Вам также может понравиться

- HCMДокумент17 страницHCMJim MathilakathuОценок пока нет

- Scheme & Syllabus For PHD Entrance Test in ManagementДокумент8 страницScheme & Syllabus For PHD Entrance Test in ManagementDar UbeasОценок пока нет

- O M 2 .2production Planning and ControlДокумент26 страницO M 2 .2production Planning and ControlJim MathilakathuОценок пока нет

- OM2.1plant Location and LytДокумент66 страницOM2.1plant Location and LytJim MathilakathuОценок пока нет

- Functions of The Handling SystemДокумент51 страницаFunctions of The Handling SystemJim MathilakathuОценок пока нет

- Finanacial Restructuring 2Документ48 страницFinanacial Restructuring 2Jim Mathilakathu100% (2)

- OM 2. 4inventorycontroДокумент26 страницOM 2. 4inventorycontroJim MathilakathuОценок пока нет

- Business Ethics 2333Документ15 страницBusiness Ethics 2333Jim MathilakathuОценок пока нет

- Dividends and Dividend PolicyДокумент24 страницыDividends and Dividend Policyfalak_praveen4928Оценок пока нет

- Aggregate Production PlanningДокумент27 страницAggregate Production PlanningJim MathilakathuОценок пока нет

- Supply Chain ManagementДокумент76 страницSupply Chain Managementsreejith_eimt13Оценок пока нет

- Operations ResearchДокумент1 страницаOperations ResearchJim MathilakathuОценок пока нет

- SHR PlanningДокумент21 страницаSHR PlanningJim MathilakathuОценок пока нет

- Exchange Rate RegimeДокумент5 страницExchange Rate RegimeNaman DugarОценок пока нет

- Economis and GovernmentДокумент63 страницыEconomis and GovernmentJim MathilakathuОценок пока нет

- Aggregate Production Planning - Lecture NotesДокумент16 страницAggregate Production Planning - Lecture NotesJim Mathilakathu100% (1)

- Financial Accounting RWДокумент592 страницыFinancial Accounting RWJim MathilakathuОценок пока нет

- Consumer Protection Act GahlotДокумент21 страницаConsumer Protection Act GahlotSwati KamtheОценок пока нет

- Tender Pricing StrategyДокумент35 страницTender Pricing StrategyWan Hakim Wan Yaacob0% (1)

- 3 Impact of Reforms in Capital Market On Indian Capital MarketДокумент29 страниц3 Impact of Reforms in Capital Market On Indian Capital MarketJim MathilakathuОценок пока нет

- Caion-Demaestri Freedberg OverpopulationpresentationДокумент21 страницаCaion-Demaestri Freedberg OverpopulationpresentationJim MathilakathuОценок пока нет

- Time StudyДокумент40 страницTime StudySazid Rahman100% (1)

- Einstein 10 LessonsДокумент26 страницEinstein 10 LessonsKrishnamurthy Prabhakar100% (1)

- 42 AmalgamationДокумент10 страниц42 AmalgamationRoopa RoyОценок пока нет

- ERV English Bible 20 ProverbsДокумент21 страницаERV English Bible 20 ProverbsJim MathilakathuОценок пока нет

- Public FinnceДокумент57 страницPublic FinnceJim MathilakathuОценок пока нет

- And Budget Management (FRBM) Bill in December 2000. in This Bill Numerical Targets ForДокумент11 страницAnd Budget Management (FRBM) Bill in December 2000. in This Bill Numerical Targets ForJim MathilakathuОценок пока нет

- GFHДокумент1 страницаGFHJim MathilakathuОценок пока нет

- Monetary PolicyДокумент24 страницыMonetary PolicySwati AgarwalОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Tulip Mania ScriptДокумент7 страницTulip Mania ScriptafzalkhanОценок пока нет

- Valuation of SAIF POWERTEC Limited: Analysis of Financial Investment Course Code: F-307Документ23 страницыValuation of SAIF POWERTEC Limited: Analysis of Financial Investment Course Code: F-307Farzana Fariha LimaОценок пока нет

- Exercise 1 WaccДокумент1 страницаExercise 1 WaccGazelle CalmaОценок пока нет

- Unit 2: Indian Accounting Standard 33: Earnings Per Share: After Studying This Unit, You Will Be Able ToДокумент56 страницUnit 2: Indian Accounting Standard 33: Earnings Per Share: After Studying This Unit, You Will Be Able ToAudit MarathonОценок пока нет

- Arbor Final ReportДокумент17 страницArbor Final Reportapi-583299179Оценок пока нет

- Investor's Perception Towards The Reliance Mutual FundsДокумент83 страницыInvestor's Perception Towards The Reliance Mutual FundsmanuОценок пока нет

- Chapter 13Документ11 страницChapter 13MekeniMekeniОценок пока нет

- Mutual Funds: Answer Role of Mutual Funds in The Financial Market: Mutual Funds Have Opened New Vistas ToДокумент43 страницыMutual Funds: Answer Role of Mutual Funds in The Financial Market: Mutual Funds Have Opened New Vistas ToNidhi Kaushik100% (1)

- Sources of Financing A ProjectДокумент8 страницSources of Financing A ProjectAbhijith PaiОценок пока нет

- Share Structure QuestionsДокумент18 страницShare Structure QuestionsmikiОценок пока нет

- 06 - Raising Equity CapitalДокумент46 страниц06 - Raising Equity CapitalAnurag PattekarОценок пока нет

- Adeel BMДокумент27 страницAdeel BMttsopalОценок пока нет

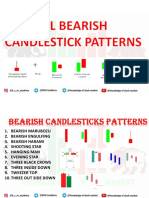

- All Bearish Candle Stick PatternsДокумент18 страницAll Bearish Candle Stick PatternsxhghdghОценок пока нет

- John Robert Maniego (CV)Документ2 страницыJohn Robert Maniego (CV)Youcan B StreetsmartОценок пока нет

- Uncertainty and Consumer BehaviorДокумент118 страницUncertainty and Consumer BehaviorPhuong TaОценок пока нет

- 358763050Документ15 страниц358763050kristelle0marisseОценок пока нет

- The Magic of Pension Accounting, Part IIIДокумент160 страницThe Magic of Pension Accounting, Part IIIMUNAWAR ALIОценок пока нет

- List of Valuation ReportsДокумент18 страницList of Valuation ReportsBhavin SagarОценок пока нет

- Acturial AnalysisДокумент14 страницActurial AnalysisRISHAB NANGIAОценок пока нет

- Chapter1 - Return CalculationsДокумент37 страницChapter1 - Return CalculationsChris CheungОценок пока нет

- Laporan Keuangan Nasi LiwetДокумент116 страницLaporan Keuangan Nasi Liwetnirmaya esthiОценок пока нет

- 0205 ReposedДокумент45 страниц0205 ReposedLameuneОценок пока нет

- Risk ManagementДокумент21 страницаRisk ManagementAndreeaEne100% (2)

- Ev Standard AnalyticsДокумент7 страницEv Standard AnalyticsDavid ShapiroОценок пока нет

- Goldman Sachs Risk Management: November 17 2010 Presented By: Ken Forsyth Jeremy Poon Jamie MacdonaldДокумент109 страницGoldman Sachs Risk Management: November 17 2010 Presented By: Ken Forsyth Jeremy Poon Jamie MacdonaldPol BernardinoОценок пока нет

- Introduction To Security MarketДокумент41 страницаIntroduction To Security MarketdeeptiОценок пока нет

- David Hillier (2019)Документ12 страницDavid Hillier (2019)eriwirandanaОценок пока нет

- HW 1, FIN 604, Sadhana JoshiДокумент40 страницHW 1, FIN 604, Sadhana JoshiSadhana JoshiОценок пока нет

- Free Mock For Jaiib & CaiibДокумент6 страницFree Mock For Jaiib & CaiibsandeepОценок пока нет

- Business Incubation CenterДокумент40 страницBusiness Incubation CenterFati ma100% (1)