Вам также может понравиться

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Nuguid Vs NuguidДокумент1 страницаNuguid Vs NuguidParis ValenciaОценок пока нет

- Diagnostic Test Phil - PoliticsДокумент8 страницDiagnostic Test Phil - PoliticsWizly Von Ledesma TanduyanОценок пока нет

- Form - Xxvi: Department of Commercial Taxes, Government of Uttar PradeshДокумент14 страницForm - Xxvi: Department of Commercial Taxes, Government of Uttar PradeshmgrfaОценок пока нет

- Transfer Payment AgreementДокумент18 страницTransfer Payment AgreementGrant LaFlecheОценок пока нет

- Wasco Lindung SDN BHD V Lustre Metals & Minerals SDN BHD (2015) 9 MLJ 610Документ22 страницыWasco Lindung SDN BHD V Lustre Metals & Minerals SDN BHD (2015) 9 MLJ 610Sari ManiraОценок пока нет

- Presentation On succession-JCJ-VMDДокумент9 страницPresentation On succession-JCJ-VMDajitlimayeОценок пока нет

- Payment Agreement: SampleДокумент3 страницыPayment Agreement: SampleAmirul Amin IVОценок пока нет

- Loyola International School Al-Nasr CampusДокумент1 страницаLoyola International School Al-Nasr CampusamirОценок пока нет

- GP Fund Calculation Formula Sheet For GP Fund StatementДокумент4 страницыGP Fund Calculation Formula Sheet For GP Fund StatementLucky KhanОценок пока нет

- Pacific Farms, Inc. v. Esguerra 30 SCRA 684 (1969)Документ22 страницыPacific Farms, Inc. v. Esguerra 30 SCRA 684 (1969)vincent gianОценок пока нет

- Del Castillo Vs Torrecampo - G.R. No. 139033 - Dec 18, 2002Документ4 страницыDel Castillo Vs Torrecampo - G.R. No. 139033 - Dec 18, 2002Boogie San JuanОценок пока нет

- 1st Year For Project Topics-1Документ4 страницы1st Year For Project Topics-1Clashin FashОценок пока нет

- Local Implementation Contract in Relation To The Master Contract For The Supply of Services #TGP CTR - 054478 - Haccp Audits & Microbiological TestsДокумент12 страницLocal Implementation Contract in Relation To The Master Contract For The Supply of Services #TGP CTR - 054478 - Haccp Audits & Microbiological TestsMaria Fernanda ValderramaОценок пока нет

- 3 Pomeroy Treatise On Equity Jurisprudence 1918 Cropped 165 Pages TrustsДокумент165 страниц3 Pomeroy Treatise On Equity Jurisprudence 1918 Cropped 165 Pages Trustsmaliklaw100% (2)

- Labour Rights and The Constitution: Law Academic Twice Winner of UCT Book PrizeДокумент12 страницLabour Rights and The Constitution: Law Academic Twice Winner of UCT Book PrizeXolani MpilaОценок пока нет

- ChrisДокумент5 страницChrisDpОценок пока нет

- Islamic LawДокумент1 страницаIslamic LawAnonymous OGuQXU8vDОценок пока нет

- Estacode 2019Документ1 043 страницыEstacode 2019Abubakar Zubair100% (4)

- Basics of GST: Partners: CA Arvind Saraf CA Ritu Agarwal CA Atul MehtaДокумент67 страницBasics of GST: Partners: CA Arvind Saraf CA Ritu Agarwal CA Atul MehtaRagnor LordbrookОценок пока нет

- 2023 - 005 LGU Mayor PERMIT BENEFIT DANCEДокумент1 страница2023 - 005 LGU Mayor PERMIT BENEFIT DANCEbarangaybingayОценок пока нет

- Piano Concerto No 2 in F MinorДокумент3 страницыPiano Concerto No 2 in F MinorJacek PyzikОценок пока нет

- Film Art An Introduction 10Th Edition Bordwell Test Bank Full Chapter PDFДокумент30 страницFilm Art An Introduction 10Th Edition Bordwell Test Bank Full Chapter PDFDeborahWestwdzt100% (9)

- Pending Payments: Issuance Work Permit For 2 Year Outside The Country - SkillДокумент1 страницаPending Payments: Issuance Work Permit For 2 Year Outside The Country - SkillHasnain proОценок пока нет

- STFAP Bracket B CertificationДокумент1 страницаSTFAP Bracket B CertificationlabellejolieОценок пока нет

- SAMED v. SEGUTAMBYДокумент20 страницSAMED v. SEGUTAMBYBinendriОценок пока нет

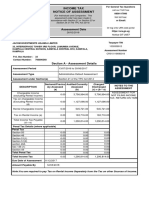

- Assessment Date: Income Tax Notice of AssessmentДокумент2 страницыAssessment Date: Income Tax Notice of AssessmentBwana KuubwaОценок пока нет

- CIR vs. Avon Products - CTA Jurisdiction - Due Process - FAN Requisites - LeonenДокумент85 страницCIR vs. Avon Products - CTA Jurisdiction - Due Process - FAN Requisites - LeonenVictoria aytonaОценок пока нет

- Final House Report - John Swallow InvestigationДокумент214 страницFinal House Report - John Swallow InvestigationThe Salt Lake TribuneОценок пока нет

- BL3 Lec 5Документ29 страницBL3 Lec 5Sanwar BajadОценок пока нет

- Assessment 7 - SJD1501Документ9 страницAssessment 7 - SJD1501Chun LiОценок пока нет