Вам также может понравиться

- Directions To New Delhi, Delhi 1,985 KM About 1 Da 5 Hours Loading..Документ9 страницDirections To New Delhi, Delhi 1,985 KM About 1 Da 5 Hours Loading..veloceteeОценок пока нет

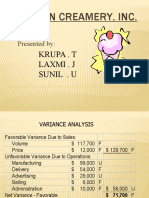

- Boston Creamery CaseДокумент9 страницBoston Creamery Caselion_heart3001100% (1)

- White Paper Summary Recent Trends in WarehousingДокумент8 страницWhite Paper Summary Recent Trends in WarehousingveloceteeОценок пока нет

- February: Ram Rahim Gurmeet SinghДокумент5 страницFebruary: Ram Rahim Gurmeet SinghveloceteeОценок пока нет

- Chapter 5 Restructuring Work and Organ Is at IonsДокумент5 страницChapter 5 Restructuring Work and Organ Is at IonsveloceteeОценок пока нет

- October13 Nov'9 ContractsДокумент1 страницаOctober13 Nov'9 ContractsveloceteeОценок пока нет

- Knowledge Management - Indian CompaniesДокумент13 страницKnowledge Management - Indian CompaniesTanmay AbhijeetОценок пока нет

- Contract LawДокумент73 страницыContract LawveloceteeОценок пока нет

- Chapter 5 Restructuring Work and Organ Is at IonsДокумент5 страницChapter 5 Restructuring Work and Organ Is at IonsveloceteeОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Financial Analysis of Pakistan State Oil For The Period July 2017-June 2020Документ25 страницFinancial Analysis of Pakistan State Oil For The Period July 2017-June 2020Adil IqbalОценок пока нет

- Customer Satisfaction Towards Investing Chits in KsfeДокумент41 страницаCustomer Satisfaction Towards Investing Chits in Ksfehariprasad kuloorОценок пока нет

- Part II Investment in Associate QuizДокумент2 страницыPart II Investment in Associate QuizSareta OblanОценок пока нет

- Financial Statement Analysis of ICICI BankДокумент31 страницаFinancial Statement Analysis of ICICI BankLipun baiОценок пока нет

- Ayub Khan Regime Presentation 1231862242284322 1Документ22 страницыAyub Khan Regime Presentation 1231862242284322 1Valentine FernandesОценок пока нет

- 4Q2022 ExternalCodeSets v1Документ266 страниц4Q2022 ExternalCodeSets v1yikega7894Оценок пока нет

- FinanceДокумент17 страницFinancejackie555Оценок пока нет

- Goldman Sachs Global Strategy Paper The Post Modern Cycle PositioningДокумент32 страницыGoldman Sachs Global Strategy Paper The Post Modern Cycle PositioningRoadtosuccessОценок пока нет

- Risk Management Topics in Indian BankingДокумент2 страницыRisk Management Topics in Indian Bankingmonabiswas100% (1)

- FerraroДокумент38 страницFerrarodaniela soto gОценок пока нет

- TFI InternationalДокумент43 страницыTFI InternationalJenny QuachОценок пока нет

- Boda Boda Business Plan: Sholinke Smart Boooda (SSB)Документ11 страницBoda Boda Business Plan: Sholinke Smart Boooda (SSB)omadiОценок пока нет

- CCI - Amazon OrderДокумент310 страницCCI - Amazon OrderRyan Denver MendesОценок пока нет

- Pairs Trading G GRДокумент31 страницаPairs Trading G GRSrinu BonuОценок пока нет

- EDP PR)Документ3 страницыEDP PR)02 - CM Ankita AdamОценок пока нет

- Case Study Analysis of Learning and Development at Tata MotorsДокумент5 страницCase Study Analysis of Learning and Development at Tata MotorsShanaya SinghaniyaОценок пока нет

- Financial Management-Important ConceptsДокумент7 страницFinancial Management-Important ConceptsPankaj YadavОценок пока нет

- The Economic Status of Indias Disinvested Central Public Sector EnterprisesДокумент8 страницThe Economic Status of Indias Disinvested Central Public Sector EnterprisesEditor IJTSRDОценок пока нет

- CFA - 6, 7 & 9. Financial Reporting and AnalysisДокумент3 страницыCFA - 6, 7 & 9. Financial Reporting and AnalysisChan Kwok WanОценок пока нет

- Blij - Back-Testing Magic - 2011Документ63 страницыBlij - Back-Testing Magic - 2011Jens GruОценок пока нет

- Analysis Slides-WACC NikeДокумент25 страницAnalysis Slides-WACC NikePei Chin100% (3)

- UMD Macro Exam 2 ReviewДокумент8 страницUMD Macro Exam 2 ReviewJames100% (1)

- SMEs - TOA - VALIX 2018 PDFДокумент17 страницSMEs - TOA - VALIX 2018 PDFHarvey Dienne Quiambao100% (1)

- Evaluation and Analysis of Financial InstitutionsДокумент2 страницыEvaluation and Analysis of Financial InstitutionsKhaireen Sofea Khairul NizamОценок пока нет

- Angeletos and Calvet 2006 JMEДокумент21 страницаAngeletos and Calvet 2006 JMEhoangpvrОценок пока нет

- Mindspace Business Parks REIT IPOДокумент4 страницыMindspace Business Parks REIT IPOKUNAL KISHOR SINGHОценок пока нет

- Course Code ME-325: Engineering EconomicsДокумент36 страницCourse Code ME-325: Engineering EconomicsGet-Set-GoОценок пока нет

- Cord 2013Документ92 страницыCord 2013charittasОценок пока нет

- Interview With Michael Hokensen, Asset ManagerДокумент5 страницInterview With Michael Hokensen, Asset ManagerWorldwide finance newsОценок пока нет

- Ambit - Strategy - ERr GRP - The Rebooting of IndiaДокумент25 страницAmbit - Strategy - ERr GRP - The Rebooting of Indiaomkarb87Оценок пока нет