Академический Документы

Профессиональный Документы

Культура Документы

Model Points

Загружено:

Rodrigo Torres GallegoИсходное описание:

Авторское право

Доступные форматы

Поделиться этим документом

Поделиться или встроить документ

Этот документ был вам полезен?

Это неприемлемый материал?

Пожаловаться на этот документАвторское право:

Доступные форматы

Model Points

Загружено:

Rodrigo Torres GallegoАвторское право:

Доступные форматы

Maastricht University

Faculty of Economics and

Business Administration

4

Model Points for

Asset Liability Models

June 28, 2008

Master thesis

Author

N.C. Jansen

i040010

Supervisors

Dr. J.J.B. de Swart (PwC)

Dr. F.J. Wille (PwC)

Prof. dr. ir. S. van Hoesel (UM)

Prof. dr. R.H.M.A. Kleynen (UM)

Abstract

ALM models are used by insurance companies as input to evaluate

their Solvency. They give rise to computational complexity because of

the number of policies and mainly the stochastic element. This stochastic

element denes the need for scenarios. Some insurance companies now use

data grouping methods to reduce run times, however these lack a theoret-

ical basis. In this paper we develop a theoretical framework to optimize

grouping strategies and to derive upper bounds for the inaccuracy caused

by grouping. We discuss determinants for the projected future cash ow

deviations, and as a result of those we try to bound the error resulting

from a certain grouping strategy. One of the main results in the paper is

the eect of linear data on the grouping strategy; we can simply group

them away. To make the method work in practice we rely on grid con-

struction, innity norms and numerical derivatives. We will furthermore

apply the method to a real life insurance product.

1

Contents

1 Introduction 3

2 Life insurances 5

2.1 ALM models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.2 Solvency II . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.3 Model Points . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

3 Framework for the model point generation 7

3.1 The problem in an Operations Research context . . . . . . . . . 7

3.2 Minimizing the error induced by making use of model points . . 8

3.3 Numerical model point creation . . . . . . . . . . . . . . . . . . . 11

3.3.1 Grid construction . . . . . . . . . . . . . . . . . . . . . . . 11

3.3.2 Determining the amount of buckets . . . . . . . . . . . . . 12

3.3.3 Creating the model points . . . . . . . . . . . . . . . . . . 12

3.3.4 Assigning the policies to the model points . . . . . . . . . 13

3.3.5 Estimating the errors . . . . . . . . . . . . . . . . . . . . 13

4 A real life example 14

4.1 Describing the product . . . . . . . . . . . . . . . . . . . . . . . . 14

4.2 Selecting the attributes . . . . . . . . . . . . . . . . . . . . . . . 14

4.3 Exploring the function . . . . . . . . . . . . . . . . . . . . . . . . 15

4.4 Interpreting the function . . . . . . . . . . . . . . . . . . . . . . . 16

4.5 Generating model points . . . . . . . . . . . . . . . . . . . . . . . 17

4.6 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

4.6.1 Grouping . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

4.6.2 Approximate deviation from the base run . . . . . . . . . 19

5 Conclusion and future work 20

A Appendix 22

A.1 Gridconstruction . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

A.2 Notations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

A.3 Figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

A.4 Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

2

1 Introduction

Insurance companies have gained increasing interest for Economic Capital, which

is used for making the optimal economic decisions, risk based pricing and perfor-

mance management. In addition, regulators are further developing their capital

requirement regulations in the appearance of Solvency II, with which insurers

need to comply to stay in business. Insurance companies use Asset Liability

models to project their future cash ows as input for evaluating their solvency

position.

Insurers have a portfolio of policies with dierent attributes and dierent

scenarios that can occur. To make a projection of their expected cash ows

they need to calculate for every scenario/policy combination the present value.

These projections can take an enormous amount of time given current process-

ing power. This is so much so that they needed to invent more sophisticated

techniques to tackle this problem. Multiple options exist to deal with the prob-

lem, and generally it is not the case that one option alone will solve the problem.

The options are:

Replicating portfolios

Software optimization

Scenario optimization

Grid technology

Model Points

Replicating portfolios has found usage in the nancial industry to value

cash ows that are not actively traded, such as insurance products. Investing

in a replicating portfolio will however not eliminate all risk, but this risk is

non-systematic and can therefore be diversied away. The market value of the

replicating portfolio is then used to determine the value of the liability cash

ow.

Optimizing the software so that it runs faster could be done, however since

most companies use certied products such as MoSes it is not our goal to beat

these well known software products.

Scenario optimization is performed by carefully selecting a subset of a large

set of scenarios, which is still accurately predicting future events. In this paper

we assume that this has already taken place.

Grid technology is a method where they spread the calculation burden for

ALM models across a grid of computers. Run times can be reduced by approxi-

mately the number of processors available. However, the drawback is that extra

hardware costs money and in addition the processors cannot concurrently be

used for other purposes.

The following observation makes data reduction methods very powerful. Pro-

jecting the future cash ows takes a lot of time, however the model that com-

putes them still runs in polynomial time. This means that we can decrease

3

the input size and achieve a great reduction in the time needed to calculate

the present values. By using model points, which is the technique that we will

present in this paper, we try to minimize the input size while still being accurate

within some bounds.

Insurance products depend on the bare essentials on policies and scenarios,

where the scenarios are generated by a scenario generator which produces up to

a certain amount of scenarios. We will assume that scenario optimization has

already taken place. Therefore, only the amount of policies can be reduced.

Model points are already being used by life insurers and have historically

been based on actuarial knowledge. Theoretical foundations are therefore not

made and as far as our knowledge reaches, no research has been done to inves-

tigate the process of creating the model points and measuring the inaccuracy of

them as an application for insurers.

Correctly measuring the inaccuracy is an important task. Inaccuracy can

now only be measured by comparing a grouped run to an ungrouped, the so

called base run. As said previously, a base run does take a lot of time and can

therefore not be performed to often. However, the base run is based upon a set

of policies which may change over time. What is done now, is that the grouped

run at time t

0

is compared to the base run at time t

0

, which is still correct. The

inaccuracy can now be measured perfectly. However, an additional time con-

suming task is to validate the model points as time has passed and the portfolio

has migrated. Here an error is made by comparing the grouped run at t

1

to the

ungrouped run at t

0

. By presenting a recipe based on theoretical foundations

we can therefore improve not only processing times, but also estimate the error

correctly, without having to perform a base run again.

The remainder of the paper is organized as follows: in Section 2 we explain

more about life insurances, ALM and Solvency, and the idea of model points.

From there we continue to Section 3, where we create a theoretical framework

for the model points. We explain notations, model the problem and nd good

indicators for grouping and error approximation. We then we move on to a

real life product in Section 4 on which we will apply our model and present the

results. Finally in Section 5 we make concluding remarks and comment on some

further research.

4

2 Life insurances

Insurers protect the insured for some unforeseeable (mostly negative) events that

can occur in the future. Of course this does not come for free. The insured pays

a premium which can be monthly, yearly or some other frequency. Whenever

a certain event happens, the insurer has a liability to full. To calculate the

present value of the expected liabilities to which they are exposed at a certain

moment in time, they use an Asset Liability Model (ALM). ALM models are

used to calculate the present value of all future assets and liabilities. However

in this paper we are only interested in the liability side.

2.1 ALM models

By using these ALM models, companies can show that they are able to pay

out all policies under normal conditions. There exist some minimum amount

of nancial resources that insurers must have in order to cover the risks. The

rules that stipulate those amounts are bundled under the name Solvency. It is

to ensure the nancial soundness of insurance undertakings, and in the end to

protect policyholders and the stability of the nancial system as a whole.

Previously, only closed form ALM models where used, which calculated the

present values deterministically. In the last decade they have been moving to-

wards a more realistic valuation [12] where stochastic modeling has been proved

to be very useful. It makes use of various scenarios, where every scenario repre-

sents some future event. These scenarios are produced by a scenario generator.

However the development of more realistic models does also come with a number

of drawbacks. Most notably is the very slow runtime.

2.2 Solvency II

Recently (July 2007)[14], they have announced the arrival of Solvency II, which

replaces old requirements and establishes more harmonized requirements across

the EU and therefore promoting competitive equality as well as high and more

uniform levels of customer protection. It is similar to the Basel II, which is

the regulation within the banking world. For Solvency II, market consistent

embedded values and other initiatives make it even more important for insur-

ance companies to model on a stochastic basis. Doing so, as already said, has

signicant implications for run times in valuing insurance portfolios. However,

reporting needs to be done on a frequent basis which means there are certain

time constraints that need to be fullled. Since Solvency II is expected to be ef-

fective from 2012 [15], there is an enormous interest in methods that can rapidly

as well as accurately predict the liabilities to which they are exposed[13]. As

said in the introduction, model points are a way to accomplish this.

5

2.3 Model Points

A model point is an aggregate of policies, that should be a good representation

of a cluster of policies. However what does good mean? If we think of what

present value the original policies produce, and compare the resulting present

value when using our model points, then we do have an indication of the quality

of our model points. An additional criterion, is that we do not want too many

of those, otherwise we do not see any computation time reduction.

A typical liability model can be grouped in three components: scenarios,

policies and attributes. As already stated, scenarios are calculated by a scenario

generator and we have assumed that they are already optimized. Therefore they

are assumed to be really dierent and necessary, which means that there is no

further grouping to be done here. The attributes are characteristics of the policy

holder (age, sex, insured amount, etc) and product specics (duration, product,

premium, etc.). These are necessary to dene the product. Furthermore the

amount of attributes a policy has could be around 50, as compared to the

number of policies, of which there are innitely many. This means it is the

policies that we can group together. This is done, in such a way that, if policies

do resemble one another, we can simply group them in a new ctional policy,

which represents the individual policies. This is called the model point.

6

3 Framework for the model point generation

3.1 The problem in an Operations Research context

In this section we will outline the model and provide a theoretical framework

for model point creation. We expect as inputs a data set X M

mn

which is

an mn matrix with policy data, where m is the number of policies, and n the

number of attributes. A single policy is denoted by x = [x

1

x

2

. . . x

n

]

T

, which is

a column vector of the attributes. Furthermore, we expect a black-box model

C(x), which calculates for a scenario, and a policy x, the projects the cash ows

of this policy to a certain time moment. A set of scenarios S, where s S is

implicitly assumed in the model.

In the matrix X, every element is denoted by x

i

j

X, i M and j N,

where M is the set of the policies and N the set of the attributes of a policy.

The black-box model is described by the function C(x) : R

m

R in which

for every policy x the discounted cash ows are calculated. The objective is to

minimize the CPU time to calculate the present value of the cash ows C(x),

subject to the restriction that the quality of the model points is sucient.

Note that attributes are can be of very dierent types (e.g. dates, amounts,

percentages, etc.) which are all on a dierent scale. In order to compare them in

a later stage, they can be scaled to correct for this. This is done by considering

the maximum and the minimum of the range of an attribute and divide the

value of every attribute minus the minimum value by their respective range.

For the sake of notation we assume the data to be already scaled.

Model point creation could be done in two ways: we could just take a rep-

resentative sample out of the policies and view these as the model points, or we

could use a more sophisticated method by carefully constructing these model

points. We take the approach of carefully constructing the model points, and we

will call this grouping. This is done by aggregating policies in the n-dimensional

space D R

n

.

We will now dene our objective function. Let X

be our set of obtained

model point policies, k M

the index of a model point, where M

is the set

of all model point indices. Furthermore, let the amount of model point policies

be dened as m

= [M

[. Then assuming that the time needed to calculate the

present value of every policys cash ow is a constant t in minutes,

1

we get the

simple objective function:

min t m

(1)

There are of course limits to the amount of policies we can group, since we

still need to ensure that our set X

is a good representation of the original set X.

In other words we do not want the loss of accuracy to be bigger then a certain

amount p R. The next question, how to measure this accuracy loss? In the

end, the present value of the cash ows resulting from the use of the model

1

Note that this needs not to be true in practice. Policies with a longer duration tend to

take longer then policies with a short duration.

7

points or the use of the original data set should be very close to one another.

This implies that the accuracy loss should be measured as the dierence in the

pv of the cash ow calculations. This suggests the following constraint to be

added to the program:

s.t. [

iM

C(x

i

)

iM

C(x

k

)[ p s S (2)

where p can be set company specic. To be able to solve the problem men-

tioned above, we need to know

iM

C(x

i

) which we will call the base run

calculation. Furthermore, we need to construct the set of model points X

and

obtain

kM

C(x

k

), where x

k

is a model point policy. We would also like to

know before we group, in which way we should group, in order to make the error

as small as possible. This is called the estimation of our errors and we denote

them per model point policy as

k

. Which means that there are basically three

actions we need to perform;

1. Calculate the base run (we still need this at rst, to check if our estimation

works)

2. Calculate the estimated errors from the model points as compared to the

base run

3. Calculate the empirical discounted cash ows resulting from the model

points (to check against the base run)

3.2 Minimizing the error induced by making use of model

points

So on which criteria should we group, and what error do we create by grouping

in this way? Can we upper bound this before we even group? Let us rst dene

our groups G

k

, k M

. Suppose that we have created m

groups. Let every

group contain a subset of the policies G

k

X = 1, . . . M , and let every

policy be in at least one group

k

G

k

= 1, . . . , M. Furthermore, let no policy

be in more then one group: G

k

G

k

= , k, k

, k ,= k

. We dene the

averages of the policies in each group as our model points. Then we can express

the distance of a policy to the respective model point, as follows: x x

k

where we dene x

k

= [

iG

k

x

i

1

|G

k

|

. . .

i

G

k

x

i

n

|G

k

|

]. Which is now the vector of

averages of every attribute j over all policies in group k.

Now, how much does the projected present value of the cash ows deviate

as we represent our policy x by a single model point x

k

? To approximate this,

we will make use of the Taylor series expansion. Let us rewrite C(x), by adding

and subtracting the model point x

k

from it.

C(x) = C(x +x

k

x

k

) =

C(x

k

) +

dC(x

k

)

dx

(x x

k

) +

1

2

_

x x

k

_

T

d

2

C(x

k

)

dx

2

(x x

k

) +

q=3

1

q!

dC

(q)

dx

(q)

_

x x

k

_

(q)

(3)

8

where

q=3

1

q!

dC

(q)

dx

(q)

are the q-the order derivatives

2

.

Furthermore the Jacobian is:

dC

dx

=

_

C

x1

,

C

x2

, . . . ,

C

xn

_

and the Hessian,

H =

d

2

C

dx

2

=

_

2

C

x

2

1

2

C

x1x2

. . .

2

C

x1xn

2

C

x2x1

2

C

x

2

2

. . .

2

C

x2xn

.

.

.

.

.

.

.

.

.

.

.

.

2

C

xnx1

2

C

xnx2

. . .

2

C

x

2

n

_

_

If we now sum our equation (3) over all policies we get the following formula:

iM

C(x

k

) +

dC(x

k

)

dx

iM

(x

i

x

k

) +

1

2

iM

_

x

i

x

k

_

T

d

2

C(x

k

)

dx

2

(x

i

x

k

) +

iM

q=3

1

q!

dC

(q)

dx

(q)

)

because of the equivalence of the Jacobian, Hessian and higher order derivatives

for every policy i we can take these terms out of the sum.

For simplicity, suppose rst that

1

q!

dC

(q)

dx

(q)

= 0 for q = 2, which means that

we suppose that C(x) is linear, then the following set of equations hold

3

:

iM

C(x

i

) =

N C(x

k

) +

dC(x

k

)

dx

iM

(x

i

x

k

) =

N C(x

k

) +

dC(x)

dx

_

iM

x

i

N

iM

x

i

N

_

. .

0

=

N C(x

k

)

(4)

This states that we do not make any error at all! For grouping this is a really

powerful result, because this means that we can use only one bucket for a specic

attribute that is linear in the present value of its cash ows. In other words, we

can group this attribute away.

Suppose now, that

1

q!

dC

(q)

dx

(q)

,= 0?. If we now rewrite C(x), this gives:

2

Note that this is a non-standard use of a Taylor representation. If we replaced x x

k

by

h we see the familiar Taylor expression. If lim

h0

h is equivalent to an increase in the amount

of model points

3

This implicitly sets all higher order derivatives also equal to 0

9

iM

C(x

i

) =

kM

iG

k

C(x

i

) =

()

kM

[G

k

[C

_

_

_

_

_

_

_

_

iG

k

x

i

1

|G

k

|

iG

k

x

i

2

|G

k

|

.

.

.

iG

k

x

i

n

|G

k

|

_

_

_

_

_

_

_

_

_

+

kM

iG

k

1

2

_

x

i

x

k

_

T

k

H

mp

_

x

i

x

k

_

=

kM

[G

k

[C

_

_

_

_

_

_

_

x

k

1

x

k

2

.

.

.

x

k

m

_

_

_

_

_

_

_

+

kM

iG

k

1

2

_

x

i

x

k

_

T

k

H

mp

_

x

i

x

k

_

where in (*) we used our result from (4). However this is only holds whenever

1

q!

dC

(q)

dx

(q)

= 0 for q = 3. However we will assume from now on, that higher

order eects are negligible, which denes the error that we make to be solely in

the second order derivatives. Note that we can only consider them negligible,

whenever our distance x

i

x

k

, k M

, i G

k

is small.

Considering now only one group k, for this group we can express the error

made as follows:

k

=

iG

k

C(x

i

) [G

k

[C(x

k

)

=

iG

k

_

1

2

_

x

i

x

k

_

T

H

mp

k

_

x

i

x

k

_

_

=

iG

k

1

2

_

x

i

x

k

_

T

_

jN

2

C(x

k

)

x1xj

(x

i

j

x

k

j

)

jN

2

C(x

k

)

x2xj

(x

i

j

x

k

j

)

.

.

.

jN

2

C(x

k

)

xnxj

(x

i

j

x

k

j

)

_

_

Now for j

1

, j

2

N we have

k

=

iG

k

j1N

j2N

1

2

2

C(x

k

)

xj

1

xj

2

(x

ij1

x

k

j1

)(x

ij2

x

k

j2

)

(5)

Suppose now that the cross derivatives are equal to zero

2

C(x

k

)

xj

1

xj

2

= 0, j

1

,=

j

2

, then the error per model point is reduced to:

k

=

iG

k

jN

1

2

2

C(x

k

)

x

2

j

(x

i

j

x

k

j

)

2

This now denes our grouping method. The grouping should be done in the

following way; if

2

C

x

2

j

is large in a certain area, then we need x

i

j

x

k

j

to be small.

This means that we need a lot of groups in those areas where the second order

derivatives are large.

10

But what if the cross derivatives are not equal to zero? By determining the

norm of the Hessian |H| we can dene our grouping method. Let us denote by

|

k

H

mp

| the Hessian evaluated at model point k. If we would calculate |H|

2

we

would have to calculate the eigenvalues of H and consequently solve the system

(H I) u = 0 of linear equations, where u is the eigenvector corresponding to

the eigenvector . Using Cramers rule, this system has only non-trivial solutions

if and only if its determinant vanishes, which means that the solutions are given

by: det (H I) = 0 which is the characteristic equation of H. This however

involves solving polynomial function of order n , p () =

jN

(1)

j

S

j

nj

,

where S

j

are the sums of the principal minors. Since there exist no exact

solutions to this system when n > 4, one has to resort to root nding algorithms

such as Newtons method. In packages such as Mathematica or Matlab, these

algorithms are readily available, but this is very costly and not desirable in

practice. What we can do however, is instead of making use of the 2-norm we

can use the norm, |H|

= max

jN

N

[H

jj

[

4

, where j are the rows in

H and j

the columns, H

jj

the element of H in row j and column j

. This is

an easy calculation and can therefore be done in practice. We can now upper

bound the error by

k

|

k

H

mp

|

iG

k

j1N

j2N

_

x

ij1

x

k

j1

_ _

x

ij2

x

k

j2

_

k M

(6)

which states again that we should create more buckets whenever the innity

norm is bigger. We can see that whenever our function C(x) is linear in its

attribute j, the innity norm equals zero, and again, one bucket suces.

3.3 Numerical model point creation

Before we move on, we will rst solve some practical issues with the method in

Section 3.2. So far we have assumed that the function C(x) is known and we have

shown that, whenever we know this function we can analytically dierentiate it.

Furthermore, we can obtain a grouping strategy, as well as an upper bound on

the error made as we have shown in equation (6). However, we do not always

have access to this function. Therefore we will also dene a numerical way to

obtain a grouping strategy.

3.3.1 Grid construction

To obtain information about the function C(x), we need to explore the function

over the range of the attributes. In order to do so we create a grid. We will call

this grid our exploration grid. We call it exploration grid to avoid confusion

later on, when we describe the creation of the model points in Section 3.3.3.

The exploration grid is measuring the value of C(x) at dierent values of x

j

over the range of every attribute j. Constructing such a grid can be a time

4

If cross derivatives are 0 we simply have only the diagonal elements of H as every sum

11

consuming task, especially if we want it to be very precise. We discus this in

Appendix A.1. This however is a one time only investment. Whenever we know

the landscape where our function C(x) lives we do not have to perform this

action again. In this paper we assume that we have created a grid in a nested

way as in Appendix A.1. Denote by L the set of grid points and let a single grid

point be denoted by l L. The amount of grid points is now [L[. These grid

points are then constructed by dening per attribute j an amount of buckets b

e

j

,

which we will call our exploration buckets. The feasible range per attribute j

is now divided in b

e

j

buckets. This implies a division of the space D in an equal

amount of hypercubes [L[ =

jN

b

e

j

, which we index by l L. Then D

l

is a

hypercube, where

l

D

l

= D and D

l

D

l

= , l ,= l

, l, l

L. In Appendix

A.1, we describe two grid construction methods. For more advanced grids we

refer to [10], where an adaptive grid is discussed.

If we move back to our Hessian H, as discussed in Section 3.2, it now has

to be evaluated in l points. Each point is now the center of a hypercube D

l

.

Let us distinguish between those Hessians by introducing the notation

l

H

e

for

the exploration Hessian evaluated in grid point l. Since we need to numer-

ically compute the Hessian by using the central dierence formula, we need

to evaluate the function C(x), 3 times (C(x

1

, . . . , x

j

, . . . , x

n

), C(x

1

, . . . , x

j

+

j

, . . . , x

m

), C(x

1

, . . . , x

j

j

, . . . , x

n

)) per entry of

l

H

e

. This means that for

every

l

H

e

, being a symmetric n n matrix, we need to call C(x), 3

n(n+1)

2

times. In total this makes [L[3

n(n+1)

2

function calls. Whenever we construct

such a grid, this should really be taken into consideration, since the amount of

function calls becomes very large, even for a small number of grid points.

3.3.2 Determining the amount of buckets

Let us now dene the maximum for every attribute j over all grid points l

in

l

H

e

, l L, by h

e

j

= max

lL

N

[

l

H

e

jj

[, j N. We can now put all

these h

e

j

in a column vector h

e

R

n

. The most important attribute is now the

attribute

j corresponding to the value |h

e

|

. Note that this value is equal to

max

lL

|

l

H

e

|. The vector h

e

denes our grouping structure. First we set the

amount of buckets for attribute

j, the amount of buckets for the other attributes

is now determined, based on their relative value of h

e

j

, j ,=

j compared to h

e

j

.

Let b

mp

j

denote the amount of model point buckets for attribute j. Then we

can calculate b

mp

j

by using the following formula b

mp

j

= b

mp

j

h

e

j

h

e

j

|, j N

j,

where [0, 1] is some parameter that should be chosen in any way to adjust

for the amount of buckets b

mp

j

. Note that the amount of buckets b

mp

j

, j N

can never be more then b

mp

j

.

3.3.3 Creating the model points

The amount of buckets for every attribute j can be spread in various ways over

the range of every attribute. We could spread them evenly for every attribute j,

or be somewhat more sophisticated and let the population distribution decide

12

on the cut-o points. Dividing the range of every attribute j in any way, we

obtain

jN

b

mp

j

hypercubes in the R

n

. Note that some of these hypercubes

may not contain any policies. We will not create any model points in empty

sets, which means that the amount of model points constructed in such a way

is m

j

b

mp

j

, where k is the model point of G

k

, just as in Section 3.2.

Whenever the amount of model points is considered to be too large, one should

decrease b

mp

j

and recompute b

mp

j

, j ,=

j until the desired amount of groups k

is formed.

3.3.4 Assigning the policies to the model points

The next step is to assign to every policy i a group G

k

. This is done by checking

if the policy is within the range of group G

k

in every dimension n. Once we

know i M, its group i G

k

, we can compute the nal model point policies

x

k

, k M

as follows: x

k

=

_

iG

k

x

i

1

|G

k

|

. . .

iG

k

x

i

n

|G

k

|

_

T

, k M

3.3.5 Estimating the errors

To estimate the errors made by using the model points we can use the formula

introduced in (6). However we need to evaluate |

k

H

mp

|

, k M

to obtain

an exact upper bound on the error made by our grouping strategy. This involves

again calling the function C(x), m

3

n(n+1)

2

times. Note that this is no

problem whenever m

is small (this is what we are trying to achieve anyhow).

However, whenever m

is considered to be too large, we can also get an ap-

proximation on the upper bound by considering the values of |

l

H

e

|

, l L,

which we have already calculated. This means that this does not cost any ex-

tra function calls. We can approximate this, by considering the distance from

the model point to every grid point (x

l

x

k

), and use either the maximum or

the closest |

l

H

e

|. Another, somewhat more sophisticated method, would use

interpolation techniques as in [1]. We will describing an interpolation method

by looking at the grid points that are the closest in every direction. So in our

dimension n we have 2

n

closest grid points, because in every dimension we have

two ways in which we can go. These will all be incorporated for the estimation

of |

k

H

mp

|

, by considering their relative distance from x

k

. Let all closest grid

points to k be denoted by l

z

L where z = 1, . . . , 2

n

|

k

H

mp

|

|

l1

H

e

|

(x

l1

x

k

) +. . . +|

l

2

n

H

e

|

(x

l

2

n

x

k

)

2

n

z=1

(x

lz

x

k

)

Of course since this is only an indication, it cannot guarantee a certain amount

of error, but is still important from a practical view.

13

4 A real life example

4.1 Describing the product

The product of focus, is a so called lijfrente polis, and the policies that we will

look at are already in force. The product consists of a single premium payment,

the policies are already in-force. When a policy is in-force, it is means that policy

holder is currently insured. We make a picture at a certain time moment and

look at which policies are captured by the interval between the start date

and end date

5

. This implicitly means that the premium payment has already

occurred and we will therefore only look at cash outows. The payment takes

place at the start date and the amount is equal to the grosspremium. For

some reason, this is not available in the database and the grosspremium is

calculated by discounting the insured amount. The insurance company invests

the grosspremium in stocks and bonds and while doing this it guarantees a

return on the clients investment equal to an interest rate over the rst ve

years and another interest rate over the rest of the period. For this product,

there are three types of benets for the insured: the surrender, death, and the

maturity benet.

Surrendering means that you have the option of withdrawing money in be-

tween. Whenever someone surrenders, the surrender value that he wishes to

withdraw will be used to buy an immediate annuity. The market value of this

immediate annuity is scenario dependent and will be paid out as the surrender

benet. The minimal annuity duration is based on the age and sex of the pol-

icy holder which is looked up on a specic table. The surrender cash ow is

now the total discounted value of all future annuity payments. The probability

associated with a surrender is scenario dependent.

Furthermore we have a death benet which is equal to the insured amount.

This is the money that is paid in case of death.

Finally the product has a maturity benefit which is equal to part of the

insured amount. The maturity benet is the money you get upon expiration

of the policy.

Annuities that were already in-force were also in our data set. However,

given annuities are modeled deterministically, and therefore not dependent on

scenarios we do not consider them. Furthermore, there were 500 scenarios for

which we did not know the rationale behind, nor the likelihood of the occurrence

of the scenarios.

4.2 Selecting the attributes

The rst thing we need to do is get a feeling for the attributes before we can

compute our Hessian. What are they, and on what scale are they projected?

This becomes really important whenever we will disturb them with our

j

.

In our model there exist 32 policy attributes which we have to examine. We

should be careful here, as some of them are not real valued (e.g. product type).

5

Attributes are denoted in monospace

14

Therefore, this is why we will look at a specic product type. Some other

attributes have only a few outcomes over the range of the attribute which means

there is not much grouping to be done. There also exist a lot of attributes that

are calculated by the model, and attributes that are not used for our specic

product. So at rst we will produce the descriptive statistics of some of the

attributes in Table 1. According to these statistics we can get a broad idea on

which attributes it might be interesting to group. We can already specify one

on which we will not group: sex, since it only has two possible values, which

are integers. After a thorough investigation in the total set of attributes, we

concluded with ve attributes that where thought to be the main determinants.

All others where either dependent on those ve or, were considered to be critical,

which means that they will not be grouped upon. The resulting attributes are

presented below:

1. date of birth

2. start date

3. end date

4. insured amount

5. interest

4.3 Exploring the function

Now that we have found our set of interesting variables we want to measure their

inuence on the projected cash ow under every scenario. For this, will follow

our method as described in Section 3.3 we will construct a grid with virtual

policies. It is virtual in the sense that the policies do not come from the data

set X. They are made using the feasible input range for every attribute. This

feasible input range is assumed to accompany every program. In our program

however, we did not have this feasible input range and we constructed these by

looking at the descriptive statistics of the data set. In Table 1 we present these

statistics. The feasible input range of an attribute is now determined by the

dierence between the maximum and the minimum value of an attribute.

There exist various options to create such a grid and we discuss two methods

in Appendix A.1. Let us rst consider a nested grid. This would require at

least 2 3

n

amount of function calls, when we consider only 2 grid points per

attribute (one in its minimum and one in the maximum, and disturbing them

all with a + and a ). For n = 5 this is already 7776 calls of C(x). Since

a policy takes on average 70 seconds to calculate on our hardware, this would

take more then 6 days to calculate. This was considered to be too long for us.

Therefore we use a sequential grid construction, which means that for every

attribute we move from its minimum to its maximum in 10 steps and set all

other interesting parameters equal to their averages. These are then the virtual

policies. We are aware of the fact that we lose a lot of accuracy in this way

and we can only hope that the averages are a good representative of the whole

15

function. This also means that we have only one entry in the matrix H(x

l

)l L

, which is the second order partial derivative with respect to the attribute on

the corresponding axis where we created our grid. This is immediately the

norm of the matrix

l

H

e

, l L. Before we continue, we should check if the

constructed grids represent feasible combinations of the attributes. This means

that no start date can fall after an end date or that the date of birth of

a person should be before the start date of a policy.

After constructing the grid points, we can put them one by one in the model

and obtain the resulting discounted cash ows for every scenario.

4.4 Interpreting the function

Now that we have projected the cash ows for every virtual policy for 500

scenarios we will rst investigate the cash ow movement over the ten grid

points. We will look at scenario 1, which we plotted in Figure 2.

A rst step is interpreting these graphs. Starting with the cash ows for

the date of birth, we see that the later you are born the more negative the

projected cash ow becomes. This can be explained by the fact that the later

you were born, the younger you are now and the longer you are expected to

live. The insured amount is build up of two components, the death benefit

insured amount and the surrender benefit insured amount. The relation

between the death benefit and the surrender benefit is on average 1 : 4,

which makes the surrender benefit the strongest determinant of projected

cash ows. Once you have died, there will not be any possibility to surrender.

This means that, the longer you live the more surrender benefit you will get,

and maybe in addition even the death benefit.

The start date is uctuating a lot and one can hardly tell what the drivers

behind this function are. However, if we look at the scale, it is not an interesting

variable at all. We can therefore simply put this attribute in one bucket without

making a signicant error.

Looking at the end date, we see that when we move our end date to a later

time moment, the cash ow is also increasing, which means that the liability is

decreasing (the cash ows are all negative). Because we expected the liability

to increase when a policy has longer duration the result is really counter intu-

itive. However looking at the actuarial model, it can easily be explained. By

shifting the end date to a later time moment, we are increasing the duration.

When investment premium is calculated, it makes use of the insured amount,

the duration and the interest rate. Discounting the insured amount at

the same interest rate over a longer term, results in a lower investment

premium. In turn, the investment premium is used to calculate the possible

amount of surrender cash ows, which is now of course lower.

Considering the insured amount we see a linear relationship between at the

chosen grid points between the project cash ows and the insured amount.

However, this is only an expectation, the function may still uctuate in between

the grid points. However when making the buckets, we expect that we can put

this attribute in one bucket without making any signicant error.

16

Discounting with higher interest rate will result in a lower investment

premium, which again causes the discounted cash ows will be lower.

What we can see from these functions is that they are either monotonically

increasing or monotonically decreasing except for the start date, which was

not considered important because of its scale. However, if the scale would have

been very large the amount of buckets needed would be very big which would

cause issues. However, all the functions seem to be not that far from linearity

and we therefore do not expect large errors at all, even if we will group them

all in one large model point (we will further discuss this in Section 4.6).

To estimate our second order partial derivatives for every attribute we use

the central dierence formula. The graphs are presented in Figure 3. If we look

at them, one can rst of all see, that all second order derivatives ar not far

from zero which means linearity. Since we did not know the whole cash ow

function, the function like end date might uctuate a little bit in between. This

can simply be seen as numerical noise. Using the recipe presented in Section

3.3, we can take the maximum second order partial derivative for every grid

point and take the maximum of these to determine the amount of buckets for

the attribute. The results are presented in Table 3, where they are all sorted

according to importance. We now see that the end date is considered the

most important attribute. Setting the amount of buckets for the end date,

automatically induces the amount of buckets for the other attributes as dened

in Section 3.3.2.

4.5 Generating model points

Until now, we have not yet used any policy data. The projected cash ow

functions were solely based on the feasible range of the attributes as discussed

in Section 4.3. The policy data that we will use is from an existing insurance

company. However for privacy and computational reasons we have modied the

data. We will now make use of these policies for the bucketing of the attributes,

by spreading the population evenly over the buckets as described in Section

3.3.2. In Microsoft Visual Basic for Applications (VBA) we developed a script

to produce a cumulative distribution function which gave us our cut-o points

for the buckets at 1/b

j

. Now that we have set our buckets, we need to nd out

which policies are in a certain group. We will do this by using the method as

described in Section 3.3.4. For this we again used VBA by checking if a policy

is within the range of every buckets cut-o points and code every policy with a

group number. The model points are now the averages of every attribute over

the policies within the group.

4.6 Results

We will rst produce a base run, where we calculate the cash ow by using all

single policies. In our resulting data set we have 243 policies. The important

statistics we need are the calculation time and the resulting present value per

17

scenario. We will present them in Table 2. As shown in Table 2 calculating the

cash ows for all single policies took 160 minutes.

4.6.1 Grouping

To show our method at work, we will explain stepwise what we can achieve.

Table 3 is produced as described in Section 3.3.2, from which we can see that

the end date requires the most groups. We will initially set the end date to 3

groups which gives the date of birth 2 groups and the amount insured and the

interest rate only 1 according to our formula in 3.3.2. Therefore we go from

243 individual policies to 6 model point policies. However, let us start bottom up

to show the algorithm at work. We start by grouping the insured amount in one

model point. Since this attribute looked linear we do not expect any error, apart

from the error that we made by assuming that the cross derivatives are zero.

When grouping this attribute away we could decrease the amount of policies by

a factor 3, i.e. 243 policies to only 81 model point policies. Computation times

dropped from over 2.4 hours to only 62 minutes. If we now look at our cash

ow deviation, we still have an accuracy of 99.9995% which is in line with our

theory.

Now, as we have seen, we can eliminate the start date attribute since it

does not contribute much to the discounted cash ow. When doing this, we

actually also group this one away and set the value equal to its average. A

reduction of 3 is again made i.e. 81 model point policies to 27. Our accuracy

lowers slightly but we are still 99.83% accurate. Solving this took only 20

minutes.

The interest rate is then grouped in one bucket which leaves us with only

9 model point policies. Computation times are now only 7 minutes and, quite

unexpectedly, the accuracy is only 97.15 %, which is still fair for most life insur-

ers since they are aiming for an accuracy in between 95% and 98%. The result

was unexpected given that the interest rate looked linear. However, recall

that we only gained very local insight by assuming that the cross derivatives

are zero and that we have at every grid point only the second order partial

derivative in one direction. Although the interest rate is nearly linear on

this local part of the hyperplane, it uctuates more elsewhere.

Therefore we will see if perhaps the date of birth should have been next

on the list instead of the interest rate. When now grouping, in addition to

insured amount and start date, the date of birth in one model point, we are

98.25 % accurate. This is also unexpected but can be explained by the weakness

of our local grid (see Appendix A.1)

However, let us continue in the way that our algorithm predicted. In the

end, this leaves us with 6 model points which are 95.91 % accurate. This took

only 3.3 minutes. Therefore, what would happen if we would group them all in 1

model point? Doing this, leaves us still with 95.72 % of accuracy. Again we are

5

All runs where performed on an IBM Lenovo T61 with Intel T7500 Core 2 Duo 2.2

GHz Processor with 2.0 Gb of RAM. Microsoft Visual Basic for Applications was run on the

Windows XP operating System.

18

confronted with the limited reliability of the local insight of a sequential grid.

The function C(x) seems to be very at and does not seem to uctuate very

much over the whole domain. As insurance companies really do have trouble

grouping policies while maintaining accuracy, this is generally not the case as.

It could be due to the chosen product or the restriction on the input parameters.

It was however not very well suited for demonstration purpose of our method.

4.6.2 Approximate deviation from the base run

For the insured amount we looked at the error that we can predict by grouping

them all in one model point. By using the interpolation method as described

in Section 3.3.5 our model estimates an accuracy of 99.999999% which is higher

than the actual accuracy as we can see in Table 3. Although this does not look

too bad as compared to the 99.9995%, one has to put this in perspective to the

total error range we are looking at. We will never make a higher error than

95.72% since this is the error made when we group all policies in one model

point. Again, we can not be conclusive and the lack of a good grid disturbs the

outcomes.

19

5 Conclusion and future work

In this paper we have provided a solution to estimate the error induced by the

usage of model points, a solution to a problem that insurance companies were

not even aware of. They estimated the errors of their grouping strategy based

on an outdated base run. We have shown how we can correctly upper bound

these errors without having to calculate the base run again.

Furthermore we have dened a way how insurance companies could group

their policies. Whenever a linear attribute is encountered it can be grouped

away, without making any error at all. If an attribute is non-linear, it should be

grouped according to the Hessian in a certain area of the domain of the function

that discounts the cash ows.

Even if the exact analytical function is not available, we have shown numer-

ical ways to group the policies. We made use of grids to explore the function

that calculates the present value of the cash ows. These exploration grids do

consume a lot of time, however if one is willing to make the one time only invest-

ment of exploring this function, we can upper bound the error made. Moreover,

if one does not want to invest too much in the construction of the grid we can

still provide an approximate upper bound.

For a simple but real life example we have illustrated the method. We have

shown the tradeo and drawbacks of a fast local exploration of the landscape,

by making use of the sequential grid versus a slow nested grid construction. The

slightly weak results can be attributed to the unfortunate choice of the product

and lack of computing power for a good grid.

Improvements can be made by better distributing the buckets over an at-

tribute. This could be done by distributing them depending on the Hessian over

the range of the attribute, instead of uniformly distributing them. Considering

the grids, a more sophisticated grid such as an adaptive one, may be of great

help. However, if we know the analytical function we might not need to use the

exploration grids at all and we can perfectly upper bound the errors. The exact

calculations can be performed by making use of software such as Mathematica

or Maple.

There is still a lot of work to be done in this area, however a rst step has

been made which can greatly benet insurance companies.

20

References

[1] Robert S. Anderssen and Markus Hegland. For numerical dierentia-

tion, dimensionality can be a blessing. Mathematics Of Computation,

68(227):1121 1141, February 1999.

[2] J. Ghosh A.Strehl, G.K. Gupta. Distance based clustering of association

rules. Department of Electrical and Computer Engineering, 1991.

[3] Prof. dr. A. Oosenbrug RA AAG. Levensverzekering in Nederland. Shaker

Publishing, 1999.

[4] S. Z. Wang G. Nakamura and Y. B. Wang. Numerical dierentiation for

the second order derivative of functions with several variables. Mathematics

Subject Classication, 1991.

[5] Hans U. Gerber. Life Insurance Mathematics. Springer, 1997.

[6] R. Bulirsch J. Stoer. Introduction to Numerical Analysis. Springer-Verlag,

2 edition, 1991.

[7] J.M. Mulvey and H.P. Crowder. Cluster analysis: An application of la-

grangian relaxation. 1979.

[8] J.M. Mulvey and H.P. Crowder. Impact of similarity measures on web-page

clustering. 2000.

[9] C.M. Procopiuc P. K. Agarwal. Exact and approximation algorithms for

clustering. Management Science, 25(4):329340, 1997.

[10] D. S. McRae R. K. Srivastava and M. T. Odmany. An adaptive grid

algorithm for air-quality modeling. Journal of Computational Physics,

(165):437472, 2000.

[11] Vladimir I. Rotar. Actuarial Models: The Mathematics Of Insurance.

Chapman & Hall, 2006.

[12] J. Rowland and D. Dullaway. Smart modeling for a stochastic world. Em-

phasis Magazine, 2004.

[13] M. Sarjeant and S. Morrison. Advances in risk management systems of life

insurers. Information Technology, September 2007.

[14] HM Treasury. Solvency II: A new framework for prudential regulation of

insurance in the EU. Crown, February 2006.

[15] HM Treasury. Supervising insurance groups under Solvency II; A discussion

paper. Crown, February 2006.

[16] G.R. Wood and B.P. Zhang. Estimation of the lipschitz constant of a

function. Journal of global optimization, 8(1):91103, January 1996.

21

A Appendix

A.1 Gridconstruction

When we do not have an analytical model, we rely on numerical methods. To

gain insight in our cash ow function in order to later construct the Hessian, we

need to know the value of C(x) evaluated at dierent points. A correct grid can

only be constructed when we can isolate an attribute. This means we need to x

all attributes at a value except for one which we let increase over its range in a

certain number of steps depending on the chosen grid size. We can do this for all

attributes. However we need to check that the policies generated in this fashion

are feasible. This means that no end date can fall before a start date, etc.

6

. There are a many ways to construct such a grid, see [10], but we will present

two ways; sequential and nested grid construction. A nested grid construction

considers all possible combinations of the attribute values. On the contrary a

sequential grid construction calculates a grid per attribute, while xing the other

attributes at a certain value. Therefore set obtained by calculating sequential

grid points is actually a subset of the nested version. Although the nested

version is far more accurate, the computational complexity is overwhelming [1].

6

If we let our grid size go to we have the exact n-dimensional landscape

22

Algorithm A.1: Sequential grid construction(C(x))

j

= [0 . . . 0

j

0 . . . 0]

T

for r 0 to [R[

do

_

_

x

r1

= min

i

x

i

1

+r

maxi x

i

1

mini x

i

1

|R|

x

r2

= x

2

, x

r3

= x

3

, . . . , x

rn

= x

n

C(x

r

)

C(x

r

+

1

)

C(x

r

1

)

for r 0 to [R[

do

_

_

x

r2

= min

i

x

2

+r

maxi x2mini x2

|R|

x

r1

= x

1

, x

r3

= x

3

, . . . , x

rn

= x

n

C(x

r

)

C(x

r

+

2

)

C(x

r

2

)

.

.

.

for r 0 to [R[

do

_

_

x

rn

= min

i

x

i

n

+r

maxi x

i

n

mini x

i

n

|R|

x

r1

= x

1

, x

r2

= x

2

, . . . , x

r,n1

= x

n1

C(x

r

)

C(x

r

+

n

)

C(x

r

n

)

As illustration, let R be the set of buckets for every attribute j, and r R

a bucket. Consider then constructing [R[ buckets for every attribute j. This

will construct in total [R[

n

(1+2n) policies which is exponential in its attribute.

Suppose now that the time to compute the cash ow of one policy is t seconds.

The nested grid construction, as described above, will take t [R[

n

(1 + 2n)

seconds. To visualize this consider 4 attributes, for which we would like to

to compute 10 grid points, and the time to compute a single policy on this

computer is 70 seconds. This would take about 72 days to compute. For the

purpose of this paper, this was considered to be too long and we will look at the

sequential grid which takes (3 nt [R[) seconds and is a factor

|R|

n1

(1+2n)

3n

faster.

For the nested version we need to make a choice at what point to x the other

attributes. For now we will x them to be their averages, but we are well aware

that this might not be the correct choice. In addition the few points created in

23

the sequential loops only give very local insight in the true n dimensional space.

Algorithm A.2: Nested grid construction(C(x))

for r

1

0 to [R[

do

_

_

x

r11

= min

i

x

i

1

+r

1

maxi x

i

1

mini x

i

1

|R|

for r

2

0 to [R[

do

_

_

x

r22

= min

i

x

i

2

+r

2

maxi x

i

2

mini x

i

2

|R|

.

.

.

for r

n

0 to [R[

do

_

_

x

rnn

= min

i

x

i

n

+r

n

maxi x

i

n

mini x

i

n

|R|

C(x

r1,1

, x

r2,2

, . . . , x

rn,n

)

C(x

r1,1

+

1

, x

r2,2

, . . . , x

rn,n

)

.

.

.

C(x

r1,1

, x

r2,2

, . . . , x

rn,n

+

n

)

C(x

r1,1

1

, x

r2,2

, . . . , x

rn,n

)

.

.

.

C(x

r1,1

, x

r2,2

, . . . , x

rn,n

n

)

Faster hardware or splitting the workload over multiple processing units

could help speeding up the computation times for the grid construction, however

this still does not reduce the exponential n which is the main determinant for

the long runtime. The bottom line is that one should really make use of adaptive

grids.

24

A.2 Notations

1. D = [0, 1]

n

: the n-dimensional space in which the scaled function C(x)

lives

2. M = 1, . . . , m: represents the policies, where i M is a policy

3. M

= 1, . . . , m

: represents the model point policies, where k M

is

a model point

4. N = 1, . . . , n: represents the policy attributes, where j N is an

attribute

5. L: represents the grid points, where l L is a grid point

6. G

k

: group of policies represented by model point k

G

k

M, G

k

G

k

= ,

k

G

k

= M, k, k

7. x R

n

: a generic policy consisting of n attributes

8. x

i

R

n

: a specic policy i

9. x

k

R

n

model point policy k,

10. x

i

j

[0, 1]: the value of attribute j for policy i

11. C(x) : R

n

R: the function which discounts the future cash ows of

policy x

12. b

e

j

: the amount of buckets for attribute j in the exploration grid

13. b

mp

j

: the amount of buckets for attribute j in the model point grid

jN

b

mp

j

m

14. H R

nn

: the general Hessian

15. H

j

R

n

: the j-th row in H

16. H

jj

R: the element at row j and column j

of the Hessian

17. |H|

R: the norm of the Hessian

18.

l

H

e

R: the Hessian evaluated in exploration grid point l

19.

k

H

mp

R: the Hessian evaluated in model point k

20. h

e

j

R = max

lL

N

l

H

jj

: the maximum sum over the rows in every

exploration grid point l, for every attribute j

21. h

e

R

n

= [h

e

1

h

e

2

. . . h

e

m

]

T

22. |h

e

|

= |H|

R: the maximum value in the vector h

e

25

A.3 Figures

Grouped

policies

Individual

policies

Model

point

genera

tor

C(X)

Grouped cash

flows

Baserun cash

flows

Compare

Estimate

the

error

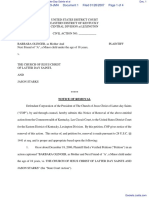

Figure 1: An overview of the structure

26

-100000

-95000

-90000

-85000

-80000

-75000

-70000

1 2 3 4 5 6 7 8 9 10

Date of birth

Date of birth

94304 66

94115,3

1 2 3 4 5 6 7 8 9 10

Startdate

94872,76

94683,4

94494,03

94304,66

Startdate

60000

40000

20000

0

1 2 3 4 5 6 7 8 9 10

Enddate

160000

140000

120000

100000

80000 Enddate

-1400000

-1200000

-1000000

-800000

-600000

-400000

-200000

0

1 2 3 4 5 6 7 8 9 10

Insured amount

Insured amount

-110000

-105000

-100000

-95000

-90000

-85000

1 2 3 4 5 6 7 8 9 10

Interest

Interest

Figure 2: cash ows for 5 dierent attributes

27

-0,0004

-0,0002

0

0,0002

0,0004

0,0006

0,0008

0,001

0,0012

0,0014

1 2 3 4 5 6 7 8 9 10

Date of birth

Date of birth

-0,008

-0,006

-0,004

-0,002

0

0,002

0,004

0,006

1 2 3 4 5 6 7 8 9 10

End date

End date

-4E-14

-3E-14

-2E-14

-1E-14

0

1E-14

2E-14

1 2 3 4 5 6 7 8 9 10

Insured amount

Insured amount

-0,02

-0,018

-0,016

-0,014

-0,012

-0,01

-0,008

-0,006

-0,004

-0,002

0

1 2 3 4 5 6 7 8 9 10

Interest rate

Interest rate

Figure 3: 2nd order partial derivative for 4 dierent attributes

28

A.4 Tables

Parameter Nr Of Dif-

ferent Val-

ues

Min Max Average

date of birth 2137 16-8-1933 31-12-1975 26-11-1952

sex 2 0 1 -

start date 1156 5-4-1995 23-6-2007 36679

end date 1469 22-7-2009 21-6-2037 43254

insured amount 2505 1086 213292 2911885

interest rate 1327 0 0.08552 0.065022

Table 1: Descriptive statistics

Accuracy (%) Time

(s)

Number

Of

Poli-

cies

buckets

date

of

birth

start

date

end

date

insured

amount

ih

100 9655 243 - - - - -

99.9995 3718 81 - - - 1 -

99.83 1194 27 - 1 - 1 -

97.19 415 9 - 1 - 1 1

98.25 285 9 1 1 - 1 -

95.9153 200 6 2 1 3 1 1

95.72 9 1 1 1 1 1 1

Table 2: Results

Attribute h

e

end date 431257.4164

date of birth 305609

interest 1.2607455

insured amount 0.098635801

Table 3: Maximal second order partial derivatives (scaled)

29

Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- LET Facilitating Learning EDITED3Документ12 страницLET Facilitating Learning EDITED3Likhaan PerformingArts HomeStudio100% (5)

- Olinger v. The Church of Jesus Christ of Latter Day Saints Et Al - Document No. 1Документ4 страницыOlinger v. The Church of Jesus Christ of Latter Day Saints Et Al - Document No. 1Justia.comОценок пока нет

- Openfire XXMPP Server On Windows Server 2012 R2Документ9 страницOpenfire XXMPP Server On Windows Server 2012 R2crobertoОценок пока нет

- Paradigm Shift in Teaching: The Plight of Teachers, Coping Mechanisms and Productivity in The New Normal As Basis For Psychosocial SupportДокумент5 страницParadigm Shift in Teaching: The Plight of Teachers, Coping Mechanisms and Productivity in The New Normal As Basis For Psychosocial SupportPsychology and Education: A Multidisciplinary JournalОценок пока нет

- Class NotesДокумент16 страницClass NotesAdam AnwarОценок пока нет

- Role of Courts in Granting Bails and Bail Reforms: TH THДокумент1 страницаRole of Courts in Granting Bails and Bail Reforms: TH THSamarth VikramОценок пока нет

- Rediscovering The True Self Through TheДокумент20 страницRediscovering The True Self Through TheManuel Ortiz100% (1)

- Stroke Practice GuidelineДокумент274 страницыStroke Practice GuidelineCamila HernandezОценок пока нет

- Introduction To Sociology ProjectДокумент2 страницыIntroduction To Sociology Projectapi-590915498Оценок пока нет

- 1999, 2003 - Purple Triangles - BrochureДокумент32 страницы1999, 2003 - Purple Triangles - BrochureMaria Patinha100% (2)

- Bubble ColumnДокумент34 страницыBubble ColumnihsanОценок пока нет

- Ogayon Vs PeopleДокумент7 страницOgayon Vs PeopleKate CalansinginОценок пока нет

- Mathematics in The Primary Curriculum: Uncorrected Proof - For Lecturer Review OnlyДокумент12 страницMathematics in The Primary Curriculum: Uncorrected Proof - For Lecturer Review OnlyYekeen Luqman LanreОценок пока нет

- SAP CRM Tax ConfigurationДокумент18 страницSAP CRM Tax Configurationtushar_kansaraОценок пока нет

- Debus Medical RenaissanceДокумент3 страницыDebus Medical RenaissanceMarijaОценок пока нет

- Humanistic Developmental Physiological RationalДокумент10 страницHumanistic Developmental Physiological RationalJin TippittОценок пока нет

- A Scenario of Cross-Cultural CommunicationДокумент6 страницA Scenario of Cross-Cultural CommunicationN Karina HakmanОценок пока нет

- The ReformationДокумент20 страницThe ReformationIlyes FerenczОценок пока нет

- Arsu and AzizoДокумент123 страницыArsu and AzizoZebu BlackОценок пока нет

- Excellent Inverters Operation Manual: We Are Your Excellent ChoiceДокумент71 страницаExcellent Inverters Operation Manual: We Are Your Excellent ChoicephaPu4cuОценок пока нет

- Corporation Law Case Digests Philippines Merger and ConsolidationДокумент7 страницCorporation Law Case Digests Philippines Merger and ConsolidationAlpha BetaОценок пока нет

- Afia Rasheed Khan V. Mazharuddin Ali KhanДокумент6 страницAfia Rasheed Khan V. Mazharuddin Ali KhanAbhay GuptaОценок пока нет

- Engineering Road Note 9 - May 2012 - Uploaded To Main Roads Web SiteДокумент52 страницыEngineering Road Note 9 - May 2012 - Uploaded To Main Roads Web SiteRahma SariОценок пока нет

- Bug Tracking System AbstractДокумент3 страницыBug Tracking System AbstractTelika Ramu86% (7)

- Number SystemsДокумент165 страницNumber SystemsapamanОценок пока нет

- Full Moon RitualsДокумент22 страницыFull Moon RitualsJP83% (6)

- International Conference On Basic Science (ICBS)Документ22 страницыInternational Conference On Basic Science (ICBS)repositoryIPBОценок пока нет

- Radiopharmaceutical Production: History of Cyclotrons The Early Years at BerkeleyДокумент31 страницаRadiopharmaceutical Production: History of Cyclotrons The Early Years at BerkeleyNguyễnKhươngDuyОценок пока нет

- 2022BusinessManagement ReportДокумент17 страниц2022BusinessManagement ReportkianaОценок пока нет

- A Tool For The Assessment of Project Com PDFДокумент9 страницA Tool For The Assessment of Project Com PDFgskodikara2000Оценок пока нет