Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Challan Format (Specialist)Документ1 страницаChallan Format (Specialist)hgfvhgОценок пока нет

- GFR FormsДокумент2 страницыGFR FormsSaurav GhoshОценок пока нет

- Consumer Price IndexДокумент20 страницConsumer Price IndexBritt John Ballentes0% (1)

- NISM-Series-VIII-Equity Derivatives Workbook (New Version September-2015)Документ162 страницыNISM-Series-VIII-Equity Derivatives Workbook (New Version September-2015)janardhanvn100% (3)

- Financial Management - PPT - 2011Документ183 страницыFinancial Management - PPT - 2011ashpika100% (1)

- Ultimate Reward Current Account GuideДокумент112 страницUltimate Reward Current Account GuideRyan BucuОценок пока нет

- Act1104midterm Exam Wit AnsДокумент9 страницAct1104midterm Exam Wit AnsDyen100% (1)

- Rural Finance and Micro FinanceДокумент32 страницыRural Finance and Micro FinanceThe Cultural CommitteeОценок пока нет

- UntitledДокумент6 страницUntitledB - Clores, Mark RyanОценок пока нет

- End of Season: Spring Summer 2021Документ29 страницEnd of Season: Spring Summer 2021Abdaud RasyidОценок пока нет

- KPMG Flash News Draft Guidelines For Core Investment CompaniesДокумент5 страницKPMG Flash News Draft Guidelines For Core Investment CompaniesmurthyeОценок пока нет

- Macroeconomics 2 ExamДокумент3 страницыMacroeconomics 2 ExamMWEBI OMBUI ERICK D193/15656/2018Оценок пока нет

- Honor Mobile Flyer 3419Документ2 страницыHonor Mobile Flyer 3419bilal asifОценок пока нет

- The Role of IPДокумент3 страницыThe Role of IPsamrat duttaОценок пока нет

- Statement of Cash FlowsДокумент13 страницStatement of Cash FlowsAldrin ZolinaОценок пока нет

- 2018 Working Capital Management: Test Code: R38 WCAM Q-BankДокумент6 страниц2018 Working Capital Management: Test Code: R38 WCAM Q-BankMarwa Abd-ElmeguidОценок пока нет

- Export Price List 2011-2012 SystemairДокумент312 страницExport Price List 2011-2012 SystemairCharly ColumbОценок пока нет

- Pennantpark Investment Corporation: PNNT - NasdaqДокумент8 страницPennantpark Investment Corporation: PNNT - NasdaqnicnicooОценок пока нет

- Chapter 2-GST Part B - Value of SupplyДокумент7 страницChapter 2-GST Part B - Value of SupplyPooja D AcharyaОценок пока нет

- Dividend Policy: by Group 5: Aayush Kumar Lewis Francis Jasneet Sai Venkat Ritika BhallaДокумент25 страницDividend Policy: by Group 5: Aayush Kumar Lewis Francis Jasneet Sai Venkat Ritika BhallaChristo SebastinОценок пока нет

- Sample MCQsДокумент6 страницSample MCQsRubal GargОценок пока нет

- Chapter 8: Cash and Bank Management Daily Procedures: ObjectivesДокумент26 страницChapter 8: Cash and Bank Management Daily Procedures: ObjectivesArturo GonzalezОценок пока нет

- New Signature Update FormДокумент3 страницыNew Signature Update FormKRIZMAL TRADING SOLUTIONS PVT LTDОценок пока нет

- Ticket Plus實名制購票流程 2023061301Документ14 страницTicket Plus實名制購票流程 2023061301daniel111478Оценок пока нет

- FCHN DisplayCheckRegisterДокумент3 страницыFCHN DisplayCheckRegisterSingh 10Оценок пока нет

- RatiosДокумент6 страницRatiosWindee CarriesОценок пока нет

- FIN 420 CASE STUDY Leverage RatioДокумент4 страницыFIN 420 CASE STUDY Leverage RatioNur AdibahОценок пока нет

- Pymnts Reinventing b2b Payments ReportДокумент27 страницPymnts Reinventing b2b Payments ReportTimmy O' CallaghanОценок пока нет

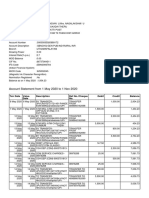

- Account Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент9 страницAccount Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChellapandiОценок пока нет

- FINA1904 - ALL Weitzel - Spring 2019Документ11 страницFINA1904 - ALL Weitzel - Spring 2019JamesОценок пока нет