Вам также может понравиться

- Dirty Boyz Issue 26Документ64 страницыDirty Boyz Issue 26Aguinaldo Family31% (32)

- Francisco vs. HerreraДокумент3 страницыFrancisco vs. Herreragen1Оценок пока нет

- IFM Notes 1Документ90 страницIFM Notes 1Tarini MohantyОценок пока нет

- Spices and Herbs UsesДокумент29 страницSpices and Herbs UsesBhavvesh JoshiОценок пока нет

- Forex Trading for Beginners: The Ultimate Trading Guide. Learn Successful Strategies to Buy and Sell in the Right Moment in the Foreign Exchange Market and Master the Right Mindset.От EverandForex Trading for Beginners: The Ultimate Trading Guide. Learn Successful Strategies to Buy and Sell in the Right Moment in the Foreign Exchange Market and Master the Right Mindset.Оценок пока нет

- Foreign Exchange Market: Dr. Amit Kumar SinhaДокумент67 страницForeign Exchange Market: Dr. Amit Kumar SinhaAmit SinhaОценок пока нет

- The Foreign Exchange MarketДокумент29 страницThe Foreign Exchange MarketSam Sep A Sixtyone100% (1)

- DPDP by KPMGДокумент19 страницDPDP by KPMGnidelel214Оценок пока нет

- Exchange RateДокумент32 страницыExchange RateCharlene Ann EbiteОценок пока нет

- Letter of CreditДокумент37 страницLetter of CreditMohammad A Yousef100% (1)

- Booking Number: FV86EA: PassengerДокумент1 страницаBooking Number: FV86EA: PassengerLe Cam NhanОценок пока нет

- English Stage 7 02 5RP AFP PDFДокумент8 страницEnglish Stage 7 02 5RP AFP PDFri.yax3365100% (8)

- Lecture 10-Foreign Exchange MarketДокумент42 страницыLecture 10-Foreign Exchange MarketfarahОценок пока нет

- Locked-In Range Analysis: Why Most Traders Must Lose Money in the Futures Market (Forex)От EverandLocked-In Range Analysis: Why Most Traders Must Lose Money in the Futures Market (Forex)Рейтинг: 1 из 5 звезд1/5 (1)

- Ibanez Vs PeopleДокумент2 страницыIbanez Vs PeopleEgo sum pulcher0% (1)

- Media ResearchДокумент53 страницыMedia Researchdeepak kumarОценок пока нет

- Forex 1Документ24 страницыForex 1Ashutosh Singh YadavОценок пока нет

- Wa0005.Документ5 страницWa0005.Kinza IqbalОценок пока нет

- Foreign Exchange MarketsДокумент25 страницForeign Exchange MarketsHimansh SagarОценок пока нет

- SPT, Cross, ForwardДокумент38 страницSPT, Cross, Forwardseagul_1183822Оценок пока нет

- Lecture Slides Chapter 11Документ22 страницыLecture Slides Chapter 11GuenazОценок пока нет

- 5 GoodДокумент19 страниц5 GoodNerea FrancesОценок пока нет

- The Study On Foreign ExchangeДокумент9 страницThe Study On Foreign ExchangeRs KailashОценок пока нет

- Kavita IbДокумент19 страницKavita IbKaranPatilОценок пока нет

- International Banking General Bank Management (Module-A)Документ39 страницInternational Banking General Bank Management (Module-A)Dhirendra Singh patwalОценок пока нет

- Forex Markets: International Finance - Group 3 Roll No-11, 16, 30, 45, 47, 58Документ34 страницыForex Markets: International Finance - Group 3 Roll No-11, 16, 30, 45, 47, 58Pradyumna SwainОценок пока нет

- International Business FinanceДокумент43 страницыInternational Business FinancesiusiuwidyantoОценок пока нет

- Unit I: Foreign Exchange Market & TransactionsДокумент31 страницаUnit I: Foreign Exchange Market & TransactionsAnkita DevnathОценок пока нет

- 3.1 Geographical Extent of The Foreign Exchange MarketДокумент8 страниц3.1 Geographical Extent of The Foreign Exchange MarketSharad BhorОценок пока нет

- Euro EconomyДокумент26 страницEuro EconomyJinal ShahОценок пока нет

- Foreign Exchange Markets: Prof Mahesh Kumar Amity Business SchoolДокумент47 страницForeign Exchange Markets: Prof Mahesh Kumar Amity Business SchoolasifanisОценок пока нет

- Currency Exchange Rates: 1 Usd 7 Yen 1USD 6 Yen Price/Base BDT/USD 85/1. 87/1, 83/1Документ31 страницаCurrency Exchange Rates: 1 Usd 7 Yen 1USD 6 Yen Price/Base BDT/USD 85/1. 87/1, 83/1mostakОценок пока нет

- Foreign Exchange MarketДокумент11 страницForeign Exchange MarketRahul Kumar AwadeОценок пока нет

- Market For Currency FuturesДокумент24 страницыMarket For Currency FuturesSharad SharmaОценок пока нет

- Multinational Financial Managment 07062022 015959pmДокумент21 страницаMultinational Financial Managment 07062022 015959pmShahbaz QureshiОценок пока нет

- Foreign Exchange RateДокумент3 страницыForeign Exchange RatesamchannuОценок пока нет

- Chapter 10Документ27 страницChapter 10trevorsum123Оценок пока нет

- Covered Interest Arbitrages IfmДокумент3 страницыCovered Interest Arbitrages IfmAshish MehraОценок пока нет

- Sample MCQsДокумент6 страницSample MCQsRubal GargОценок пока нет

- Forex PPTДокумент35 страницForex PPTRohan TrivediОценок пока нет

- CHAPTER 10 + Lecture: Foreign Exchange MarketДокумент68 страницCHAPTER 10 + Lecture: Foreign Exchange Marketradhika1991Оценок пока нет

- Chapter 7 - CompleteДокумент20 страницChapter 7 - Completemohsin razaОценок пока нет

- Forex (FX)Документ18 страницForex (FX)Vikram SinghОценок пока нет

- International PaymentДокумент28 страницInternational PaymentMayurRawoolОценок пока нет

- Trading Begins in The Asia-Pacific Region Followed by The Middle East, Europe, and AmericaДокумент5 страницTrading Begins in The Asia-Pacific Region Followed by The Middle East, Europe, and AmericaEzhilarasan AravendanОценок пока нет

- Unit 7 - Class SlidesДокумент57 страницUnit 7 - Class Slidessabelo.j.nkosi.5Оценок пока нет

- 02 EconomicsДокумент94 страницы02 EconomicsTecwyn LimОценок пока нет

- Done Motives For Using International Financial MarketsДокумент6 страницDone Motives For Using International Financial Marketskingsley Bill Owusu NinepenceОценок пока нет

- International FinanceДокумент34 страницыInternational FinanceabhibcbiОценок пока нет

- Forex Short NotesДокумент6 страницForex Short NotesClinton MutindaОценок пока нет

- Foreign Exchange MarketДокумент37 страницForeign Exchange MarketAkanksha MittalОценок пока нет

- CH 13Документ12 страницCH 13Simona NicolaeОценок пока нет

- TTQ-group 4Документ13 страницTTQ-group 4Phan ThọОценок пока нет

- Unit 2Документ15 страницUnit 2Aryan RajОценок пока нет

- Direct Quotations Can Be Converted Into Indirect Quotations and Vice VersaДокумент6 страницDirect Quotations Can Be Converted Into Indirect Quotations and Vice VersaLeo the BulldogОценок пока нет

- Internatinal Financial Markets, Rates and QuotesДокумент13 страницInternatinal Financial Markets, Rates and QuotesShivani Goyal100% (1)

- Introduction To DerivativesДокумент139 страницIntroduction To Derivativesnivedita_h42404Оценок пока нет

- Foreign Exchange MarketДокумент29 страницForeign Exchange MarketRavi SistaОценок пока нет

- Foreign Exchange ManagementДокумент2 страницыForeign Exchange ManagementobreroeldojohnОценок пока нет

- Foreign Currency RiskДокумент4 страницыForeign Currency RiskUsha KarkiОценок пока нет

- Investment Banking - F-D 97Документ139 страницInvestment Banking - F-D 97Sameer Sawant100% (1)

- FINM8007 PS1 AnswerДокумент4 страницыFINM8007 PS1 Answerqx62n6xxrkОценок пока нет

- Financial Markets and Institution: The Foreign Exchange MarketДокумент33 страницыFinancial Markets and Institution: The Foreign Exchange MarketDavid LeowОценок пока нет

- Foreign Exchange MarketДокумент37 страницForeign Exchange MarketMuneeb SahaniОценок пока нет

- 3-Forward ExchangeДокумент6 страниц3-Forward Exchangeyaseenjaved466Оценок пока нет

- Training and Development: Submitted By:-Amit KumarДокумент8 страницTraining and Development: Submitted By:-Amit KumarBhavvesh JoshiОценок пока нет

- Key Features of Successful Organisational Development, Professional Development and Improved Productivity Jon RoseДокумент4 страницыKey Features of Successful Organisational Development, Professional Development and Improved Productivity Jon RoseBhavvesh JoshiОценок пока нет

- Reservation: Availability. Below Is The Detailed Process of ReservationДокумент8 страницReservation: Availability. Below Is The Detailed Process of Reservationzaiby41Оценок пока нет

- Human Resource DevelopmentДокумент192 страницыHuman Resource DevelopmentShanmukh HallikeriОценок пока нет

- Wine Rates ListДокумент30 страницWine Rates ListBhavvesh Joshi67% (12)

- Emerging Indian Trade Regionalism (Trends & Prospects)Документ28 страницEmerging Indian Trade Regionalism (Trends & Prospects)Bhavvesh JoshiОценок пока нет

- Bhavesh Joshi: LogisticsДокумент14 страницBhavesh Joshi: LogisticsBhavvesh JoshiОценок пока нет

- Porsche AG: True To Brand?: - Presented by - Bhavesh JoshiДокумент9 страницPorsche AG: True To Brand?: - Presented by - Bhavesh JoshiBhavvesh JoshiОценок пока нет

- Primary Sources FinalДокумент2 страницыPrimary Sources Finalapi-203215781Оценок пока нет

- National Bank of Pakistan: Karachi (South) RegionДокумент6 страницNational Bank of Pakistan: Karachi (South) RegionAMIR4263Оценок пока нет

- CH03Документ3 страницыCH03Fuyiko Kaneshiro HosanaОценок пока нет

- NPFL - Rules - Professional - Players and Clubs in Nigeria Must Know - LawyardДокумент10 страницNPFL - Rules - Professional - Players and Clubs in Nigeria Must Know - LawyardOtito KoroОценок пока нет

- Quiz 2Документ2 страницыQuiz 2Zhaira Kim CantosОценок пока нет

- 2018LLB003 - DPC - Sem Vii - Research PaperДокумент16 страниц2018LLB003 - DPC - Sem Vii - Research PaperAishwarya BuddharajuОценок пока нет

- LTO Application To Deposit Plan - V18Документ1 страницаLTO Application To Deposit Plan - V18anjeeОценок пока нет

- RahulVansh - SS101 FALL MIDTERM EXAMДокумент2 страницыRahulVansh - SS101 FALL MIDTERM EXAMRahul VanshОценок пока нет

- E-Certificate For Participation in WebinarДокумент7 страницE-Certificate For Participation in Webinarjisha shajiОценок пока нет

- Prevention of Corruption Act, 1988Документ7 страницPrevention of Corruption Act, 1988Ashish BilolikarОценок пока нет

- Company Law ProjectДокумент6 страницCompany Law ProjectAyushi JaryalОценок пока нет

- People v. Yanson-DumancasДокумент20 страницPeople v. Yanson-DumancasBea MarañonОценок пока нет

- Short Texts On MasculinityДокумент6 страницShort Texts On Masculinityapi-522679657Оценок пока нет

- 10Документ4 страницы10Rosario BacaniОценок пока нет

- SONG BOK YOONG V HO KIM POUIДокумент2 страницыSONG BOK YOONG V HO KIM POUIAinul Mardiah bt HasnanОценок пока нет

- Information Sheet Motorcycle Helmets Visors and Goggles Aug 10Документ4 страницыInformation Sheet Motorcycle Helmets Visors and Goggles Aug 10HANIFОценок пока нет

- Hindu Marriage Act, 1955Документ20 страницHindu Marriage Act, 1955Prashant MishraОценок пока нет

- Z102 - C2-Convencia Cívica PDFДокумент35 страницZ102 - C2-Convencia Cívica PDFLuciana PintoОценок пока нет

- Encrypt SignedfinalДокумент2 страницыEncrypt SignedfinalRamОценок пока нет

- 2023-01-26 St. Mary's County TimesДокумент32 страницы2023-01-26 St. Mary's County TimesSouthern Maryland OnlineОценок пока нет

- Risk Management Approach For Testing and Calibration Laboratories - SpringerLinkДокумент8 страницRisk Management Approach For Testing and Calibration Laboratories - SpringerLinkrobert borgОценок пока нет

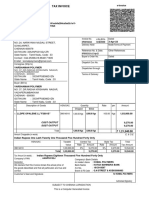

- Tax InvoiceДокумент2 страницыTax InvoiceTechnetОценок пока нет