Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Distressed Debt HF's Update (Mar 2013)Документ40 страницDistressed Debt HF's Update (Mar 2013)Peter UrbaniОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Random Forest in Excel and VBAДокумент24 страницыRandom Forest in Excel and VBAPeter UrbaniОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Do You Have To Be Abnormal To Beat The MarketДокумент3 страницыDo You Have To Be Abnormal To Beat The MarketPeter UrbaniОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Ishares Portfolio Analytics Coskew and CoKurt VBA3Документ178 страницIshares Portfolio Analytics Coskew and CoKurt VBA3Peter Urbani100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Cholesky Versus SVDДокумент4 страницыCholesky Versus SVDPeter UrbaniОценок пока нет

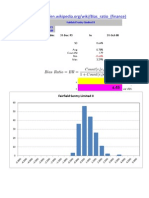

- Benford Bias Ratio VBA 2014Документ136 страницBenford Bias Ratio VBA 2014Peter UrbaniОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

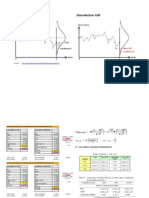

- Impact of Auto-Correlation On Expected Maximum DrawdownДокумент67 страницImpact of Auto-Correlation On Expected Maximum DrawdownPeter UrbaniОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Chimp Chump or ChampДокумент7 страницChimp Chump or ChampPeter UrbaniОценок пока нет

- Portfolio - Analytics Coskew and CoKurt VBA3Документ131 страницаPortfolio - Analytics Coskew and CoKurt VBA3Peter Urbani0% (1)

- Partial Correlation Network Graph VBA (DJINDI)Документ463 страницыPartial Correlation Network Graph VBA (DJINDI)Peter UrbaniОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Singular Spectrum Analysis Demo With VBAДокумент12 страницSingular Spectrum Analysis Demo With VBAPeter UrbaniОценок пока нет

- Intra-Horizon VaR and Expected Shortfall Spreadsheet With VBAДокумент7 страницIntra-Horizon VaR and Expected Shortfall Spreadsheet With VBAPeter Urbani0% (1)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Opalesque NewManagers Sep 2012Документ38 страницOpalesque NewManagers Sep 2012Peter UrbaniОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- POD For GS VIP Hedge Fund Indices (Q3 2012)Документ72 страницыPOD For GS VIP Hedge Fund Indices (Q3 2012)Peter UrbaniОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Portfolio POD VBAДокумент14 страницPortfolio POD VBAPeter Urbani100% (1)

- Risk Perspectives: What Is Risk? Its Measurement, Dimensions, Modeling (Asset Classes, Risk Factors and Regimes)Документ11 страницRisk Perspectives: What Is Risk? Its Measurement, Dimensions, Modeling (Asset Classes, Risk Factors and Regimes)Peter UrbaniОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Opalesque NewManagers July 2012Документ45 страницOpalesque NewManagers July 2012Peter UrbaniОценок пока нет

- Opalesque New Managers May 2012Документ51 страницаOpalesque New Managers May 2012Peter Urbani0% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Opalesque NewManagers Jun 2012Документ43 страницыOpalesque NewManagers Jun 2012Peter UrbaniОценок пока нет

- Opalesque New Managers April 2012Документ42 страницыOpalesque New Managers April 2012Peter UrbaniОценок пока нет

- Opalesque New Managers May 2012Документ51 страницаOpalesque New Managers May 2012Peter Urbani0% (1)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Performance of NZ Super Vs Avg. Australian SuperfundДокумент49 страницPerformance of NZ Super Vs Avg. Australian SuperfundPeter UrbaniОценок пока нет

- Do Emerging Managers Add Value (Mar 2012)Документ19 страницDo Emerging Managers Add Value (Mar 2012)Peter UrbaniОценок пока нет

- Opalesque New Managers Jan 2012Документ36 страницOpalesque New Managers Jan 2012Peter UrbaniОценок пока нет

- Emerging Manager Time Series DecompositionДокумент1 страницаEmerging Manager Time Series DecompositionPeter UrbaniОценок пока нет

- ETFdb Screening Model (March 2012)Документ507 страницETFdb Screening Model (March 2012)Peter UrbaniОценок пока нет

- Opalesque New Managers March 2012Документ37 страницOpalesque New Managers March 2012Peter UrbaniОценок пока нет

- Opalesque New Managers Feb 2012Документ37 страницOpalesque New Managers Feb 2012Peter UrbaniОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Why Distributions Matter (16 Jan 2012)Документ43 страницыWhy Distributions Matter (16 Jan 2012)Peter UrbaniОценок пока нет

- Unit-Ii Syllabus: Basic Elements in Solid Waste ManagementДокумент14 страницUnit-Ii Syllabus: Basic Elements in Solid Waste ManagementChaitanya KadambalaОценок пока нет

- Assignment November11 KylaAccountingДокумент2 страницыAssignment November11 KylaAccountingADRIANO, Glecy C.Оценок пока нет

- Module 7 NSTP 1Документ55 страницModule 7 NSTP 1PanJan BalОценок пока нет

- Domesticity and Power in The Early Mughal WorldДокумент17 страницDomesticity and Power in The Early Mughal WorldUjjwal Gupta100% (1)

- Chapter1 Intro To Basic FinanceДокумент28 страницChapter1 Intro To Basic FinanceRazel GopezОценок пока нет

- Advanced Herd Health Management, Sanitation and HygieneДокумент28 страницAdvanced Herd Health Management, Sanitation and Hygienejane entunaОценок пока нет

- PRESENTACIÒN EN POWER POINT Futuro SimpleДокумент5 страницPRESENTACIÒN EN POWER POINT Futuro SimpleDiego BenítezОценок пока нет

- MSCM Dormitory Housing WEB UpdateДокумент12 страницMSCM Dormitory Housing WEB Updatemax05XIIIОценок пока нет

- Abas Drug Study Nicu PDFДокумент4 страницыAbas Drug Study Nicu PDFAlexander Miguel M. AbasОценок пока нет

- Coke Drum Repair Welch Aquilex WSI DCU Calgary 2009Документ37 страницCoke Drum Repair Welch Aquilex WSI DCU Calgary 2009Oscar DorantesОценок пока нет

- CandyДокумент24 страницыCandySjdb FjfbОценок пока нет

- VRARAIДокумент12 страницVRARAIraquel mallannnaoОценок пока нет

- Fashion DatasetДокумент2 644 страницыFashion DatasetBhawesh DeepakОценок пока нет

- Landscape ArchitectureДокумент9 страницLandscape Architecturelisan2053Оценок пока нет

- Febrile Neutropenia GuidelineДокумент8 страницFebrile Neutropenia GuidelineAslesa Wangpathi PagehgiriОценок пока нет

- Communicating Value - PatamilkaДокумент12 страницCommunicating Value - PatamilkaNeha ArumallaОценок пока нет

- B-GL-385-009 Short Range Anti-Armour Weapon (Medium)Документ171 страницаB-GL-385-009 Short Range Anti-Armour Weapon (Medium)Jared A. Lang100% (1)

- Partnership Digest Obillos Vs CIRДокумент2 страницыPartnership Digest Obillos Vs CIRJeff Cadiogan Obar100% (9)

- Densha: Memories of A Train Ride Through Kyushu: By: Scott NesbittДокумент7 страницDensha: Memories of A Train Ride Through Kyushu: By: Scott Nesbittapi-16144421Оценок пока нет

- ACC030 Comprehensive Project April2018 (Q)Документ5 страницACC030 Comprehensive Project April2018 (Q)Fatin AkmalОценок пока нет

- MEMORANDUM OF AGREEMENT DraftsДокумент3 страницыMEMORANDUM OF AGREEMENT DraftsRichard Colunga80% (5)

- Data Science ProjectsДокумент3 страницыData Science ProjectsHanane GríssetteОценок пока нет

- Forensic IR-UV-ALS Directional Reflected Photography Light Source Lab Equipment OR-GZP1000Документ3 страницыForensic IR-UV-ALS Directional Reflected Photography Light Source Lab Equipment OR-GZP1000Zhou JoyceОценок пока нет

- The Marriage of Figaro LibrettoДокумент64 страницыThe Marriage of Figaro LibrettoTristan BartonОценок пока нет

- MegaMacho Drums BT READ MEДокумент14 страницMegaMacho Drums BT READ MEMirkoSashaGoggoОценок пока нет

- Measuring Road Roughness by Static Level Method: Standard Test Method ForДокумент6 страницMeasuring Road Roughness by Static Level Method: Standard Test Method ForDannyChaconОценок пока нет

- E-CRM Analytics The Role of Data Integra PDFДокумент310 страницE-CRM Analytics The Role of Data Integra PDFJohn JiménezОценок пока нет

- 8 X 56 M.-SCH.: Country of Origin: ATДокумент1 страница8 X 56 M.-SCH.: Country of Origin: ATMohammed SirelkhatimОценок пока нет

- Flipkart Labels 06 Jul 2022 09 52Документ37 страницFlipkart Labels 06 Jul 2022 09 52Dharmesh ManiyaОценок пока нет

- Ty Baf TaxationДокумент4 страницыTy Baf TaxationAkki GalaОценок пока нет