Вам также может понравиться

- A Case Analysis of Farnsworth Furniture IndustriesДокумент20 страницA Case Analysis of Farnsworth Furniture IndustriesHimalaya Ban100% (1)

- Action Standard Manufacturing Company Report FinalДокумент16 страницAction Standard Manufacturing Company Report FinalNirab BhattaraiОценок пока нет

- Ethical Investment Process and OutcomesДокумент2 страницыEthical Investment Process and OutcomesGanesh ShresthaОценок пока нет

- Warner Body WorksДокумент35 страницWarner Body WorksPadam Shrestha50% (4)

- Ch-3: Intermediate Term Debt FinancingДокумент8 страницCh-3: Intermediate Term Debt Financingjack johnsonОценок пока нет

- Egret Printing and PublishingДокумент61 страницаEgret Printing and Publishingsank47_31497034450% (2)

- Warner Body WorksДокумент32 страницыWarner Body WorksPadam Shrestha100% (2)

- The Impact of Corporate Governance On The Profitability of Nepalese EnterpriseДокумент10 страницThe Impact of Corporate Governance On The Profitability of Nepalese EnterpriseAyush Nepal100% (1)

- Group 4 Mba Finance 21st Batch Report On Envrongard CorporationДокумент53 страницыGroup 4 Mba Finance 21st Batch Report On Envrongard CorporationS TMОценок пока нет

- Silver River Manufacturing Company (SRM)Документ45 страницSilver River Manufacturing Company (SRM)Siddhartha Chhetri100% (2)

- Case Study On Biotech Services Inc.: MBA-Finance Third TrimesterДокумент19 страницCase Study On Biotech Services Inc.: MBA-Finance Third TrimesteranjanaОценок пока нет

- Environgard CorporationДокумент4 страницыEnvirongard CorporationRina Nanu33% (3)

- Environgard Corp CaseДокумент45 страницEnvirongard Corp Casejack johnson100% (1)

- Capital StructureДокумент4 страницыCapital StructureNaveen GurnaniОценок пока нет

- Organizational Structure of Nepal Investment Bank LimitedДокумент1 страницаOrganizational Structure of Nepal Investment Bank LimitedRupak Raj Rimal67% (3)

- Hudson CaseДокумент8 страницHudson CaseSrikar ReddyОценок пока нет

- IAPM Selected NumericalsДокумент18 страницIAPM Selected NumericalsPareen DesaiОценок пока нет

- SMJC 3123 Project Finance QuestionsДокумент2 страницыSMJC 3123 Project Finance QuestionsJuandeLaОценок пока нет

- Environgrad Corporation: Evaluating Three Financing AlternativesДокумент25 страницEnvirongrad Corporation: Evaluating Three Financing AlternativesAbhi Krishna ShresthaОценок пока нет

- Nepal Clearing HouseДокумент17 страницNepal Clearing HouseDiwas MandalОценок пока нет

- Determination of Forward and Futures Prices: Practice QuestionsДокумент3 страницыDetermination of Forward and Futures Prices: Practice Questionshoai_hm2357Оценок пока нет

- Relevant PopulationДокумент3 страницыRelevant PopulationMarsya Chikita LestariОценок пока нет

- Silver River Manufacturing Company Case StudyДокумент46 страницSilver River Manufacturing Company Case StudyPankaj Kunwar100% (3)

- Financial Econometrics-Mba 451F Cia - 1 Building Research ProposalДокумент4 страницыFinancial Econometrics-Mba 451F Cia - 1 Building Research ProposalPratik ChourasiaОценок пока нет

- CF Final (1) On PTR Restaurant Mini CaseДокумент23 страницыCF Final (1) On PTR Restaurant Mini Caseshiv029Оценок пока нет

- Case Study - Nilgai Foods: Positioning Packaged Coconut Water in India (Cocofly)Документ6 страницCase Study - Nilgai Foods: Positioning Packaged Coconut Water in India (Cocofly)prathmesh kulkarniОценок пока нет

- MBA Financial Management Assignment SolutionsДокумент24 страницыMBA Financial Management Assignment SolutionsRohan AhujaОценок пока нет

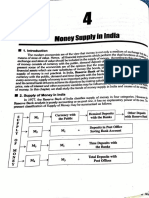

- Money Supply in India 1Документ9 страницMoney Supply in India 1Chaitanya ChoudharyОценок пока нет

- ADL 01 Assignment AДокумент5 страницADL 01 Assignment Aversha2950% (2)

- Yankee Fork and Hoe Company1Документ18 страницYankee Fork and Hoe Company1Pallav KumarОценок пока нет

- Mercier Corporation stock valuation analysisДокумент3 страницыMercier Corporation stock valuation analysisTien Dao0% (1)

- QP March2012 p1Документ20 страницQP March2012 p1Dhanushka Rajapaksha100% (1)

- Solutions To Problems: Smart/Gitman/Joehnk, Fundamentals of Investing, 12/e Chapter 8Документ4 страницыSolutions To Problems: Smart/Gitman/Joehnk, Fundamentals of Investing, 12/e Chapter 8Ahmed El KhateebОценок пока нет

- Ch01 Solutions Manual An Overview of FM and The Financial Management and The FinancialДокумент4 страницыCh01 Solutions Manual An Overview of FM and The Financial Management and The FinancialAM FMОценок пока нет

- Chapter 05 - (The Accounting Cycle. Reporting Financial Results)Документ22 страницыChapter 05 - (The Accounting Cycle. Reporting Financial Results)Hafiz SherazОценок пока нет

- Case PPA (SMART) - QuestionДокумент9 страницCase PPA (SMART) - QuestionSekar WiridianaОценок пока нет

- HRM Practices in Nepalese Commercial BanksДокумент13 страницHRM Practices in Nepalese Commercial BanksSomesh Ashim JoshiОценок пока нет

- History and Features of Nepal's Consumer Protection MovementДокумент12 страницHistory and Features of Nepal's Consumer Protection MovementBijayОценок пока нет

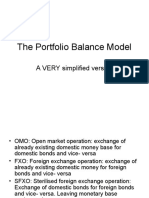

- 9.the Portfolio Balance ModelДокумент40 страниц9.the Portfolio Balance ModelVelichka DimitrovaОценок пока нет

- Liquidity Preference As Behavior Towards Risk Review of Economic StudiesДокумент23 страницыLiquidity Preference As Behavior Towards Risk Review of Economic StudiesCuenta EliminadaОценок пока нет

- P2 November 2014 Question Paper PDFДокумент20 страницP2 November 2014 Question Paper PDFAnu MauryaОценок пока нет

- FM11 CH 12 Mini CaseДокумент14 страницFM11 CH 12 Mini CaseRahul Rathi100% (1)

- Aggregate Planning Strategies for Supply Chain OptimizationДокумент9 страницAggregate Planning Strategies for Supply Chain OptimizationThiru VenkatОценок пока нет

- Mergers, Acquisitions & Strategic AlliancesДокумент17 страницMergers, Acquisitions & Strategic AlliancesTahseenKhanОценок пока нет

- Practice Questions MGT 632: Business Research Methods/ MGB 114: Research MethodsДокумент9 страницPractice Questions MGT 632: Business Research Methods/ MGB 114: Research MethodsVishal SharmaОценок пока нет

- Black Scholes Model ReportДокумент6 страницBlack Scholes Model ReportminhalОценок пока нет

- Bond ImmunisationДокумент29 страницBond ImmunisationVaidyanathan RavichandranОценок пока нет

- Yankee Fork and HoeДокумент4 страницыYankee Fork and HoeRhiki CourdhovaОценок пока нет

- BF2207 Exercise 6 - Dorchester LimitedДокумент2 страницыBF2207 Exercise 6 - Dorchester LimitedEvelyn TeoОценок пока нет

- Portfolio ManagementДокумент40 страницPortfolio ManagementSayaliRewaleОценок пока нет

- Security Market Indicator Series - STДокумент36 страницSecurity Market Indicator Series - STEng Hams100% (1)

- Buyback and Delisting of SharesДокумент42 страницыBuyback and Delisting of SharesSahil SinglaОценок пока нет

- Case Study Solution ResultsДокумент1 страницаCase Study Solution ResultsOscar VillarrealОценок пока нет

- Case QuestionsДокумент6 страницCase QuestionsRia MehtaОценок пока нет

- Appendix B Solutions To Concept ChecksДокумент31 страницаAppendix B Solutions To Concept Checkshellochinp100% (1)

- Background - Venture Capital and Stages of Financing (Ross - 7th Edition) Venture CapitalДокумент8 страницBackground - Venture Capital and Stages of Financing (Ross - 7th Edition) Venture CapitalDaniel GaoОценок пока нет

- Revision Pack 4 May 2011Документ27 страницRevision Pack 4 May 2011Lim Hui SinОценок пока нет

- Compre BAV Sol 2019-20 1Документ9 страницCompre BAV Sol 2019-20 1f20211062Оценок пока нет

- Solutions Lam PhamДокумент20 страницSolutions Lam PhamHuong Thien Hoang0% (1)

- Essential Business School Case Studies - Business InsiderДокумент8 страницEssential Business School Case Studies - Business InsiderHimalaya BanОценок пока нет

- Role of Remittance in Economic Development of NepalДокумент1 страницаRole of Remittance in Economic Development of NepalHimalaya BanОценок пока нет

- ALM AssignmentДокумент2 страницыALM AssignmentHimalaya BanОценок пока нет

- Selection Tests in Human Resource ManagementДокумент11 страницSelection Tests in Human Resource ManagementHimalaya BanОценок пока нет

- The Impact of Board Composition On Corporate Firm Perfomance Evidence From Listed Commercial Banks in NepalДокумент26 страницThe Impact of Board Composition On Corporate Firm Perfomance Evidence From Listed Commercial Banks in NepalHimalaya BanОценок пока нет

- Egret Case StudyДокумент35 страницEgret Case StudyHimalaya BanОценок пока нет

- Egret Printing and Publishing CompanyДокумент35 страницEgret Printing and Publishing CompanyHimalaya BanОценок пока нет

- Business Plan of OrthodoxДокумент54 страницыBusiness Plan of OrthodoxHimalaya BanОценок пока нет

- Presenting Data in Tables and ChartsДокумент35 страницPresenting Data in Tables and ChartsHimalaya BanОценок пока нет

- Uniglobe College: Lesson Plan: Business StatisticsДокумент6 страницUniglobe College: Lesson Plan: Business StatisticsHimalaya BanОценок пока нет

- Introduction and Data CollectionДокумент27 страницIntroduction and Data CollectionHimalaya Ban100% (1)

- Introduction StatisticsДокумент23 страницыIntroduction StatisticsHimalaya Ban100% (1)

- SPDR Barclays Capital Intermediate Term Corporate Bond ETF 1-10YДокумент2 страницыSPDR Barclays Capital Intermediate Term Corporate Bond ETF 1-10YRoberto PerezОценок пока нет

- CIMB Loan ApplicationДокумент10 страницCIMB Loan ApplicationSyamz AzrinОценок пока нет

- Financial Inclusion in India - A Review of InitiatДокумент11 страницFinancial Inclusion in India - A Review of InitiatEshan BedagkarОценок пока нет

- Black BookДокумент21 страницаBlack BookShaikh Muskaan100% (2)

- For Revision of Income TaxДокумент5 страницFor Revision of Income TaxMA AttariОценок пока нет

- Four Steps First FX Trade CAДокумент7 страницFour Steps First FX Trade CAKevin MonksОценок пока нет

- Time Value of MoneyДокумент20 страницTime Value of Moneymdsabbir100% (1)

- Indian Rupee: People Also AskДокумент1 страницаIndian Rupee: People Also AskAadish ChopraОценок пока нет

- Farm Animal Payment Plan AgreementДокумент3 страницыFarm Animal Payment Plan AgreementRia KudoОценок пока нет

- RPT Math DLP Year 2 2022-2023 by Rozayus AcademyДокумент16 страницRPT Math DLP Year 2 2022-2023 by Rozayus AcademyrphsekolahrendahОценок пока нет

- Audit of Cash and Cash EquivalentsДокумент10 страницAudit of Cash and Cash EquivalentsDebs FanogaОценок пока нет

- Key Smart Checking: Account SummaryДокумент4 страницыKey Smart Checking: Account SummaryDemetrius Diamond IIОценок пока нет

- Ibo-6 Unit-1 International Monetary Systems and InstitutionsДокумент7 страницIbo-6 Unit-1 International Monetary Systems and InstitutionsGaytri KochharОценок пока нет

- ACCT 3331 Exam 2 Review Chapter 18 - Revenue RecognitionДокумент14 страницACCT 3331 Exam 2 Review Chapter 18 - Revenue RecognitionXiaoying XuОценок пока нет

- Hotel Real Estate Investments & Asset Management CertificateДокумент2 страницыHotel Real Estate Investments & Asset Management CertificateAsrarОценок пока нет

- CBN Rule Book Volume 3Документ1 243 страницыCBN Rule Book Volume 3Justus OhakanuОценок пока нет

- Understanding Cheques and Bank StatementsДокумент2 страницыUnderstanding Cheques and Bank StatementsAaliyah BayleyОценок пока нет

- Lakshadweep Island-Tour Packages - APAДокумент2 страницыLakshadweep Island-Tour Packages - APAmanishk21Оценок пока нет

- Government Grants AccountingДокумент2 страницыGovernment Grants AccountingCaseylyn RonquilloОценок пока нет

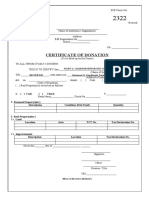

- BIR Form 2322 Cert of Don - FG Calderon High SchoolДокумент3 страницыBIR Form 2322 Cert of Don - FG Calderon High SchoolEdmund G. VillarealОценок пока нет

- Annuities Problems Worksheet with Formulas and SolutionsДокумент8 страницAnnuities Problems Worksheet with Formulas and SolutionsSiddharth DahiyaОценок пока нет

- Skandia Mining Company Financial Statements Income Statement Balance Sheet Assets Liabilities and Owner'S EquityДокумент2 страницыSkandia Mining Company Financial Statements Income Statement Balance Sheet Assets Liabilities and Owner'S EquityIzzahIkramIllahiОценок пока нет

- Principles of Accoutning Edb 100 NotesДокумент67 страницPrinciples of Accoutning Edb 100 NotesFidel Flavin100% (3)

- Jas PDFДокумент21 страницаJas PDFJaspreet singh LICОценок пока нет

- Money Market PresentationДокумент18 страницMoney Market PresentationAvni Sharma100% (1)

- Conventional Subrogation Requires ConsentДокумент2 страницыConventional Subrogation Requires ConsentLiaa Aquino100% (3)

- Nestle PakistanДокумент9 страницNestle PakistanRabia Mahmood ChaudhryОценок пока нет

- Case Study - Financial Statement AnaysisДокумент8 страницCase Study - Financial Statement Anaysisssimi137Оценок пока нет

- Practice Problems Ch12Документ57 страницPractice Problems Ch12Kevin Baconga100% (2)

- Chapter 15Документ10 страницChapter 15Julia Angelica WijayaОценок пока нет