) Grameen Byabosa Bikash (Business Promotion ) 16) Grameen Trust 17) Grameen Health Care Trust 18) Grameen Health Care Service Ltd. 19) Grameen Danone Food Ltd. 20) Grameen Veolia Water Ltd. 21) Grameen Shakti. 22) Grameen IT Park Ltd. 23) Grameen Star Education Ltd. 24) Grameen Employment Services Ltd. 25) Grameen Fabrics and Fashion Ltd. 26) Grameen Distribution Ltd. 27) Grameen Shamogree Purbanchal Ltd. 28) Grameen Shamogree Uttaranchal Ltd.

Page 18 of 35

29) BASF Grameen Ltd. 30) Grameen Fund: Inherited Social Venture Capital Fund (SVCF) that was created in Grameen Bank as a donor funded project. Subsequently money in the fund was given as loan to Grameen Fund, an independently created not-for-profit company,with the consent of the donors. Grameen Fund continues to function as a social venture fund. 31) Grameen Kalyan: Grameen Kalyan (Well-being) is a not for profit company registered under the Companies Act 1994. Grameen Bank created an internal fund called Social Advancement Fund (SAF) by imputing interest on all the grant money it received from various donors. Money accumulated in SAF was given to Grameen Kalyan to manage a project of undertaking social advancement activities among the Grameen borrowers, such as, education, health, technology, etc. Not only Grameen Kalyan is implementing the project, it has also ensured growth of the initial fund by several times, and expanding the coverage of the social advancement activities for Grameen borrowers.

3.22.0 Loans Paid Off At Death Grameen offers an optional insurance programme called Loan Insurance Programme. Those who sign up for this programme in case of their death , all outstanding loans are paid off. Under this programme, an insurance fund is created by the interest generated in a savings account created by deposits of the borrowers made for loan insurance purpose, at the time of receiving loans. Each time an amount equal to 3 per cent of the loan amount is deposited in this account. This amount is transferred from the Special Savings account. If the current balance in the insurance savings account is equal or more than the 3 per cent of the loan amount, the borrower does not need to add any more money in this account. If it is less than 3 per cent of the loan amount, she has to deposit enough money to make it equal. Total deposits in the loan insurance savings account stood at Tk 7,000.17 million (US$ 93.77 million) as on October 31, 2011. Up to that date 217,907 insured borrowers and insured husbands died and a total outstanding loans and interest of Tk 2022.00 million (US $ 29.53 million) left behind was paid off by the bank under the programme. The families of the deceased borrowers are not be required to pay off their debt burden any more, because the insured borrowers or their insured husbands do not leave behind any debt burden to take care of.

Page 19 of 35

3.23.0 Life Insurance Each year families of deceased borrowers of Grameen Bank receive a total of Tk 17 to 20 million (US $ 0.25 million to 0.29 million) in life insurance benefits. Each family receives Tk 1,500. A total of 137,976 borrowers died so far in Grameen Bank. Their families collectively received a total amount of Tk 241.34 million (US$ 4.74 million). Borrowers are not required to pay any premium for this life insurance. Borrowers come under this insurance coverage by being a shareholder of the bank. 3.24.0 Deposits By the end of October, 2011 total deposit in Grameen Bank stood at Tk. 105.95 billion (US$ 1399.30 million). Member deposit constituted 56 per cent of the total deposits. Balance of member deposits has increased at a monthly average rate of 1.42 percent during the last 12 months. 3.25.0 Pension Fund for Borrowers Another optional, but enormously popular programme in Pension Fund Programme.As borrowers grow older they worry about what will happen to them when they cannot work and earn any more. Grameen Bank addressed that issue by introducing a programme of creating a Pension Fund for old age. It immediately became a very popular programme. Under this programme a borrower is required to save a small amount, such as Tk 50 (US $ 0.66), each month over a period of 10 years. The depositor gets almost twice the amount of money she saved, at the end of the period. The borrowers find it very attractive. By the end of October 2011 the balance under this account comes to a total of Tk 38.87 billion (US $ 513.28 million). Tk 6.28 billion (US $ 86.61 million) was added during the past 12 months (November10-October, 2011). We expect the balance in this account to grow by Tk 6.65 billion (US $ 94.17 million) in 2011 making the balance to reach Tk 44.56 billion (US $ 631.04 million).

Page 20 of 35

3.26.0 Loan Loss Reserve Grameen Bank has a very rigourous policy on bad debt provisioning. If a loan does not get paid back on time it is converted into a special type of loan called "Flexible Loan", and 50 per cent provisioning is done on the last day of each month. Hundred per cent provisioning is done when flexible loan completes the second year. At its third year, the outstanding amount is completely written off even if the loan repayment still continues. Balance in the loan loss reserve stood at Tk 5.40 billion (US $ 76.70 million) at the end of 2010 after writing off an amount of Tk 1.22 billion (US $ 17.37 million) during 2010. Out of the total amount written off in the past an amount of Tk 0.58 billion (US $ 8.24 million) has been recovered during 2010. 3.27.0 Retirement Benefits Paid Out Grameen Bank has an attractive retirement policy. Any staff can retire after completing ten years or more of service. At the time of retirement he receives a retirement benefit in cash. It is usually paid out within a month after retirement. Since this benefit was introduced 8,857 staff members retired and received a total amount of Tk 7.09 billion (US $ 113.94 million) in cash. This amounts to Tk 0.80 million (US $ 12864) per retiring staff. During the past 12 months 689 staffs went on retirement collecting a retirement benefit of Tk 1287.16 million (US $ 17.75 million). Average retirement benefit per staff was Tk 1.87 million (US $ 25,752 ). 3.28.0 Telephone-Ladies To-date Grameen Bank has provided loans to 457953 borrowers to buy mobile phones and offer telecommunication services in nearly half of the villages of Bangladesh where this service never existed before. Telephone-ladies run a very profitable business with these phones. Telephone-ladies play an important role in the telecommunication sector of the country, and also in generating revenue for Grameen Phone, the largest telephone company in the country. Telephone ladies use 2.22 percent of the total air-time of the company, while their number is only 1.89 per cent of the total number of telephone subscribers of the company.

Page 21 of 35

3.29.0 Getting Elected in Local Bodies Grameen system makes the borrowers familiar with election process. They routinely go through electing group chairmen and secretaries, centre-chiefs and deputy centre-chiefs every year. They elect board members for running Grameen Bank every three years. This experience has prepared them to run for public offices. They are contesting and getting elected in the local governments. In 2011 local government (Union Porishad) election got elected 13 Chairman out of 4,498 candidates. In the reserved seats for women 3,473 members got elected out of 13,494 candidates. They constitute 26 per cent of the total members elected in the seats reserved for women members in the Union Porishad local government.During 2003 and 1997 local government election 3,059 and 1,753 members respectively got elected to these reserved seats. 3.30.0 Computerised MIS and Accounting System Accounting and information management of nearly all the branches (2,565 out of 2,565) has computerised. This has freed the branch staff to devote more time to the borrowers rather than spend it in paper-work. Branch staffs are provided with pre-printed repayment figures for each weekly meeting. If every borrower pays according to the repayment schedule, the staff has nothing to write on the document except for putting the signature. Only the deviations are recorded. Paper work that remains to be done at the village level is to enter figures in the borrowers' passbooks. All zones (40) are connected with the head office, and with each other, through intra-net. This has made data transfer and communications very easy. 3.31.0 Policy For Opening New Branches New branches are required to fund themselves entirely with the deposits they moblise. No fund from head office or any other office is lent to them. A new branch is expected to breakeven within the first year of its operation. 3.32.0 Crossing the Poverty-Line According to a recent internal survey, 68 per cent of Grameen borrowers' families of Grameen borrowers have crossed the poverty line. The remaining families are moving steadily towards the poverty line from below.

Page 22 of 35

3.33.0 'Stars' for Achievements Grameen Bank provides colour-coded stars to branches and staff for 100 percent achievement of a specific task. A branch (or a staff) having five-stars indicate the highest level of performance. At the end of June'2011, branches showed the following result. 929 branches, out of total 2,565 branches, received stars (green) for maintaining 100 per cent repayment record. 19,93 branches received stars (blue) for earning profit. (Grameen Bank as a whole earns profit because the total profit of the profit-earning branches exceeds the total loss of the loss-incurring branches.) 1,869 branches earned stars (violet) by meeting all their financing out of their earned income and deposits. These branches not only carry out their business with their own funds, but also contribute their surpluses to meet the fund requirement of deficit branches. 324 branches have applied for stars (brown) for ensuring education for 100% of the children of Grameen families. After the completion of the verification processes their stars will be confirmed. 65 branches have applied for stars (red) indicating branches those have succeeded in taking all its borrowers' families (usually 3,000 families per branch) over the poverty line. The star will be confirmed only after the verification procedure is completed. Each month branches are coming closer to achieving new stars. Grameen staff look forward to transforming all the branches of Grameen Bank into five star branches.

Page 23 of 35

Chapter Four Allied Concern of Grameen Bank

4.1 Allied Concern of Grameen Bank: Inspired by the work of Grameen Bank in Bangladesh, Grameen Foundation was created to accelerate the impact of microfinance on the worlds poorest people, especially women. Started in 1976 by Professor Muhammad Yunus with a mere $27, Grameen Bank now serves more than 7 million poor families with loans, savings, insurance and other services. The bank is fully owned by its clients and has been a model for microfinance institutions around the world. In 2006, Professor Yunus and Grameen Bank jointly received the Nobel Peace Prize. President Barack Obama awarded Professor Yunus the 2009 Presidential Medal of Freedom. Although we are independent organizations, Grameen Foundation and Grameen Bank maintain an enduring relationship. Grameen Foundation President Alex Counts trained under and worked closely with Professor Yunus during his six-year tenure in Bangladesh. Professor Yunus was a founding member of Grameen Foundations board of directors and currently serves as director emeritus. Grameen Foundation seeks to further the Grameen Bank legacy and objectives by supporting microfinance institutions and poverty-fighting organizations that embody its vision and values on a global scale. The allied concerns of Grameen Banks are as follows:

4.1.1 Grameen Trust

As a result of the success of Grameen Bank in reaching and serving the poor with credit, many people and organizations began to think in Grameen's way, and wanted to learn more about Grameen and follow Grameen's principles in their own sphere of work. It is primarily to meet this demand that the Grameen Trust (GT) came into being in 1989.

Page 24 of 35

The program goals are: 1. Create an option for a begging-free honorable life for a beggar through interest and collateral free flexible term microcredit. 2. Provide basic literacy and mentoring to the struggling members. 3. Provide peer support to the struggling members. 4. Through Innovation Dialogue programs harness information about the field level challenges and innovative solutions for creating opportunities for the beggars. 5. Compile the collective wisdom of the Innovations Dialogue to disseminate within the partner network for adaptation and replication. 4.1.2 Grameen Communications:

Grameen Communications, a member of Grameen family of enterprises, is a not for profit Information Technology company. It has been providing complete systems solution through developing software products and services, internet services, hardware & networking services and IT education services since its inception in 1997 under the Companies Act, 1994. 4.1.3 Grameen America

Grameen America is a microfinance company whose mission is to help alleviate poverty through entrepreneurship. It provides financial services, such as loans, savings programs and a pathway to establish credit to the working poor, especially women, in the United States.

4.1.4 Grameen Crdit Agricole Foundation

Page 25 of 35

The Grameen Crdit Agricole Foundation offers a combination of financial support and technical assistance to microfinance institutions and "social business" enterprises and projects. It mobilizes human and financial resources to poorest. 4.1.5 Grameen Kalyan

Grameen Kalyan provides affordable health care services to the rural poor in Bangladesh. They currently operate 30 health clinics in different parts of rural Bangladesh. 4.1.6 Grameen Shakti

Grameen Shakti promotes, develops and popularizes renewable energy technologies in rural areas of Bangladesh. Having served more than 2 million people since inception, Grameen Shakti is one of the largest and fastest growing renewable energy technology programs in the world. 4.1.7 Grameen Shikkha

Grameen Shikkha is a company in the family of Grameen companies. Established in 1997 its main objectives are to promote mass education in rural areas, provide financial support in the form of loans and grants for the purpose of education, use IT for alleviation of illiteracy and evelopment of education, promote new technologies and innovate ideas and methods for development of education etc. Grameen Shikkha has been conducting Life Oriented Education Program, Preschool/Child Development Program, Early Childhood Development Program and Arsenic Mitigation Program in various districts of Bangladesh.

Page 26 of 35

4.1.8 Grameen Fund Grameen Fund was incorporated on January 17, 1994 as a "not-for-profit" company and started operations on February 1, 1994. Its emphasis is on providing finance to ventures that are risky, technology - oriented and otherwise deprived of financing from existing formal lending institutions. 4.1.9 Grameen Telecom Grameen Telecom is a company dedicated to bringing the information revolution to the rural people of Bangladesh. Grameen Telecom is planning, over the next 4 years, to provide GSM 900/1100 cellular mobile phone service to 100 million rural inhabitants in 68,000 villages of Bangladesh by (1) financing 60,000 members of Grameen Bank to provide village pay phone service and (2) providing direct phones to potential subscribers. 4.1.10Grameen Cyber Net Grameen Cybernet Ltd. has been Bangladesh's leader in Internet service provision since it commenced operation in July 1996. Its Chief Executive has had an extensive career in education and information technology in the US and is assisted by a team of bright, young executives

4.1.11 Grameen Phone In the fast-paced world of telecommunications, vibrant and dynamic Corporate Governance practices are an essential ingredient to success. Grameenphone believes in the continued improvement of corporate governance. This in turn has led the Company to commit considerable resources and implement internationally accepted Corporate Standards in its day-to-day operations 4.1.12 Grameen Knitwear Limited Grameen Knitwear Limited: The company is a 100% export oriented composite knitwear factory, located in the Export Processing Zone in Savar in the vicinity of Dhaka, the capital of Bangladesh. It has knitting, dyeing, finishing and garments production facilities. Most of the machinery and equipment have been sourced from Europe. The factory is capable to produce very high quality of different knit fabrics and garments of children, men and women. The fabrics and garments are fabric and yarn dyed 100% cotton, TC, CVC, Polyester with lycra attachement etc of various counts. The countries where the goods are currently exported are mostly Europe. The goods are exported against confirmed irrevocable letter of credit.

Page 27 of 35

4.1.13 Grameen Solutions Grameen Solutions, a flagship technology company within Grameen family of organizations. Founded by Dr. Muhammad Yunus, recipient of 2006 Nobel Peace Prize, Grameen Solutions offers business services, management consulting, software development, business process and service outsourcing. Grameen Solutions offers unparallel total value through creative solutions that meet the diverse and dynamic needs of our global and local client base 4.1.14 Grameen Byabosa Bikash Grameen Byabosa Bikash (GBB) is one of the sister organizations in the Grameen family of enterprises. The English meaning of this name is Grameen Business Promotion and Services. GBB is a social business and not-for-profit organization registered under the Companies Act 1994 of Peoples Republic of Bangladesh Government. It started operation in 2001 with its registered office located at the Grameen Bank Complex at Mirpur area of Dhaka city. GBB has a board consisting of 8 members. The Board is headed by nobel laureate Professor Muhammad Yunus. The other Board members are also renowned in their respective field. The Board sits at least every four months to assess the progress of the organization.

Page 28 of 35

Chapter Five Summary of Grameen Bank

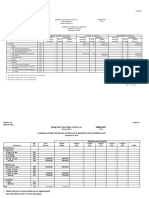

Balance Sheet 2003-2010 (As on December 31), Amount in Million Taka Property and Assets Cash in hand Balance with other Banks Investment Loans and Advances Fixed assets-(at cost less accumulated depreciation) Investment property (at cost less accumulated depreciation) Other assets Total: Capital and Liabilities Share Capital: Authorized Paid Up General and Other reserves Revolving Funds Deposits and Other Funds Borrowings from banks and foreign institutions Other Liabilities Profit and loss account Total: Contigent Liabilities 2007 2008 2009 2010 6,799,759 3,798,731 1,119,488 895,544 929,598,021 1,324,659,716 1,295,311,555 1,310,692,097 24,465,809,686 28,730,304,221 37,750,731,641 47,757,186,897 37,546,479,706 45,786,957,884 56,359,028,995 68,417,977,923 1,114,517,485 4,890,494,100 1,163,268,845 5,791,712,934 1,222,283,438 111,558,215 6,265,224,923 1,379,656,418 108,540,014 6,422,009,079

68,953,698,757 82,800,702,331 103,005,258,255 125,396,957,972

500,000,000 3,500,000,000 3,500,000,000 3,500,000,000 318,000,000 358,000,000 523,949,300 547,689,200 5,547,882,878 6,078,437,278 6,219,533,668 6,815,290,863 55,640,755,203 68,314,322,203 87,286,490,709 109,206,727,710 1,793,276,465 1,731,218,532 1,669,160,600 1,589,027,602

5,653,784,211 6,318,724,318 7,306,123,978 7,238,222,597 68,953,698,757 82,800,702,331 103,005,258,255 125,396,957,972 5,719,054 -

Page 29 of 35

Chapter Six Strength & weakness Recommendation & Conclusion

6.1 Weakness Theres not much research done on the actual effectiveness of microfinance as a tool for economic growth. Some argue that theres to much focus on microfinance which will motivating less spending in other helping assistances as public health, welfare, and education. Some are doubting microfinance really have those impacts on poverty as the practioners would submit. Other describes microcrediting as a privatization of public safety net programs. There are also some microfinance institutions charging excessive interest rates. Questions against the Grameen Bank were raised in a Wall Street Journal article. It was regarding the repayment rate, collection methods and questionable accounting practices. Studies of microcredit programs have found that women often act as collection agents for their husbands and sons, such that the men spend the money themselves while women are saddled with the credit risk. Some borrowers have become dependent on loans for household expenditures rather than capital investments. The key debate about microfinance is weather it should focus on improved welfare or financial sustainability. The two different approaches are usually named as poverty lending or the welfares approach and the institutions approach or financial system approach. The welfares approach could be for example supplying the customer with education and health wilts the institutions focus only on the financial service. The reason for that is only with total focus on financial sustainability the huge demand can be met. MFIs with the welfares approach are for example the Grameen Bank and Womens World Banking. Examples of institutions are ACCION International and BRI Unit Desa.

Page 30 of 35

6.2 Main Strengths 1. Banking for the Poor 2. Empowerment 3. Easy replication 4. Going beyond Donor Assistance 5. A Common Praxis 6.3 General Recommendations & conclusion The policy recommendations that follow draw on the innovative institutional arrangements, practices and policies designed within the Co-operative Banking Model and the Grameen Bank Model. There are five main recommendations: (1) Specific Institutional Recommendations 1.1 The Midrand Council consider establishing a Savings and Credit Co-operative (SACCO) in the Greater Midrand area with the following objectives and institutional tiers : Objectives Harness local community savings in order to provide the poor with access to credit; Establish a financial backbone to sustain and develop the local co-operative movement; Ensure local economic development is financed to meet the needs of the poor in an ecologically sustainable manner. The Board of Directors Sets overall policy for the co-operative; employs managerial staff; Establishes an Education Committee and a Credit Committee; has formalized representation from the Council and at least two co-operatives operating in the community; Ensures regular auditing.

Page 31 of 35

Supervisory Committee Monitors the operation of the Board; Ensures regular audits are carried out.

Management Centre Provides technical back-up and training to branches; Has regular meetings with branches to receive reports on operations; Provides business planning facilities to co-operatives and other clients of the SACCO; Plans and develops projections for the expansion of the SACCO; Makes policy recommendations and provides reports to the Board of Directors; Sits on the SACCO Credit Committee; Sources outside expertise when necessary; Employs staff for the branches; Manages the IT of the SACCO and ensures proper linkages with even commercial banks to acquire benefits of ATM technology of possible. Produces publication; Liases with SACCOL.

(2)The Savings and Loan Delivery System The savings and loan delivery system envisaged should be member driven and based on the twin objective of building up a stable savings portfolio that contributes to self sufficiency and a loan system that balances meeting the needs of members and ensuring the financial self sufficiency of the co-operative, as well. It is proposed that the following conceptual framework be considered for the design of a savings and loan delivery system : 2.1 Membership The common bond for membership is the fact of living in the common area of the Greater Midrand; Every member pays a once of joining fee (that is not refundable) and buys a share for a certain sum of money. A member should be able to buy more than one share but not more than ten, for which they would receive a dividend once the co-operative begins to produce a surplus. All members, irrespective of the number of shares they own would be entitled to only one vote;

Page 32 of 35

Membership shall be opened to co-operatives, community organisations and even local government itself; Members will be entitled to vote for the Board of Directors and can have a say on policy matters; Every member is entitled to a monthly financial statement Members can only utilise the services of the co-operative once they are organised into a Savings and Credit Team of 7 people, living in their immediate area. The Savings and Credit team would monitor compulsory savings by meeting twice a month and would also monitor loan repayment;

Every member should receive a smart card that would enable withdrawals and balance statements to be obtained at any ATM, as well as branches of the SACCO.

2.2 Savings and Investment Policy Savings can happen through payroll deductions, stop order and direct cash deposits; Savings must be compulsory for all members and monthly minima must be agreed to for employed and unemployed members. The Savings and Credit Teams must monitor compulsory savings of members, using the monthly financial statements they would receive; At least 80% of savings received, equity finance and other reserves of the SACCO must be invested; 10% must be saved with the CFC of SACCOL; Savings products both fixed, annual like X-mas savings and open account must receive commercial rates of return that are not below inflation; The savings and depositor base of the SACCO must be constantly expanded to even include a host of organizations including the local council, other co operatives, trade unions and community organizations. 2.3 Loans Policy Loans must only happen through Savings and Credit Teams and only three out of the seven members in the team will get loans first. Based on successful repayment, loans will be extended to other members and even obtained for other purposes; Loan products have to be decided and should initially have a mix of productive, consumption and development products. A special loan product for co-operatives must be developed, either for start-up or expansion, and this has to be linked to proper business planning;

Page 33 of 35

Loans should only be given out once the SACCO has achieved financial self sufficiency through its savings policy. The percentage of assets given out as loans initially has to be prudent and well managed;

(3)Technology The Smart Card The feasibility of providing members with a plastic smart card must be explored with SACCOL. The extent to which it can be harmonised with the current ATM banking infrastructure has to also be explored. If the CUBIS system, used by SACCOL, allows for this then this technology can be used for the following purposes : Easy withdrawals, even through the ATM system, in Midrand and any other place; Controlling of withdrawals by placing a withdrawal limit if there is a loan taken out by the particular member. This technology also opens up the prospect of experimenting with a complimentary currency. (4) The Public - Community Partnership The idea of Savings and Credit Co-operative for Midrand can only work if there is Widespread support. To achieve this the Council must secure a public and community partnership for the Midrand SACCO. The main focus of the partnership is to bring the poor and women into this initiative that are unemployed or are poor working class and self employed. The public and community partnership should be launched at a workshop which achieves the following: A declaration that clearly defines the objectives of the SACCO, the benefits to members and responsibilities of the parties associated with this initiative; constitutes a community liason task group that would participate in the capacitating process; Launches a recruitment program for members; and Clarifies and kicks of the capacitating process.

Page 34 of 35

(5) The Capacitating Agents and the Capacitating Process Consideration must be given to establishing a capacitating team that includes COPAC, SACCOL and FSA. The capacitating process that this team will manage will include the following: Finalizing and clarifying the Concept envisaged for the SACCO; Work shopping the liaison team to secure statutes, bye laws, business plan and policies; Training of prospective staff; Forming and registering the co-operative once recruitment is at a critical level; Setting up a pilot branch of the SACCO.

Page 35 of 35

Appendix 1. http://www.microfinanceinfo.com/category/microcredit/ 2. http://dspace.nitle.org/handle/10090/11722 3. http://copac.org.za/publications/comparative-study-cooperative-banks-and-grameen-bankmodel 4. http://www.grameenfoundation.org/ 5. Grameen Bank | Bank for the poor - GB At a Glance 6. Grameen Trust 7. Grameen Families Organizations

8. Our Impact of Grameen Foundation 9. What We Do about Grameen Foundation

Page 36 of 35

Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- A PROJECT REPORT ON HDFC BANK Submiited by Ankita SinghДокумент29 страницA PROJECT REPORT ON HDFC BANK Submiited by Ankita SinghBHRIGURASHAN 16588% (94)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Source of Wealth - NETELLERДокумент2 страницыSource of Wealth - NETELLERTahsin Ove100% (1)

- Sme1st Reso MaybankДокумент9 страницSme1st Reso MaybankAhmad HazwanОценок пока нет

- 2007 Resume Book TuckДокумент92 страницы2007 Resume Book TuckKang-Li Cheng100% (3)

- Optimize Cash Flow With Electronic PaymentsДокумент22 страницыOptimize Cash Flow With Electronic Paymentshendraxyzxyz100% (1)

- Questionnaire For BankДокумент5 страницQuestionnaire For BankRajendra Patidar100% (1)

- Dep LiabДокумент6 страницDep LiabMary Ann PacariemОценок пока нет

- IFN Guide 2019 PDFДокумент104 страницыIFN Guide 2019 PDFPastel IkasyaОценок пока нет

- Tenders 20 11122018carshed PDFДокумент63 страницыTenders 20 11122018carshed PDFMihirОценок пока нет

- Automotive components survey BangladeshДокумент103 страницыAutomotive components survey Bangladeshjony_nsu022Оценок пока нет

- Bill PPPPPДокумент6 страницBill PPPPPsnelu1178Оценок пока нет

- Global Finance - Introduction AДокумент268 страницGlobal Finance - Introduction AfirebirdshockwaveОценок пока нет

- Your Strawman (Legal Fiction)Документ31 страницаYour Strawman (Legal Fiction)Karl_23100% (4)

- Procedure On Financing of Two-Wheeler Loan at Centurian Bank by Sneha SalgaonkarДокумент57 страницProcedure On Financing of Two-Wheeler Loan at Centurian Bank by Sneha SalgaonkarAarti Kulkarni0% (2)

- Trade Finance: GuideДокумент36 страницTrade Finance: Guidesujitranair100% (1)

- Chapter 14Документ12 страницChapter 14Aditi SenОценок пока нет

- Important Simple Interest Practice Questions for Bank ExamsДокумент15 страницImportant Simple Interest Practice Questions for Bank ExamsKothapalli VinayОценок пока нет

- Form 3CBДокумент12 страницForm 3CBpriya sharmaОценок пока нет

- Types of Cyber CrimeДокумент22 страницыTypes of Cyber CrimeHina Aswani100% (1)

- Soal Test Corporate Law FirmДокумент4 страницыSoal Test Corporate Law FirmMerin Zuldani AlamОценок пока нет

- Courses Subject Codes 1. B.A. TAMIL (2008-2009) I YEARДокумент48 страницCourses Subject Codes 1. B.A. TAMIL (2008-2009) I YEARMAdhuОценок пока нет

- TyreXpo Data 2019-13-14th DecДокумент45 страницTyreXpo Data 2019-13-14th DecNeeraj KumarОценок пока нет

- Compensation Management System of Finca Micro Finance Bank BahawalpurДокумент8 страницCompensation Management System of Finca Micro Finance Bank BahawalpurMMohammadMohsinОценок пока нет

- FINA2001 PortfolioДокумент2 страницыFINA2001 PortfolioJoshОценок пока нет

- Sewale Bitew PDFДокумент84 страницыSewale Bitew PDFTILAHUNОценок пока нет

- Rural Bank Wins Case Against Central Bank Penalty ChargeДокумент1 страницаRural Bank Wins Case Against Central Bank Penalty ChargechatoОценок пока нет

- Credit RiskДокумент32 страницыCredit RiskDrNisa SОценок пока нет

- DH3050 Tenancy Assistance Application 03.21Документ16 страницDH3050 Tenancy Assistance Application 03.21Sarah VirziОценок пока нет

- Foundations of Financial Management Canadian 10th Edition Block Solutions Manual DownloadДокумент33 страницыFoundations of Financial Management Canadian 10th Edition Block Solutions Manual DownloadPeter Coffey100% (22)

- Online Banking Project FinalДокумент55 страницOnline Banking Project FinalSANTOSH GAIKWADОценок пока нет