Вам также может понравиться

- Special Power of Attorney SPA - To Buy PurchaseДокумент2 страницыSpecial Power of Attorney SPA - To Buy PurchaseAlberto Pamintuan III79% (19)

- YBM GST Invoice FormatДокумент4 страницыYBM GST Invoice FormatMl AgarwalОценок пока нет

- Jakarta Investment ProjectДокумент63 страницыJakarta Investment ProjectLuqmanSudradjatОценок пока нет

- 14 Class Action Suit Filed in New York AgainstДокумент1 страница14 Class Action Suit Filed in New York AgainstAnonymous EKGJIpGwPjОценок пока нет

- EXIM Financing and Documentationt200813Документ340 страницEXIM Financing and Documentationt200813Ramalingam Chandrasekharan0% (1)

- Facilities Provided by The Bank To Importer & ExporterДокумент65 страницFacilities Provided by The Bank To Importer & Exportershahin14367% (9)

- FinanceДокумент3 страницыFinanceyogi9009Оценок пока нет

- CocДокумент47 страницCocUmesh ChandraОценок пока нет

- Final Project EXIM FINANCEДокумент78 страницFinal Project EXIM FINANCErohit utekar100% (1)

- Balance of PaymentДокумент38 страницBalance of PaymentAyush SinghОценок пока нет

- Capital BudgetingДокумент30 страницCapital BudgetingUmesh ChandraОценок пока нет

- What Is A "Derivative" ?Документ4 страницыWhat Is A "Derivative" ?RAHULОценок пока нет

- Terms of PaymentДокумент20 страницTerms of PaymentNiladri Sekhar JyotiОценок пока нет

- Financing International TradeДокумент19 страницFinancing International TradeUmesh ChandraОценок пока нет

- Financing International TradeДокумент19 страницFinancing International TradeUmesh ChandraОценок пока нет

- Financing International TradeДокумент19 страницFinancing International TradeUmesh ChandraОценок пока нет

- Quiz One 9-12 BatchДокумент5 страницQuiz One 9-12 BatchAtish MukherjeeОценок пока нет

- International Business StrategyДокумент7 страницInternational Business StrategyKRITI SETH MBA IB 2018-20 (DEL)Оценок пока нет

- Sources of International FinancingДокумент6 страницSources of International FinancingSabha Pathy100% (2)

- 453a Exim FinanceДокумент19 страниц453a Exim FinanceZain MaggssiОценок пока нет

- Import FinanceДокумент6 страницImport FinanceSammir Malhotra0% (1)

- SCM - 2 UnitДокумент91 страницаSCM - 2 UnitNeelam Yadav50% (2)

- Term Paper - Evolution of Derivatives in IndiaДокумент20 страницTerm Paper - Evolution of Derivatives in IndiachiragIRMAОценок пока нет

- Money MarketДокумент20 страницMoney Marketmanisha guptaОценок пока нет

- Indian Financial SystemДокумент163 страницыIndian Financial SystemrohitravaliyaОценок пока нет

- IE GA Notes - 1 PDFДокумент113 страницIE GA Notes - 1 PDFsurajdhunnaОценок пока нет

- STP Competitive AdvantageДокумент58 страницSTP Competitive Advantageamatulmateennoor100% (1)

- International Production: A Decade of Transformation AheadДокумент60 страницInternational Production: A Decade of Transformation AheadSunil ChoudhuryОценок пока нет

- IBFE Note 1Документ9 страницIBFE Note 1Dinesh SinghОценок пока нет

- RBI Intervention in Foreign Exchange MarketДокумент26 страницRBI Intervention in Foreign Exchange Marketshamchandak03100% (1)

- Epgdib 2014-15 P&GДокумент16 страницEpgdib 2014-15 P&Ggrover_kОценок пока нет

- CyWorld Group 11Документ11 страницCyWorld Group 11Shweta Srivastava100% (1)

- Tips On Project FinancingДокумент3 страницыTips On Project FinancingRattinakumar SivaradjouОценок пока нет

- OTCEIДокумент11 страницOTCEIvisa_kpОценок пока нет

- Cox Communications XLS372 XLS ENGДокумент13 страницCox Communications XLS372 XLS ENGPriyank BoobОценок пока нет

- Financing of Foreign TradeДокумент18 страницFinancing of Foreign Tradepriya nОценок пока нет

- Pre-Shipment and Post-Shipment Finance: Dr. A.K. Sengupta Former Dean, Indian Institute of Foreign TradeДокумент7 страницPre-Shipment and Post-Shipment Finance: Dr. A.K. Sengupta Former Dean, Indian Institute of Foreign TradeimadОценок пока нет

- Security Analysis and Portfolio ManagementДокумент20 страницSecurity Analysis and Portfolio ManagementReetika JainОценок пока нет

- Bond ValuationДокумент3 страницыBond ValuationNoman Khosa100% (1)

- What Is An International Bank?: AnswerДокумент22 страницыWhat Is An International Bank?: AnswerSonetAsrafulОценок пока нет

- Export Finance-Countertrade and ForfaitingДокумент26 страницExport Finance-Countertrade and ForfaitingRajat LoyaОценок пока нет

- Environmental Analysis: Process of Examining The Organization's Environment To DetermineДокумент9 страницEnvironmental Analysis: Process of Examining The Organization's Environment To DetermineTirthankar DattaОценок пока нет

- Lasserre Globalisation IndicesДокумент10 страницLasserre Globalisation IndicesNavneet KumarОценок пока нет

- Concep To Export PromotionДокумент30 страницConcep To Export PromotionshailendraОценок пока нет

- Euro BondsДокумент21 страницаEuro BondsKhan ZiaОценок пока нет

- Term Paper On: "Money Market Contribution in A Developing Economy Like Bangladesh"Документ30 страницTerm Paper On: "Money Market Contribution in A Developing Economy Like Bangladesh"Fahim MalikОценок пока нет

- CH 1 - Scope of International FinanceДокумент7 страницCH 1 - Scope of International Financepritesh_baidya269100% (3)

- Quiz 2Документ3 страницыQuiz 2rajthakre81Оценок пока нет

- Introduction To Project FinanceДокумент38 страницIntroduction To Project FinanceMuhammad Waheed SattiОценок пока нет

- Pre Shipment FinanceДокумент21 страницаPre Shipment FinanceSandip ShawОценок пока нет

- International Business Strategy 1Документ7 страницInternational Business Strategy 1rajthakre81Оценок пока нет

- Global Strategy-Lesserie PhilippeДокумент10 страницGlobal Strategy-Lesserie PhilippePrashant BedwalОценок пока нет

- Strategic AlliancesДокумент7 страницStrategic AlliancesNahian Rahman RochiОценок пока нет

- International Trade TheoriesДокумент41 страницаInternational Trade TheoriesShruti VadherОценок пока нет

- Financing Ofproject Appraisal ProjectДокумент52 страницыFinancing Ofproject Appraisal Projectdeeparaghu6100% (2)

- AssignmentДокумент5 страницAssignmentASHHAR AZIZОценок пока нет

- Wto PPT 121124195716 Phpapp02Документ10 страницWto PPT 121124195716 Phpapp02Raaj KumarОценок пока нет

- Factoring Project ReportДокумент15 страницFactoring Project ReportSiddharth Desai100% (3)

- WalmartДокумент36 страницWalmartMohan Lal AroraОценок пока нет

- Composition and Direction of Trade and Foreign Trade PolicyДокумент34 страницыComposition and Direction of Trade and Foreign Trade PolicySnehithОценок пока нет

- Strategic Market Segmentation: Prepared By: Ma. Anna Corina G. Kagaoan Instructor College of Business and AccountancyДокумент33 страницыStrategic Market Segmentation: Prepared By: Ma. Anna Corina G. Kagaoan Instructor College of Business and AccountancyAhsan ShahidОценок пока нет

- Basel I II and IIIДокумент52 страницыBasel I II and IIIAPPIAH DENNIS OFORIОценок пока нет

- Some Examples of Strategic AlliancesДокумент1 страницаSome Examples of Strategic AlliancesShelly AgarwalОценок пока нет

- Forward Rate AgreementsДокумент6 страницForward Rate AgreementsAmul ShresthaОценок пока нет

- Regional Integrations IBMДокумент64 страницыRegional Integrations IBMdileepsuОценок пока нет

- FDRM AssignmentДокумент3 страницыFDRM AssignmentAmit K SharmaОценок пока нет

- Gamification in Consumer Research A Clear and Concise ReferenceОт EverandGamification in Consumer Research A Clear and Concise ReferenceОценок пока нет

- Methods of Payment in International TradeДокумент43 страницыMethods of Payment in International TradeSantosh SharmaОценок пока нет

- Presented By: Altamash Ahmad: PGDM 2014-2016Документ14 страницPresented By: Altamash Ahmad: PGDM 2014-2016lifeis1enjoyОценок пока нет

- International MarketingДокумент2 страницыInternational MarketingSwetha RameshОценок пока нет

- Research Methodology PH.D EntranceДокумент2 страницыResearch Methodology PH.D EntranceUmesh ChandraОценок пока нет

- Annual Report 2017-18Документ116 страницAnnual Report 2017-18Umesh ChandraОценок пока нет

- JAIIB Banker Customer Relation - J N NayakДокумент14 страницJAIIB Banker Customer Relation - J N NayakUmesh ChandraОценок пока нет

- Sunil Kumar Bansal: Encl.: As AboveДокумент3 страницыSunil Kumar Bansal: Encl.: As AboveUmesh ChandraОценок пока нет

- Lecture 18Документ10 страницLecture 18Umesh ChandraОценок пока нет

- Lecture 16: Friedman's Challenge To Keynes Money Demand and Labour Supply CurveДокумент7 страницLecture 16: Friedman's Challenge To Keynes Money Demand and Labour Supply CurveUmesh ChandraОценок пока нет

- Modelling Stress Scenarios: Sanjay Basu, NIBM, November 2012Документ10 страницModelling Stress Scenarios: Sanjay Basu, NIBM, November 2012Umesh ChandraОценок пока нет

- Overview On Risk in Int BsnsДокумент34 страницыOverview On Risk in Int BsnsUmesh ChandraОценок пока нет

- Currency ExposureДокумент39 страницCurrency ExposureUmesh ChandraОценок пока нет

- Global Liquidity and Financial ContagionДокумент10 страницGlobal Liquidity and Financial ContagionUmesh ChandraОценок пока нет

- Basic Aspects of Superconductivity: By-Poonam Kumari Guide: Prof. S. Ramakrishnan TIFR, MumbaiДокумент24 страницыBasic Aspects of Superconductivity: By-Poonam Kumari Guide: Prof. S. Ramakrishnan TIFR, MumbaiUmesh ChandraОценок пока нет

- Stress Testing Market RiskДокумент18 страницStress Testing Market RiskUmesh ChandraОценок пока нет

- By Sudarshana Bhat Asst General Manager Corporation Bank: Exchange Rate MechanismДокумент42 страницыBy Sudarshana Bhat Asst General Manager Corporation Bank: Exchange Rate MechanismUmesh ChandraОценок пока нет

- Finance 2Документ98 страницFinance 2kjpatelОценок пока нет

- JAIIB N I Act 1881Документ42 страницыJAIIB N I Act 1881Umesh ChandraОценок пока нет

- Lecture 19Документ12 страницLecture 19Umesh ChandraОценок пока нет

- Finance 2Документ98 страницFinance 2kjpatelОценок пока нет

- Economy I EngДокумент40 страницEconomy I EngNitinSharmaОценок пока нет

- Financial Inclusion PNBДокумент25 страницFinancial Inclusion PNBUmesh ChandraОценок пока нет

- A Project Study Report On: Training Undertaken atДокумент59 страницA Project Study Report On: Training Undertaken atAmit GuptaОценок пока нет

- CMC Vellore AppointmentДокумент1 страницаCMC Vellore AppointmentVarun reddy JavvajiОценок пока нет

- 2013 Economy PrelimsДокумент135 страниц2013 Economy PrelimsNancy DebbarmaОценок пока нет

- 3 Cash - Lecture Notes PDFДокумент11 страниц3 Cash - Lecture Notes PDFJohn Paul EslerОценок пока нет

- Corporate PPT - Nucleus SoftwareДокумент13 страницCorporate PPT - Nucleus SoftwarePriyanshu AggarwalОценок пока нет

- FI - Summer 2022 - PPT Slides - Banking RatiosДокумент34 страницыFI - Summer 2022 - PPT Slides - Banking RatiosMavara SiddiquiОценок пока нет

- Chapter 4 TVM EditedДокумент24 страницыChapter 4 TVM EditedWonde BiruОценок пока нет

- Mission and Vision StatementsДокумент4 страницыMission and Vision Statementsabass amaduОценок пока нет

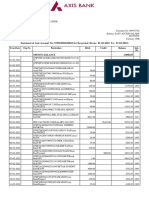

- Statement of Axis Account No:919010020630823 For The Period (From: 01-02-2022 To: 27-02-2022)Документ3 страницыStatement of Axis Account No:919010020630823 For The Period (From: 01-02-2022 To: 27-02-2022)Laxman GandiОценок пока нет

- All Entrance Exam Papers - Abhyudaya Cooperative Bank General Awareness PaperДокумент9 страницAll Entrance Exam Papers - Abhyudaya Cooperative Bank General Awareness PaperPrasunMajumderОценок пока нет

- Project Report " ": Cashless Payment A Convenient Mode of PaymentДокумент33 страницыProject Report " ": Cashless Payment A Convenient Mode of PaymentDhaval MistryОценок пока нет

- Michael C. Robinson QualificationsДокумент3 страницыMichael C. Robinson QualificationsIsland Packet and Beaufort GazetteОценок пока нет

- Jyothy Laboratories LTDДокумент5 страницJyothy Laboratories LTDViju K GОценок пока нет

- Final Black Book CONSUMER FINANCE FOR MOINДокумент78 страницFinal Black Book CONSUMER FINANCE FOR MOINirfan khanОценок пока нет

- Recharge Amount: Original Copy For Recipient - Tax InvoiceДокумент1 страницаRecharge Amount: Original Copy For Recipient - Tax InvoiceRoshan MahtoОценок пока нет

- 18BNU5196Документ3 страницы18BNU5196jayanthanОценок пока нет

- Shopno Jatra Proposal LetterДокумент3 страницыShopno Jatra Proposal LetterNazrul IslamОценок пока нет

- Galanesia Invoice For Transaction 5495Документ2 страницыGalanesia Invoice For Transaction 5495Agus SuОценок пока нет

- Partner of Our N.C.V.T / Approved Co Partner of Our N.C.V.T / M.HRD Approved Courses M.HRDДокумент6 страницPartner of Our N.C.V.T / Approved Co Partner of Our N.C.V.T / M.HRD Approved Courses M.HRDQhsef Karmaveer Jyoteendra VaishnavОценок пока нет

- INVOICE GambiaДокумент2 страницыINVOICE GambiaPhilippe AKUE-ABOSSEОценок пока нет

- 601imguf CarryOverExaminationSchedule (B.Tech.,BCA)Документ2 страницы601imguf CarryOverExaminationSchedule (B.Tech.,BCA)Utkarsha SinghОценок пока нет

- Industrial Sickness-Causes & RemediesДокумент3 страницыIndustrial Sickness-Causes & RemediesdeepshrmОценок пока нет

- CV TN 09012016Документ2 страницыCV TN 09012016Parag ShettyОценок пока нет

- PROPOSALДокумент24 страницыPROPOSALNesru SirajОценок пока нет