Вам также может понравиться

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Intro to Macro Midterm Boot Camp Assignment 1 ReviewДокумент104 страницыIntro to Macro Midterm Boot Camp Assignment 1 Reviewmaged famОценок пока нет

- Future Cities Dubai ReportДокумент24 страницыFuture Cities Dubai ReportVictor RattanavongОценок пока нет

- R13 Currency Exchange Rates SlidesДокумент58 страницR13 Currency Exchange Rates SlidesRahul RawatОценок пока нет

- International Monetary SystemДокумент16 страницInternational Monetary Systemriyaskalpetta100% (2)

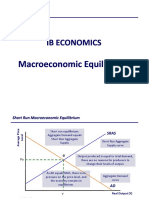

- IB MACRO EQUILIBRIUMДокумент13 страницIB MACRO EQUILIBRIUMPablo Torrecilla100% (1)

- 13 Steps For Investing (Motley Fool)Документ49 страниц13 Steps For Investing (Motley Fool)api-26637661Оценок пока нет

- Sustainability of Freight Forwarding FinДокумент49 страницSustainability of Freight Forwarding FinVictor Rattanavong0% (1)

- Sustainability of Freight Forwarding FinДокумент49 страницSustainability of Freight Forwarding FinVictor Rattanavong0% (1)

- 成語資料庫Документ165 страниц成語資料庫Victor RattanavongОценок пока нет

- AIIB Full Digital Infrastructure Report - Final With Appendix 2020-01-10Документ103 страницыAIIB Full Digital Infrastructure Report - Final With Appendix 2020-01-10Victor RattanavongОценок пока нет

- Chapter 8 Myfinancelab Solutions Pearsoncmgcom PDFДокумент89 страницChapter 8 Myfinancelab Solutions Pearsoncmgcom PDFChristopher Carpenter100% (7)

- Roland Berger Tab Digital Future of b2b Sales 1Документ16 страницRoland Berger Tab Digital Future of b2b Sales 1Abhishek KumarОценок пока нет

- ISEAS Perspective 2018 2@50Документ8 страницISEAS Perspective 2018 2@50Ayub PramudiaОценок пока нет

- Selection Process On TrackДокумент6 страницSelection Process On TrackVictor RattanavongОценок пока нет

- Global Middle Class 2030: 2.4 Billion 3.8 Billion 5.4 BillionДокумент12 страницGlobal Middle Class 2030: 2.4 Billion 3.8 Billion 5.4 BillionVictor RattanavongОценок пока нет

- Study On The High Speed Railway Project (Jakarta-Bandung Section), Republic of IndonesiaДокумент20 страницStudy On The High Speed Railway Project (Jakarta-Bandung Section), Republic of IndonesiaVictor RattanavongОценок пока нет

- Architecture Strategy of High Speed Railway Indonesia ChinaДокумент8 страницArchitecture Strategy of High Speed Railway Indonesia ChinaVictor RattanavongОценок пока нет

- Architecture Strategy of High Speed Railway Indonesia ChinaДокумент8 страницArchitecture Strategy of High Speed Railway Indonesia ChinaVictor RattanavongОценок пока нет

- Key Opportunities in ASEAN - Integration and Growth: Singapore's Chairmanship Thailand's ChairmanshipДокумент4 страницыKey Opportunities in ASEAN - Integration and Growth: Singapore's Chairmanship Thailand's ChairmanshipVictor RattanavongОценок пока нет

- Lao People's Democratic Republic Resource-Based Growth and Economic ChallengesДокумент3 страницыLao People's Democratic Republic Resource-Based Growth and Economic ChallengesVictor RattanavongОценок пока нет

- Chevron Annual Report SupplementДокумент64 страницыChevron Annual Report SupplementVictor RattanavongОценок пока нет

- Advanced Macroeconomics: An easy guideДокумент420 страницAdvanced Macroeconomics: An easy guideLucas OrdoñezОценок пока нет

- Hsslive XII Eco Macro ch2 National Income PDFДокумент7 страницHsslive XII Eco Macro ch2 National Income PDFIRSHAD KIZHISSERIОценок пока нет

- Monetary Policy: Based On "Macroeconomics" by Dornbusch and Fischer and "Elements of Economics" by TullaoДокумент12 страницMonetary Policy: Based On "Macroeconomics" by Dornbusch and Fischer and "Elements of Economics" by TullaoDiane UyОценок пока нет

- Programme Project Report (PPR) For Bachelor of CommerceДокумент48 страницProgramme Project Report (PPR) For Bachelor of CommerceshishirkantОценок пока нет

- Calculating National Income MethodsДокумент11 страницCalculating National Income MethodsJaivardhan KanoriaОценок пока нет

- International Parity Conditions You Can TrustДокумент51 страницаInternational Parity Conditions You Can Trustrohan100% (1)

- SA LIII 42 201018 Utsa PatnaikДокумент11 страницSA LIII 42 201018 Utsa PatnaikRaghubalan DurairajuОценок пока нет

- 9 General Structure of An Economic ParagraphДокумент2 страницы9 General Structure of An Economic ParagraphDilip PasariОценок пока нет

- Pros Cons: CapitalismДокумент5 страницPros Cons: CapitalismAlejandro Sanchez ArequipaОценок пока нет

- BS AssignmentДокумент4 страницыBS AssignmentRaufur RahmanОценок пока нет

- Santander - Brazil Fiscal Policy - Fiscal X-RayДокумент9 страницSantander - Brazil Fiscal Policy - Fiscal X-RayIgor EnnesОценок пока нет

- Diskusi 4 Bhs. Inggris Niaga ADBI4201 Chrisdianti 041153205Документ2 страницыDiskusi 4 Bhs. Inggris Niaga ADBI4201 Chrisdianti 041153205Lesley TrialОценок пока нет

- ECON 45- Theories of Economic DevelopmentДокумент9 страницECON 45- Theories of Economic DevelopmentVeronika MartinОценок пока нет

- Trade Policy in Developing CountriesДокумент26 страницTrade Policy in Developing CountriesAlice AungОценок пока нет

- Methodological Guide - Eurostat - OECD Developing Producer Price Indices For ServicesДокумент439 страницMethodological Guide - Eurostat - OECD Developing Producer Price Indices For ServicessandraexplicaОценок пока нет

- Engineering EconomicsДокумент60 страницEngineering EconomicsAbhineet GuptaОценок пока нет

- Vdocument - in - Project Report On Equity Research On Indian Banking SectorДокумент100 страницVdocument - in - Project Report On Equity Research On Indian Banking SectorNarendran BalarajuОценок пока нет

- Measures To Control InflationДокумент6 страницMeasures To Control InflationFeroz PashaОценок пока нет

- The Mundell-Fleming ModelДокумент3 страницыThe Mundell-Fleming ModelM31 Lubna AslamОценок пока нет

- Working Paper No. 792: From The State Theory of Money To Modern Money Theory: An Alternative To Economic OrthodoxyДокумент35 страницWorking Paper No. 792: From The State Theory of Money To Modern Money Theory: An Alternative To Economic OrthodoxyMATICAPEОценок пока нет

- Quiz 1 - SolutionsДокумент4 страницыQuiz 1 - Solutionsabijith taОценок пока нет

- International Monetary Arrangements For MBA, BBA, B.Com StudentsДокумент25 страницInternational Monetary Arrangements For MBA, BBA, B.Com StudentsRavishJiОценок пока нет

- CH 7Документ4 страницыCH 7Aryan RawatОценок пока нет

- UNIT IV - Performance of An Economy - MacroeconomicsДокумент50 страницUNIT IV - Performance of An Economy - MacroeconomicsSaravanan ShanmugamОценок пока нет

- Multinational Financial Management 10th Edition Shapiro Test Bank 1Документ7 страницMultinational Financial Management 10th Edition Shapiro Test Bank 1gerald100% (42)