Вам также может понравиться

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- MCDДокумент65 страницMCDFrancisco Javier CazaresОценок пока нет

- Introduction To Layers of Earth's Atmosphere: Presented by Abhishek RaveendranДокумент10 страницIntroduction To Layers of Earth's Atmosphere: Presented by Abhishek RaveendranAbhishek RaveendranОценок пока нет

- Investment Banking OverviewДокумент8 страницInvestment Banking OverviewAbhishek RaveendranОценок пока нет

- The Management Environment: LIS 580: Spring 2006 Instructor-Michael CrandallДокумент22 страницыThe Management Environment: LIS 580: Spring 2006 Instructor-Michael CrandallAbhishek RaveendranОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Discounting and Unwinding: Answer 2-No, Deferred Consideration Is Not A Contingent Consideration Because It Does NotДокумент5 страницDiscounting and Unwinding: Answer 2-No, Deferred Consideration Is Not A Contingent Consideration Because It Does NotM Azeem IqbalОценок пока нет

- BRS Practice QuestionsДокумент2 страницыBRS Practice Questionssyed ali raza kazmiОценок пока нет

- Pas 40 Investment PropertyДокумент4 страницыPas 40 Investment PropertykristineОценок пока нет

- Investment Banks: Financial InstitutionsДокумент3 страницыInvestment Banks: Financial Institutionsruthmae bumanglagОценок пока нет

- Banking VocabularyДокумент3 страницыBanking Vocabularytahar benattiaОценок пока нет

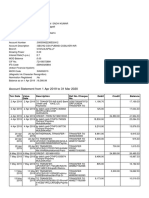

- Account Statement From 1 Apr 2019 To 31 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент7 страницAccount Statement From 1 Apr 2019 To 31 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSadhi KumarОценок пока нет

- G12 Fabm2 Week 8Документ11 страницG12 Fabm2 Week 8Whyljyne GlasanayОценок пока нет

- RBI Format ROI PC PDFДокумент9 страницRBI Format ROI PC PDFmohana sundaram pОценок пока нет

- Receivable-Financing-Quizbowl DONE For CpaДокумент30 страницReceivable-Financing-Quizbowl DONE For CpaKae Abegail GarciaОценок пока нет

- CFP Risk Analysis and Insurance Planning Practice Book SampleДокумент34 страницыCFP Risk Analysis and Insurance Planning Practice Book SampleMeenakshi100% (7)

- ADV ACC TBch03Документ18 страницADV ACC TBch03hassan nassereddineОценок пока нет

- Chapter 6: Accounting For Plant Assets and Depreciation. ContentsДокумент46 страницChapter 6: Accounting For Plant Assets and Depreciation. ContentsSimon MollaОценок пока нет

- Sbaa7001 Banking and Insurance Management II MBA - BATCH (2019-2021) Semester Iii - August 2020 School of Management StudiesДокумент38 страницSbaa7001 Banking and Insurance Management II MBA - BATCH (2019-2021) Semester Iii - August 2020 School of Management StudiesGracyОценок пока нет

- Verotel Merchant Services B.V. v. Rizal Commercial Bank 2021Документ90 страницVerotel Merchant Services B.V. v. Rizal Commercial Bank 2021hyenadogОценок пока нет

- Coding and Decoding QuestionsДокумент28 страницCoding and Decoding QuestionsAbdulawwal IntisorОценок пока нет

- Question 2: Ias 19 Employee Benefits: Page 1 of 2Документ2 страницыQuestion 2: Ias 19 Employee Benefits: Page 1 of 2paul sagudaОценок пока нет

- Completing The Accounting Cycle: Service Concern: Subject-Descriptive Title Subject - CodeДокумент12 страницCompleting The Accounting Cycle: Service Concern: Subject-Descriptive Title Subject - CodeRose LaureanoОценок пока нет

- Zenith Bank Statement Ronald Morris For Dec 20TH To 22ND 2023Документ2 страницыZenith Bank Statement Ronald Morris For Dec 20TH To 22ND 2023Emeka AmaliriОценок пока нет

- A Mba Lo SurrenderДокумент6 страницA Mba Lo SurrenderGabe AmbaloОценок пока нет

- Pulse TNC Booklet CombinedffdДокумент62 страницыPulse TNC Booklet CombinedffdRrdОценок пока нет

- A Comparative Analysis of Financial Products in Banking Industry With Special Reference To ICICI Bank and State Bank of IndiaДокумент98 страницA Comparative Analysis of Financial Products in Banking Industry With Special Reference To ICICI Bank and State Bank of IndiaWhatsapp stutsОценок пока нет

- Chapter 13 - Financial Asset at Fair ValueДокумент10 страницChapter 13 - Financial Asset at Fair ValueMark LopezОценок пока нет

- Assignment, Managerial AccountingДокумент8 страницAssignment, Managerial Accountingmariamreda7754Оценок пока нет

- 25885110Документ21 страница25885110Llyana paula SuyuОценок пока нет

- 1) Introduction To Management Accounting-2Документ34 страницы1) Introduction To Management Accounting-2fpasanfiverОценок пока нет

- Ba Smart Jul-AprДокумент68 страницBa Smart Jul-AprShubham KashyapОценок пока нет

- PF PFi Terms and ConditionsДокумент20 страницPF PFi Terms and ConditionsAzeizulОценок пока нет

- Income Statement - ExДокумент14 страницIncome Statement - ExQuân Uông Đình MinhОценок пока нет

- Star PREMIUM CHART 18%Документ5 страницStar PREMIUM CHART 18%Rajat GuptaОценок пока нет

- Chap 009Документ30 страницChap 009Ngọc Lan Anh TrầnОценок пока нет