Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

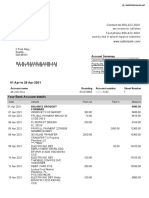

- Sutton Bank StatementДокумент2 страницыSutton Bank StatementNadiia AvetisianОценок пока нет

- CH 20Документ22 страницыCH 20sumihosaОценок пока нет

- CH 16Документ20 страницCH 16sumihosaОценок пока нет

- CH 21Документ20 страницCH 21sumihosaОценок пока нет

- CH 22Документ19 страницCH 22sumihosaОценок пока нет

- CH 19Документ23 страницыCH 19sumihosaОценок пока нет

- CH 15Документ24 страницыCH 15sumihosaОценок пока нет

- CH 12Документ23 страницыCH 12sumihosaОценок пока нет

- CH 14Документ20 страницCH 14sumihosaОценок пока нет

- Selecting and Optimal PortfolioДокумент16 страницSelecting and Optimal PortfoliosumihosaОценок пока нет

- CH 09Документ29 страницCH 09sumihosaОценок пока нет

- What To Know About Trading SecuritiesДокумент16 страницWhat To Know About Trading SecuritiessumihosaОценок пока нет

- What To Know About Trading SecuritiesДокумент16 страницWhat To Know About Trading SecuritiessumihosaОценок пока нет

- Diversification and Portfolio TheoryДокумент20 страницDiversification and Portfolio TheorysumihosaОценок пока нет

- Financial Assets Available To InvestorsДокумент22 страницыFinancial Assets Available To InvestorssumihosaОценок пока нет

- Investing in Mutual Funds and EtfsДокумент16 страницInvesting in Mutual Funds and EtfssumihosaОценок пока нет

- Investing in Mutual Funds and EtfsДокумент16 страницInvesting in Mutual Funds and EtfssumihosaОценок пока нет

- Financial Assets Available To InvestorsДокумент22 страницыFinancial Assets Available To InvestorssumihosaОценок пока нет

- Artifact5 Position PaperДокумент2 страницыArtifact5 Position Paperapi-377169218Оценок пока нет

- A Real Driver of US CHINA Trade ConflictДокумент8 страницA Real Driver of US CHINA Trade ConflictSabbir Hasan EmonОценок пока нет

- The Economist-Why Indonesia MattersДокумент3 страницыThe Economist-Why Indonesia Mattersdimas hasantriОценок пока нет

- What Are The Difference Between Governme PDFДокумент2 страницыWhat Are The Difference Between Governme PDFIndira IndiraОценок пока нет

- Infosys Case StudyДокумент2 страницыInfosys Case StudySumit Chopra100% (1)

- "Training and Action Research of Rural Development Academy (RDA), Bogra, Bangladesh." by Sheikh Md. RaselДокумент101 страница"Training and Action Research of Rural Development Academy (RDA), Bogra, Bangladesh." by Sheikh Md. RaselRasel89% (9)

- Algorithmic Market Making StrategiesДокумент34 страницыAlgorithmic Market Making Strategiessahand100% (1)

- Bank Interview QuestionsДокумент8 страницBank Interview Questionsfyod100% (1)

- India Timber Supply and Demand 2010-2030Документ64 страницыIndia Timber Supply and Demand 2010-2030Divyansh Rodney100% (1)

- Case Study 3 NirmaДокумент9 страницCase Study 3 NirmaPravin DhobleОценок пока нет

- Howe India Company ProfileДокумент62 страницыHowe India Company ProfileowngauravОценок пока нет

- Oceanic Wireless Vs CirДокумент6 страницOceanic Wireless Vs CirnazhОценок пока нет

- 9 Ekonomi Kesehatan MateriДокумент51 страница9 Ekonomi Kesehatan MaterialyunusОценок пока нет

- Core Complexities Bharat SyntheticsДокумент4 страницыCore Complexities Bharat SyntheticsRohit SharmaОценок пока нет

- Econometrics Assignment Summary and TableДокумент4 страницыEconometrics Assignment Summary and TableG Murtaza DarsОценок пока нет

- A Study On Customer Satisfaction Towards Idbi Fortis Life Insurance Company Ltd.Документ98 страницA Study On Customer Satisfaction Towards Idbi Fortis Life Insurance Company Ltd.Md MubashirОценок пока нет

- HR PoliciesДокумент129 страницHR PoliciesAjeet ThounaojamОценок пока нет

- Advanced Rohn Building Your Network Marketing1Документ31 страницаAdvanced Rohn Building Your Network Marketing1sk8ermarga267% (6)

- Tanzania Mortgage Market Update 2014Документ7 страницTanzania Mortgage Market Update 2014Anonymous FnM14a0Оценок пока нет

- Project Profile ON Roasted Rice FlakesДокумент7 страницProject Profile ON Roasted Rice FlakesPrafulla ChandraОценок пока нет

- The Role of Philanthropy or The Social ResponsibilityДокумент8 страницThe Role of Philanthropy or The Social ResponsibilityShikha Trehan100% (1)

- Neelam ReportДокумент86 страницNeelam Reportrjjain07100% (2)

- Voyage Accounting ExampleДокумент4 страницыVoyage Accounting Exampledharmawan100% (1)

- Contingent Liabilities For Philippines, by Tarun DasДокумент62 страницыContingent Liabilities For Philippines, by Tarun DasProfessor Tarun DasОценок пока нет

- Aid For TradeДокумент6 страницAid For TradeRajasekhar AllamОценок пока нет

- 2023 - Forecast George FriedmanДокумент17 страниц2023 - Forecast George FriedmanGeorge BestОценок пока нет

- Rivalry in The Eastern Mediterranean: The Turkish DimensionДокумент6 страницRivalry in The Eastern Mediterranean: The Turkish DimensionGerman Marshall Fund of the United StatesОценок пока нет

- Court of Tax Appeals First Division: Republic of The Philippines Quezon CityДокумент2 страницыCourt of Tax Appeals First Division: Republic of The Philippines Quezon CityPaulОценок пока нет

- MphasisДокумент2 страницыMphasisMohamed IbrahimОценок пока нет