Вам также может понравиться

- Analysis of India Cement LTD 2011Документ19 страницAnalysis of India Cement LTD 2011Kr Nishant100% (1)

- Shree CementДокумент30 страницShree Cementsushant_vjti17Оценок пока нет

- Ultra Tech Final 2007Документ16 страницUltra Tech Final 2007pvinayakamОценок пока нет

- India Cements Merges with Visaka CementДокумент5 страницIndia Cements Merges with Visaka CementAnkita AgarwalОценок пока нет

- Cement Industry Feasibility ReportДокумент4 страницыCement Industry Feasibility Reportds ww100% (1)

- Project Final - India CementsДокумент73 страницыProject Final - India Cementsabhisekparija86% (7)

- Prism Cement Investor Update May 2014Документ5 страницPrism Cement Investor Update May 2014abmahendruОценок пока нет

- Ompany Is Building A Waste Heat RecoveryДокумент1 страницаOmpany Is Building A Waste Heat RecoverypanjoshiОценок пока нет

- Financial PerformanceДокумент71 страницаFinancial PerformanceTshering Choden Lachungpa50% (2)

- Cement ProjectДокумент3 страницыCement ProjectPonnoju ShashankaОценок пока нет

- Maha Cements - Pon Pure Logistics by VenkatДокумент27 страницMaha Cements - Pon Pure Logistics by VenkatVenkata SubramanianОценок пока нет

- Madras Cements, Ltd.Документ24 страницыMadras Cements, Ltd.skkk kkkОценок пока нет

- India Cement (INDCEM) : Higher Prices Lead To Margin ExpansionДокумент11 страницIndia Cement (INDCEM) : Higher Prices Lead To Margin ExpansionumaganОценок пока нет

- RBSA Indian Cement Industry AnalysisДокумент18 страницRBSA Indian Cement Industry AnalysisPuneet Mathur100% (1)

- Cement 04102005Документ7 страницCement 04102005ShubinОценок пока нет

- B2B Assignment Section C Group 3Документ8 страницB2B Assignment Section C Group 3PON VINOTHANОценок пока нет

- Gujarat Ambuja Cost LeadershipДокумент27 страницGujarat Ambuja Cost Leadershipsurabhi vyasОценок пока нет

- Topic: Gujarat Ambuja Cost Leader in The Indian Cement Industry'Документ27 страницTopic: Gujarat Ambuja Cost Leader in The Indian Cement Industry'surabhi vyasОценок пока нет

- Cement Industry in India AnalysisДокумент13 страницCement Industry in India AnalysisSalma Pazhayillath50% (2)

- Malabar Cements Performance AppraisalДокумент92 страницыMalabar Cements Performance AppraisalDoraiBalamohan0% (1)

- Shree Cement's Growth in Cement and Power BusinessДокумент5 страницShree Cement's Growth in Cement and Power BusinessChandan AgarwalОценок пока нет

- Investor Update Oct 2012Документ5 страницInvestor Update Oct 2012abmahendruОценок пока нет

- Prism Cement Limited: Investor Update Feb 2014Документ5 страницPrism Cement Limited: Investor Update Feb 2014abmahendruОценок пока нет

- HR Project Report on Employee Perceptions of Performance AppraisalДокумент94 страницыHR Project Report on Employee Perceptions of Performance AppraisalNitesh ZendeОценок пока нет

- Birla Cement WorksДокумент71 страницаBirla Cement WorksrohittakОценок пока нет

- Indian Tyre Industry OutlookДокумент6 страницIndian Tyre Industry OutlookSundeep TariyalОценок пока нет

- Industry Background: Cement Industry in IndiaДокумент4 страницыIndustry Background: Cement Industry in IndiaShahib ZadОценок пока нет

- Directors Report 12 ACC CementsДокумент13 страницDirectors Report 12 ACC Cements9987303726Оценок пока нет

- Organizational Culture - Final ProjectДокумент85 страницOrganizational Culture - Final ProjectMBA19 DgvcОценок пока нет

- Introduction To The IndustryДокумент5 страницIntroduction To The Industrytarika88Оценок пока нет

- Welingkar WE Girls General MotorsДокумент10 страницWelingkar WE Girls General MotorsSmita NayakОценок пока нет

- Case: Hero Cements LTD (HCL) : BackgroundДокумент4 страницыCase: Hero Cements LTD (HCL) : BackgroundCH NAIR0% (1)

- G.S. Petropull Company (GSPC)Документ2 страницыG.S. Petropull Company (GSPC)HarshikaОценок пока нет

- Ambuja Cements Report - Market Size & Stock PerformanceДокумент5 страницAmbuja Cements Report - Market Size & Stock PerformanceBell BottleОценок пока нет

- Accenture 2016 Shareholder Letter10 K006Документ6 страницAccenture 2016 Shareholder Letter10 K006ziaa senОценок пока нет

- Shareholder Pattern: CEO's & Chairman's MessageДокумент2 страницыShareholder Pattern: CEO's & Chairman's MessageSohini DeyОценок пока нет

- Chettinad Cement Set for Strong Growth on Improving DemandДокумент9 страницChettinad Cement Set for Strong Growth on Improving Demandrajan10_kumar_805053Оценок пока нет

- Harish Kumar Shree Cement ReportДокумент87 страницHarish Kumar Shree Cement Reportrahulsogani123Оценок пока нет

- Binani Cement Research ReportДокумент11 страницBinani Cement Research ReportRinkesh25Оценок пока нет

- Acc Cement: 36.htmlДокумент8 страницAcc Cement: 36.htmlsiddharthgargОценок пока нет

- Cement Industry ResearchДокумент9 страницCement Industry ResearchSounakОценок пока нет

- SCL JaipurДокумент96 страницSCL JaipurPrateek DaveОценок пока нет

- Assignment: Macroeconomic & Business EnvironmentДокумент10 страницAssignment: Macroeconomic & Business EnvironmentHimanshu ShekharОценок пока нет

- A Case Study On Labour Unrest in Tata Cummins - Trainees On The StrikeДокумент11 страницA Case Study On Labour Unrest in Tata Cummins - Trainees On The StrikeIF387Оценок пока нет

- Supply Chain Management in The Cement IndustryДокумент8 страницSupply Chain Management in The Cement IndustryRamakrishna Reddy100% (1)

- Equity Valuation of ACC LTDДокумент12 страницEquity Valuation of ACC LTDAbhishek GuptaОценок пока нет

- Due Diligence Report Acc IndiaДокумент24 страницыDue Diligence Report Acc IndiaKishore KrishnaОценок пока нет

- India's $383.5 Billion Cement Industry OutlookДокумент2 страницыIndia's $383.5 Billion Cement Industry OutlookJobin DevasiaОценок пока нет

- Innovative Strategy For Launch of New Brand of Cement: A Case StudyДокумент8 страницInnovative Strategy For Launch of New Brand of Cement: A Case StudyAbay ShiferaОценок пока нет

- A Report On Swot Analysis and Pest Analysis of Birla GroupДокумент5 страницA Report On Swot Analysis and Pest Analysis of Birla Groupjustinlanger4100% (5)

- Cement Sector Result UpdatedДокумент27 страницCement Sector Result UpdatedAngel BrokingОценок пока нет

- Ejefas 27 05Документ14 страницEjefas 27 05Namrata SaxenaОценок пока нет

- Ibis Cement Directory 2020 SampleДокумент11 страницIbis Cement Directory 2020 SampleDINKER MAHAJANОценок пока нет

- Recruitment and Selection at Shree CementДокумент122 страницыRecruitment and Selection at Shree CementSmartydr100% (1)

- Comparative Analysis of Orient Cement With Other in Nasik DistrictДокумент39 страницComparative Analysis of Orient Cement With Other in Nasik DistrictKumar BhargavaОценок пока нет

- Auto slowdown deepens: Tata, Hero, Ashok Leyland halt production as job cuts riseДокумент3 страницыAuto slowdown deepens: Tata, Hero, Ashok Leyland halt production as job cuts risesiddharth vermaОценок пока нет

- Maruti Suzuki 16S517Документ6 страницMaruti Suzuki 16S517Himanshu JhaОценок пока нет

- Facilitating Power Trade in the Greater Mekong Subregion: Establishing and Implementing a Regional Grid CodeОт EverandFacilitating Power Trade in the Greater Mekong Subregion: Establishing and Implementing a Regional Grid CodeОценок пока нет

- FunctionalityДокумент17 страницFunctionalityKavipriya KarunakaranОценок пока нет

- Paper-Iii Commerce: Signature and Name of InvigilatorДокумент32 страницыPaper-Iii Commerce: Signature and Name of InvigilatorPankhuri VermaОценок пока нет

- UgcДокумент22 страницыUgcKavipriya Karunakaran33% (3)

- B - A - Tamil 3rd Year AY 2010 - 11Документ3 страницыB - A - Tamil 3rd Year AY 2010 - 11Kavipriya KarunakaranОценок пока нет

- Draftugcregulations 2009Документ86 страницDraftugcregulations 2009goldenphoenix1987Оценок пока нет

- D 0804 Paper IiДокумент16 страницD 0804 Paper IiAjay KumarОценок пока нет

- Anna University MBA Question PapersДокумент17 страницAnna University MBA Question PapersKavipriya KarunakaranОценок пока нет

- Team Communication Performance StrategiesДокумент10 страницTeam Communication Performance StrategiesKavipriya KarunakaranОценок пока нет

- 10th-SocialScience Part1Документ65 страниц10th-SocialScience Part1Kavipriya KarunakaranОценок пока нет

- TeamsДокумент27 страницTeamsKumar SiddharthaОценок пока нет

- Research DesignДокумент23 страницыResearch DesignKavipriya KarunakaranОценок пока нет

- Shades of RedДокумент2 страницыShades of RedKavipriya KarunakaranОценок пока нет

- 10th ScienceДокумент310 страниц10th ScienceAbishek BachanОценок пока нет

- Managing Groups and Teams EffectivelyДокумент35 страницManaging Groups and Teams EffectivelyKavipriya KarunakaranОценок пока нет

- Group - Discussion On 4 Dec1Документ20 страницGroup - Discussion On 4 Dec1Kavipriya KarunakaranОценок пока нет

- Meaning of EtiquetteДокумент5 страницMeaning of EtiquetteKavipriya KarunakaranОценок пока нет

- Our FounderДокумент19 страницOur FounderKavipriya KarunakaranОценок пока нет

- Wharton CareerMgt2Документ21 страницаWharton CareerMgt2DaSkepticОценок пока нет

- Budgetary Reforms and New Financial Management Initiatives - CRSundaramurtiДокумент61 страницаBudgetary Reforms and New Financial Management Initiatives - CRSundaramurtiKavipriya KarunakaranОценок пока нет

- HR Important QuestionsДокумент3 страницыHR Important QuestionsKavipriya KarunakaranОценок пока нет

- Aire Acondicionado Split Mural X Frig TK 10992786 TechsheetsupДокумент1 страницаAire Acondicionado Split Mural X Frig TK 10992786 TechsheetsupJOSE ANGEL VILLALOBOS JIMENEZОценок пока нет

- Human Rights ReportДокумент39 страницHuman Rights ReportBipin RethinОценок пока нет

- Feminine App SAULДокумент50 страницFeminine App SAULKОценок пока нет

- Railway Recruitment Board : Kolkata (RRB/Kolkata's Panel dated 07.01.2020Документ1 страницаRailway Recruitment Board : Kolkata (RRB/Kolkata's Panel dated 07.01.2020Firebrand iawinОценок пока нет

- Atp Program DetailsДокумент9 страницAtp Program DetailsAhmed BernoussiОценок пока нет

- Common Terminology in Wireless NetworksДокумент15 страницCommon Terminology in Wireless Networksabhishek4vishwakar-1Оценок пока нет

- Long-Term Finance OptionsДокумент21 страницаLong-Term Finance OptionsBhakti MehtaОценок пока нет

- Commerce F2 SampleДокумент30 страницCommerce F2 SampleMalcolm CharidzaОценок пока нет

- Cisco CCW Configuration User GuideДокумент102 страницыCisco CCW Configuration User GuideRoger RicciОценок пока нет

- Respecting diversity in the workplaceДокумент8 страницRespecting diversity in the workplaceJoannix V VillanuevaОценок пока нет

- Taking Sides EssayДокумент7 страницTaking Sides EssayJulie CaoОценок пока нет

- Halaqat Open Call Performance Residency 2022 - Final2023Документ3 страницыHalaqat Open Call Performance Residency 2022 - Final2023Sos DosОценок пока нет

- EMSC Enrollment Agreement EMT-BДокумент2 страницыEMSC Enrollment Agreement EMT-BUSCBISCОценок пока нет

- Boveda Espirituales EnglishДокумент11 страницBoveda Espirituales EnglishReynolds Larmore100% (4)

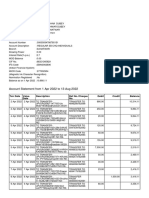

- Account Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент11 страницAccount Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceShubham TyagiОценок пока нет

- Strategic Hrm At Nestle BusinessДокумент9 страницStrategic Hrm At Nestle Businessvivi_15o689_11272315Оценок пока нет

- FYP SRS For E TailoringДокумент9 страницFYP SRS For E TailoringMuhammad SaqibОценок пока нет

- Engineering Economy: Cheerobie B. AranasДокумент27 страницEngineering Economy: Cheerobie B. AranasCllyan ReyesОценок пока нет

- SAP Changes S4HANA HCM SupportДокумент17 страницSAP Changes S4HANA HCM SupportMazen Al-RefaeiОценок пока нет

- Agirm Agn 4500210653 Itp 001 02 Kas3 Iso Seawater Strainer Forward Sea ChestДокумент6 страницAgirm Agn 4500210653 Itp 001 02 Kas3 Iso Seawater Strainer Forward Sea ChestRJS TUTORIALОценок пока нет

- Intelligent Assurance Smart Controls PDFДокумент31 страницаIntelligent Assurance Smart Controls PDFChristen CastilloОценок пока нет

- PancaratrasДокумент1 страницаPancaratrasAcyutánanda DasОценок пока нет

- Module 6 - Preparation of Financial StatementДокумент3 страницыModule 6 - Preparation of Financial StatementAngel Frankie RamosОценок пока нет

- Cambridge Assessment International Education: This Document Consists of 19 Printed PagesДокумент19 страницCambridge Assessment International Education: This Document Consists of 19 Printed Pagestecho2345Оценок пока нет

- Changing Names: Ussr Bulgaria Amnesty InternationalДокумент4 страницыChanging Names: Ussr Bulgaria Amnesty InternationalMete ÖzözgürОценок пока нет

- Regd. & Head Office: 3, Middleton Street, Kolkata-700 001 Address For Policy Issuing OfficeДокумент2 страницыRegd. & Head Office: 3, Middleton Street, Kolkata-700 001 Address For Policy Issuing OfficeNimesh ThakkarОценок пока нет

- Keithley September NewsletterДокумент6 страницKeithley September NewsletterwfbarnesОценок пока нет

- Lesson Sequence On TotemsДокумент7 страницLesson Sequence On Totemsapi-325835259Оценок пока нет

- Modern Approaches To Comparative Politics, Nature of Comparative PoliticsДокумент32 страницыModern Approaches To Comparative Politics, Nature of Comparative PoliticsGamer JiОценок пока нет

- Punishment Theories ExplainedДокумент39 страницPunishment Theories ExplainedAditya D TanwarОценок пока нет