Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Important Banking abbreviations and their full formsДокумент10 страницImportant Banking abbreviations and their full formsSivaChand DuggiralaОценок пока нет

- What Causes Small Businesses To FailДокумент11 страницWhat Causes Small Businesses To Failmounirs719883Оценок пока нет

- Project On SpicesДокумент96 страницProject On Spicesamitmanisha50% (6)

- Working Capital Managment ProjectДокумент48 страницWorking Capital Managment ProjectArun BhardwajОценок пока нет

- Del Monte Philippines, Inc. vs. AragoneДокумент1 страницаDel Monte Philippines, Inc. vs. AragoneLeizle Funa-FernandezОценок пока нет

- Bot ContractДокумент18 страницBot ContractideyОценок пока нет

- 9707 s11 Ms 22Документ6 страниц9707 s11 Ms 22kaviraj1006Оценок пока нет

- Synonym:, LED Flashlight, Multifunctional FlashlightДокумент1 страницаSynonym:, LED Flashlight, Multifunctional Flashlightkaviraj1006Оценок пока нет

- Sa Stein AccaДокумент4 страницыSa Stein AccaALIEVALIОценок пока нет

- 1.pilot Paper 1Документ21 страница1.pilot Paper 1Eugene MischenkoОценок пока нет

- f6 Uk SG 2013 PDFДокумент17 страницf6 Uk SG 2013 PDFkaviraj1006Оценок пока нет

- 7110 s05 QP 1Документ12 страниц7110 s05 QP 1kaviraj1006Оценок пока нет

- June 2005 o Level AccountingДокумент16 страницJune 2005 o Level Accountingkaviraj1006Оценок пока нет

- RFI Vs eRFIДокумент6 страницRFI Vs eRFITrade InterchangeОценок пока нет

- 10 Types of Entrepreneurial BMsДокумент36 страниц10 Types of Entrepreneurial BMsroshnisoni_sОценок пока нет

- Corporate ExcellenceДокумент14 страницCorporate ExcellenceJyoti WaindeshkarОценок пока нет

- Advantages and Disadvantages of Business Entity Types.Документ3 страницыAdvantages and Disadvantages of Business Entity Types.Kefayat Sayed AllyОценок пока нет

- Lectura 2 - Peterson Willie, Reinventing Strategy - Chapters 7,8, 2002Документ42 страницыLectura 2 - Peterson Willie, Reinventing Strategy - Chapters 7,8, 2002jv86Оценок пока нет

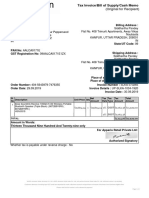

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Документ1 страницаTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Satyam SinghОценок пока нет

- ENY MRGN 016388 31012024 NSE DERV REM SignДокумент1 страницаENY MRGN 016388 31012024 NSE DERV REM Signycharansai0Оценок пока нет

- MQP For MBA I Semester Students of SPPUДокумент2 страницыMQP For MBA I Semester Students of SPPUfxn fndОценок пока нет

- Three Eras of Survey ResearchДокумент11 страницThree Eras of Survey ResearchGabriela IrrazabalОценок пока нет

- Case Study 7.5 SPMДокумент2 страницыCase Study 7.5 SPMgiscapindyОценок пока нет

- MM ZC441-L2Документ60 страницMM ZC441-L2Jayashree MaheshОценок пока нет

- Dendrite InternationalДокумент9 страницDendrite InternationalAbhishek VermaОценок пока нет

- Edmonton City Council Report On Downtown ArenaДокумент61 страницаEdmonton City Council Report On Downtown ArenaedmontonjournalОценок пока нет

- CV B Sahoo (AGM) 101121Документ4 страницыCV B Sahoo (AGM) 101121Benudhar SahooОценок пока нет

- Chapter-I: Customer Service and Loan Activities of Nepal Bank LimitedДокумент48 страницChapter-I: Customer Service and Loan Activities of Nepal Bank Limitedram binod yadavОценок пока нет

- Formato Casa de La Calidad (QFD)Документ11 страницFormato Casa de La Calidad (QFD)Diego OrtizОценок пока нет

- MCI BrochureДокумент7 страницMCI BrochureAndrzej M KotasОценок пока нет

- COA 018 Audit Checklist For Coal Operation Health and Safety Management Systems Field Audit2Документ42 страницыCOA 018 Audit Checklist For Coal Operation Health and Safety Management Systems Field Audit2sjarvis5Оценок пока нет

- Model Trading Standard ExplainedДокумент12 страницModel Trading Standard ExplainedVinca Grace SihombingОценок пока нет

- ENSP - Tender No.0056 - ENSP - DPE - AE - INV - 19 - Supply of A Truck Mounted Bundle ExtractorДокумент2 страницыENSP - Tender No.0056 - ENSP - DPE - AE - INV - 19 - Supply of A Truck Mounted Bundle ExtractorOussama AmaraОценок пока нет

- Ets 2021Документ4 страницыEts 2021Khang PhạmОценок пока нет

- Fractions Decimals and Percentages Word ProblemsДокумент4 страницыFractions Decimals and Percentages Word ProblemsMary Jane V. RamonesОценок пока нет

- HBO - Change Process, Managing ConflictДокумент12 страницHBO - Change Process, Managing ConflictHazel JumaquioОценок пока нет

- (Income Computation & Disclosure Standards) : Income in Light of IcdsДокумент25 страниц(Income Computation & Disclosure Standards) : Income in Light of IcdsEswarReddyEegaОценок пока нет