Вам также может понравиться

- Verbal Communication: Presented By: Antra SinghДокумент27 страницVerbal Communication: Presented By: Antra SinghSudhir Kumar YadavОценок пока нет

- A Definition of AdvertisingДокумент11 страницA Definition of AdvertisingSudhir Kumar YadavОценок пока нет

- By Anurag Verma Pramod Pal Aushi Singhal Raghuvendra SinghДокумент15 страницBy Anurag Verma Pramod Pal Aushi Singhal Raghuvendra SinghSudhir Kumar YadavОценок пока нет

- Industrial PolicyДокумент16 страницIndustrial PolicySudhir Kumar YadavОценок пока нет

- Ifci 2Документ10 страницIfci 2Sudhir Kumar YadavОценок пока нет

- Share Capital: Equity Capital Preference CapitalДокумент12 страницShare Capital: Equity Capital Preference CapitalSudhir Kumar YadavОценок пока нет

- Non Verbal Communication FinalДокумент18 страницNon Verbal Communication FinalSudhir Kumar YadavОценок пока нет

- Options Futures and DerivativesДокумент33 страницыOptions Futures and DerivativesSudhir Kumar YadavОценок пока нет

- Fera and Fema2Документ31 страницаFera and Fema2Sudhir Kumar YadavОценок пока нет

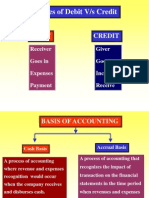

- Debit & CreditДокумент6 страницDebit & CreditSudhir Kumar YadavОценок пока нет

- International EntrepreneurshipДокумент4 страницыInternational EntrepreneurshipSudhir Kumar Yadav100% (1)

- Airtel (India) : Navigation SearchДокумент10 страницAirtel (India) : Navigation SearchSudhir Kumar YadavОценок пока нет

- Depreciation: Salient FeaturesДокумент12 страницDepreciation: Salient FeaturesSudhir Kumar YadavОценок пока нет

- Creative Problem SolvingДокумент26 страницCreative Problem SolvingSudhir Kumar Yadav50% (2)

- Business Presentations: Prepared By: Antra SinghДокумент14 страницBusiness Presentations: Prepared By: Antra SinghSudhir Kumar YadavОценок пока нет

- Women Entrepreneurs.Документ19 страницWomen Entrepreneurs.Sudhir Kumar Yadav100% (1)

- Innovation: The 4Ps' of InnovationДокумент9 страницInnovation: The 4Ps' of InnovationSudhir Kumar YadavОценок пока нет

- Managerial Communication Sr. Prof B D SinghДокумент48 страницManagerial Communication Sr. Prof B D SinghSudhir Kumar YadavОценок пока нет

- Presentation On SidosДокумент5 страницPresentation On SidosSudhir Kumar YadavОценок пока нет

- Aspm 1Документ37 страницAspm 1Sudhir Kumar YadavОценок пока нет

- Nabard Bank: National Bank For Agriculture and Rural DevelopementДокумент8 страницNabard Bank: National Bank For Agriculture and Rural DevelopementSudhir Kumar YadavОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- 24 - Costupdates - Very Important For May Final ExamsДокумент9 страниц24 - Costupdates - Very Important For May Final ExamsAnkur AgarwalОценок пока нет

- Customer Profitability Modeling at Aeroplan: Sylvain Tremblay, Aeroplan, Montréal, CanadaДокумент5 страницCustomer Profitability Modeling at Aeroplan: Sylvain Tremblay, Aeroplan, Montréal, CanadaNishant DuttaОценок пока нет

- Kotz, McDonough, Reich, Boyer Etc Estrutura Social de Acumulação, ConferênciaДокумент538 страницKotz, McDonough, Reich, Boyer Etc Estrutura Social de Acumulação, ConferênciaaflagsonОценок пока нет

- NUCOR Corporation CaseДокумент20 страницNUCOR Corporation Casekahlil gibran 17100% (1)

- Unit-12 Liquidity Vs ProfitabilityДокумент14 страницUnit-12 Liquidity Vs ProfitabilityKusum JaiswalОценок пока нет

- Customer Lifetime ValueДокумент16 страницCustomer Lifetime Valuearpit_9688Оценок пока нет

- Joint Venture 113: Solutions To Multiple ChoicesДокумент3 страницыJoint Venture 113: Solutions To Multiple ChoicesLaraОценок пока нет

- Weighted Scoring Model Kipling MethodДокумент7 страницWeighted Scoring Model Kipling MethodRabiatul AdawiyahОценок пока нет

- Oil PricingДокумент4 страницыOil PricingLola100% (1)

- Introduction To Managerial EconomicsДокумент7 страницIntroduction To Managerial EconomicsKran Lin100% (2)

- Course DocumentsДокумент257 страницCourse DocumentsGaurav Jain0% (1)

- 2 ACCT 2A&B P. OperationДокумент6 страниц2 ACCT 2A&B P. OperationBrian Christian VillaluzОценок пока нет

- TBДокумент31 страницаTBBenj LadesmaОценок пока нет

- Nesle BD - Term PaperДокумент17 страницNesle BD - Term PaperRakib HassanОценок пока нет

- Safi Airways In-Flight Magazine Issue 17th May-June 2013Документ88 страницSafi Airways In-Flight Magazine Issue 17th May-June 2013Said Zahid DanialОценок пока нет

- Ratio AnalysisДокумент69 страницRatio AnalysisAniqa AshrafОценок пока нет

- Ch01 SolutionsДокумент4 страницыCh01 SolutionshunkieОценок пока нет

- Business 2210 Case Analysis Report-FINALДокумент34 страницыBusiness 2210 Case Analysis Report-FINALtamim707100% (3)

- Incremental AnalysisДокумент18 страницIncremental AnalysisMonique CabreraОценок пока нет

- Alan Freeman - Value and The Foundation of Economic DynamicsДокумент20 страницAlan Freeman - Value and The Foundation of Economic DynamicsSebastián HernándezОценок пока нет

- Understanding Transactions in The Controlling ModuleДокумент31 страницаUnderstanding Transactions in The Controlling ModuleAbdelhamid HarakatОценок пока нет

- Final Project On Parag Dairy IndustryДокумент68 страницFinal Project On Parag Dairy IndustrySNEHAM29100% (2)

- Case Studies of Cost and Works AccountingДокумент17 страницCase Studies of Cost and Works AccountingShalini Srivastav50% (2)

- Financial Statements Are The End Products of Financial AcountingДокумент20 страницFinancial Statements Are The End Products of Financial AcountingAnkita Tolasaria100% (1)

- The Economic Impact of The British Greyhound Racing Industry 2014Документ32 страницыThe Economic Impact of The British Greyhound Racing Industry 2014artur_ganateОценок пока нет

- Nestle Annual ReportДокумент104 страницыNestle Annual ReportmohitagrahariОценок пока нет

- Where Is The Crisis Going?: Michel HussonДокумент18 страницWhere Is The Crisis Going?: Michel Hussonjajaja86868686Оценок пока нет

- Hassan Tariq Ghani Syed Saad Shah Syed Muhammad Hamza Syed Ather Waqar Syed Fayyaz Hasnain Case Presentation - Accounting For Decision MakingДокумент21 страницаHassan Tariq Ghani Syed Saad Shah Syed Muhammad Hamza Syed Ather Waqar Syed Fayyaz Hasnain Case Presentation - Accounting For Decision Makingchacha_420100% (2)

- Distinctions in Descriptive and Instrumental Stakeholder TheoryДокумент44 страницыDistinctions in Descriptive and Instrumental Stakeholder TheoryHimeОценок пока нет