Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Bill of ExchangeДокумент4 страницыBill of ExchangeSara SanamОценок пока нет

- SPA For SellersДокумент23 страницыSPA For Sellersพิมพ์ วิมุกตะลพ100% (2)

- Credit Appraisal Process of Axis BankДокумент112 страницCredit Appraisal Process of Axis Bankpujanswetal60% (5)

- FOB Barge MasterДокумент19 страницFOB Barge MasterMarco HandokoОценок пока нет

- Case 12-6Документ5 страницCase 12-6Umar Dhani100% (1)

- Chapter 23 - City of Miami OrdinanceДокумент11 страницChapter 23 - City of Miami Ordinanceal_crespoОценок пока нет

- General Awareness Questions Asked in RBI Grade B' 2016 - Shift IДокумент9 страницGeneral Awareness Questions Asked in RBI Grade B' 2016 - Shift IAbhishek SoniОценок пока нет

- Complete Exam Analysis of Bank of Maharashtra Clerk 2016Документ1 страницаComplete Exam Analysis of Bank of Maharashtra Clerk 2016Abhishek SoniОценок пока нет

- Number Series 264Документ22 страницыNumber Series 264Abhishek Soni100% (3)

- Roti Reminder' A Hit For Lifebuoy During Kumbh: Wash Reminder On 2.5 Million RotisДокумент10 страницRoti Reminder' A Hit For Lifebuoy During Kumbh: Wash Reminder On 2.5 Million RotisAbhishek SoniОценок пока нет

- 001 BPI V de RenyДокумент2 страницы001 BPI V de RenyPatrick ManaloОценок пока нет

- Letter of Credit ProcedureДокумент4 страницыLetter of Credit ProcedureKarthickDevanОценок пока нет

- The Commercial Letter of Credit Final NA TALAGAДокумент27 страницThe Commercial Letter of Credit Final NA TALAGAMaricar SalameñaОценок пока нет

- 350exi-Q22659 00Документ24 страницы350exi-Q22659 00Jack YangОценок пока нет

- Banking Assignment 3Документ5 страницBanking Assignment 3Rida KhanОценок пока нет

- Mercantile Law PDFДокумент15 страницMercantile Law PDFThe Supreme Court Public Information Office33% (3)

- Merc Law MT Suggested Answers - 146991554Документ9 страницMerc Law MT Suggested Answers - 146991554Francis Louie Allera HumawidОценок пока нет

- CC Unit 5, Orders and Cover Letters of OrdersДокумент36 страницCC Unit 5, Orders and Cover Letters of OrdersReikoAiОценок пока нет

- 1.S. Introduction To I.PДокумент20 страниц1.S. Introduction To I.PHoàng Lan Lê TrầnОценок пока нет

- Chapter 13 Exporting, Importing, and CountertradeДокумент7 страницChapter 13 Exporting, Importing, and CountertradeThế TùngОценок пока нет

- Tender IP Based CCTV Surveillance System PDFДокумент162 страницыTender IP Based CCTV Surveillance System PDFakhilОценок пока нет

- Documentary Credit ApplicationДокумент4 страницыDocumentary Credit ApplicationThanh HuyenОценок пока нет

- BPI vs. de RenyДокумент1 страницаBPI vs. de RenyVanya Klarika NuqueОценок пока нет

- Loans and AdvancesДокумент49 страницLoans and Advancesravi kangneОценок пока нет

- Export Finance ProjectДокумент67 страницExport Finance ProjectVinay Singh67% (3)

- Import ProcurementДокумент23 страницыImport ProcurementGirish Raj100% (1)

- Standby Letters of Credit - A Comprehensive Guide (Finance and Capital Markets) (PDFDrive)Документ251 страницаStandby Letters of Credit - A Comprehensive Guide (Finance and Capital Markets) (PDFDrive)Trey NgugiОценок пока нет

- BFSiДокумент70 страницBFSisayanuchatterjee4Оценок пока нет

- DGM GS-3 + SS8 - 201901Документ19 страницDGM GS-3 + SS8 - 201901LeTruongОценок пока нет

- ADR CaseДокумент22 страницыADR Casezimm potОценок пока нет

- Indian Institute of Banking & FinanceДокумент14 страницIndian Institute of Banking & Financekarthik100% (1)

- Siri Mba Final ProjectДокумент56 страницSiri Mba Final Projectjunkie333Оценок пока нет

- Methods of PaymentДокумент5 страницMethods of PaymentJoeina MathewОценок пока нет

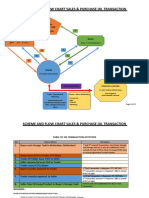

- FINAL - REVISED. Scheme and Flow Chart OIL TransactionДокумент4 страницыFINAL - REVISED. Scheme and Flow Chart OIL TransactionPebb PondОценок пока нет