Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Case Study 2 NutraSweetДокумент5 страницCase Study 2 NutraSweetRyan Kay50% (2)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Chapter 19 Test BankДокумент100 страницChapter 19 Test BankBrandon LeeОценок пока нет

- JPM Bitcoin ReportДокумент86 страницJPM Bitcoin ReportknwongabОценок пока нет

- Ch02 PRДокумент17 страницCh02 PRpks009Оценок пока нет

- Digital Marketing Strategy For New Product Launch - Russell MarketingДокумент8 страницDigital Marketing Strategy For New Product Launch - Russell MarketingRussell MarketingОценок пока нет

- Elliott Waves - Fibonacci Application Click-By-Click - Forex Indicators GuideДокумент1 страницаElliott Waves - Fibonacci Application Click-By-Click - Forex Indicators GuideAgape Cahaya100% (1)

- Company Analysis and Valuation Project PDFДокумент19 страницCompany Analysis and Valuation Project PDFAugusto LopezОценок пока нет

- The Transactions Listed Below Are Typical of Those Involving SouthernДокумент1 страницаThe Transactions Listed Below Are Typical of Those Involving SouthernTaimour HassanОценок пока нет

- Starbucks: Delivering Customer ServiceДокумент13 страницStarbucks: Delivering Customer ServiceMOHD SAHIL ZAIDIОценок пока нет

- South-Tek Systems Appoints Jens Bolleyer As CEOДокумент3 страницыSouth-Tek Systems Appoints Jens Bolleyer As CEOPR.comОценок пока нет

- Baydoun Willett (2000) Islamic Corporate Reports PDFДокумент20 страницBaydoun Willett (2000) Islamic Corporate Reports PDFAqilahAzmiОценок пока нет

- Behavioral Finance and Technical AnalysisДокумент28 страницBehavioral Finance and Technical AnalysisochirubaraОценок пока нет

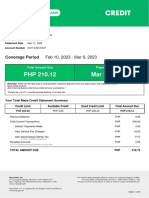

- MayaCredit SoA 2023MARДокумент2 страницыMayaCredit SoA 2023MARJan SaysonОценок пока нет

- Avon Products Inc - 2009Документ22 страницыAvon Products Inc - 2009Charisse L. SarateОценок пока нет

- Financial Reporting Week 4Документ9 страницFinancial Reporting Week 4islam hamdyОценок пока нет

- SCM TableДокумент5 страницSCM TableRed VelvetОценок пока нет

- Dse 05Документ3 страницыDse 05SharifMahmudОценок пока нет

- Chapter 29 ReviewДокумент18 страницChapter 29 ReviewTata NozadzeОценок пока нет

- Abid ResumeДокумент3 страницыAbid ResumeMohd Abid RazaОценок пока нет

- Costco Case Study and Strategic Analysis PDFДокумент11 страницCostco Case Study and Strategic Analysis PDFMaryam KhushbakhatОценок пока нет

- 1846635969Документ85 страниц1846635969Riadh RidhaОценок пока нет

- ConvergEx Traders Guide 2014 Q2 PDFДокумент166 страницConvergEx Traders Guide 2014 Q2 PDFthisthat7Оценок пока нет

- Arora's Cash Store - Business - PlanДокумент27 страницArora's Cash Store - Business - PlanmasroorОценок пока нет

- Marketing Reserach Paper II English VersionДокумент132 страницыMarketing Reserach Paper II English VersionMayukh.Оценок пока нет

- Qualities of A Successful Marketing ExecutiveДокумент2 страницыQualities of A Successful Marketing Executivesumith1990Оценок пока нет

- Aerari ProfileДокумент7 страницAerari ProfilemobinjabbarОценок пока нет

- Difference Between Sales and MarketingДокумент24 страницыDifference Between Sales and MarketingCYBER VILLA INTERNET CAFEОценок пока нет

- Competition Issues in India Mobile Handset IndustryДокумент96 страницCompetition Issues in India Mobile Handset Industryakshay shindeОценок пока нет

- Resource Allocation and Strategy Maritan2017Документ10 страницResource Allocation and Strategy Maritan2017crystalia diamondaОценок пока нет

- Vanguard VEAДокумент114 страницVanguard VEARaka AryawanОценок пока нет