Вам также может понравиться

- Corporate Finance Formulas: A Simple IntroductionОт EverandCorporate Finance Formulas: A Simple IntroductionРейтинг: 4 из 5 звезд4/5 (8)

- NYSF Leveraged Buyout Model Solution Part TwoДокумент20 страницNYSF Leveraged Buyout Model Solution Part TwoBenОценок пока нет

- Risk and Retrun TheoryДокумент40 страницRisk and Retrun TheorySonakshi TayalОценок пока нет

- Unit-3, The Risk and Return-The Basics, 2015Документ66 страницUnit-3, The Risk and Return-The Basics, 2015Momenul Islam Mridha MuradОценок пока нет

- Strategy FormulationДокумент12 страницStrategy FormulationChinmay ShirsatОценок пока нет

- Portfolio Performance EvaluationДокумент20 страницPortfolio Performance Evaluationrajin_rammsteinОценок пока нет

- Origin of All Derivatives: Risk Is The Only Constant, Uncertainty Is The Only CertaintyДокумент36 страницOrigin of All Derivatives: Risk Is The Only Constant, Uncertainty Is The Only CertaintyChinmay ShirsatОценок пока нет

- Presentation 04 - Risk and Return 2012.11.15Документ54 страницыPresentation 04 - Risk and Return 2012.11.15SantaAgataОценок пока нет

- Sortino - A "Sharper" Ratio! - Red Rock CapitalДокумент6 страницSortino - A "Sharper" Ratio! - Red Rock CapitalInterconti Ltd.Оценок пока нет

- Var, CaR, CAR, Basel 1 and 2Документ7 страницVar, CaR, CAR, Basel 1 and 2ChartSniperОценок пока нет

- Risk N Return BasicsДокумент47 страницRisk N Return BasicsRosli OthmanОценок пока нет

- 2.3 - Average Directional Movement Index Rating (ADXR) - Forex Indicators GuideДокумент2 страницы2.3 - Average Directional Movement Index Rating (ADXR) - Forex Indicators Guideenghoss77Оценок пока нет

- Session 18 & 19: Instructor: Nivedita Sinha Email: Nivedita - Sinha@nmims - EduДокумент23 страницыSession 18 & 19: Instructor: Nivedita Sinha Email: Nivedita - Sinha@nmims - EduHitesh JainОценок пока нет

- Chapter 25 - Evaluation of Portfolio PerformanceДокумент32 страницыChapter 25 - Evaluation of Portfolio PerformanceMukesh Karunakaran100% (1)

- Sortino - A Better Measure of Risk? ROLLINGER Feb 2013Документ3 страницыSortino - A Better Measure of Risk? ROLLINGER Feb 2013Interconti Ltd.Оценок пока нет

- Portfolio Performance Measures Course Code: DFI 354 Submitted To: Dr. Winnie Nyamute Presented byДокумент12 страницPortfolio Performance Measures Course Code: DFI 354 Submitted To: Dr. Winnie Nyamute Presented byChristopher KipsangОценок пока нет

- How Sharp Is The Shape-Ratio? - Risk-Adjusted Performance MeasuresДокумент13 страницHow Sharp Is The Shape-Ratio? - Risk-Adjusted Performance MeasuresMaggie HartonoОценок пока нет

- Treynor Performance MeasureДокумент8 страницTreynor Performance MeasureAshadur Rahman JahedОценок пока нет

- Risk and Return S1 2018Документ9 страницRisk and Return S1 2018Quentin SchwartzОценок пока нет

- Sharpe Ratio: R R E (R RДокумент17 страницSharpe Ratio: R R E (R Rvipin gargОценок пока нет

- Treynor RatioДокумент1 страницаTreynor Ratiosana_sr_96Оценок пока нет

- Investment Management Evaluation of Portfolio PerformanceДокумент28 страницInvestment Management Evaluation of Portfolio PerformanceJohnfree VallinasОценок пока нет

- Foundations of Risk Management: FRM Part 1Документ19 страницFoundations of Risk Management: FRM Part 1Javneet KaurОценок пока нет

- CAPM2Документ31 страницаCAPM2ELISHA OCAMPOОценок пока нет

- Chap 10 Portfolio Performance RevДокумент35 страницChap 10 Portfolio Performance RevYibeltal AssefaОценок пока нет

- Investment Management: Chapter 5 - Performance EvaluationДокумент25 страницInvestment Management: Chapter 5 - Performance EvaluationyebegashetОценок пока нет

- CH 7 Portfolio RiskДокумент5 страницCH 7 Portfolio RiskPravin MandoraОценок пока нет

- Mutual Fund Evaluation/Model: Ranpreet KaurДокумент14 страницMutual Fund Evaluation/Model: Ranpreet KaurmuntaquirОценок пока нет

- CHAPTER 4 Risk and Return The BasicsДокумент48 страницCHAPTER 4 Risk and Return The BasicsBerto UsmanОценок пока нет

- Chapter 11 NISMДокумент12 страницChapter 11 NISMKiran VidhaniОценок пока нет

- Chapter 11 20212 Portfolio Performance EditedДокумент28 страницChapter 11 20212 Portfolio Performance Editedsyed hakeemОценок пока нет

- Risk Adjusted PerformanceДокумент23 страницыRisk Adjusted PerformanceIrfan U ShahОценок пока нет

- Investment Decision and Portfolio Management (ACFN 524: Chapter 5 - Performance EvaluationДокумент25 страницInvestment Decision and Portfolio Management (ACFN 524: Chapter 5 - Performance EvaluationSnn News TubeОценок пока нет

- Investment Theory #16 - Performance Appraisal - Wiser DailyДокумент4 страницыInvestment Theory #16 - Performance Appraisal - Wiser DailyVovan VovanОценок пока нет

- Financial Ratios CFP On ExcelДокумент20 страницFinancial Ratios CFP On ExcelAkash JadhavОценок пока нет

- Investment Management: Risk & Performance MeasurementДокумент18 страницInvestment Management: Risk & Performance MeasurementPaul WangОценок пока нет

- Ex Ante Beta MeasurementДокумент24 страницыEx Ante Beta MeasurementAnonymous MUA3E8tQОценок пока нет

- Sapm M6Документ6 страницSapm M6Aarushi GuptaОценок пока нет

- FIN 435 Exam 3 SlidesДокумент85 страницFIN 435 Exam 3 SlidesMd. Mehedi HasanОценок пока нет

- FIN 435 SlidesДокумент61 страницаFIN 435 SlidesMd. Mehedi HasanОценок пока нет

- Risk Adjusted Return RatiosДокумент15 страницRisk Adjusted Return RatiosvenugopalОценок пока нет

- Evaluation of StockДокумент48 страницEvaluation of StockMd Zainuddin IbrahimОценок пока нет

- BCH 503 SM05Документ14 страницBCH 503 SM05sugandh bajajОценок пока нет

- RMG (Jorge) RiskAttributionForAssetManagerДокумент31 страницаRMG (Jorge) RiskAttributionForAssetManagerShekharmehta77Оценок пока нет

- Portfolio Performance Evaluation (1285)Документ6 страницPortfolio Performance Evaluation (1285)Nahid AhmedОценок пока нет

- Task 15 The Art of Listening: Prepared by Akshaya Venugopal Junior Research AnalystДокумент4 страницыTask 15 The Art of Listening: Prepared by Akshaya Venugopal Junior Research AnalystAkshaya VenugopalОценок пока нет

- Module #04 - Risk and Rates ReturnДокумент13 страницModule #04 - Risk and Rates ReturnRhesus UrbanoОценок пока нет

- 10 Risk and Return - Student VersionДокумент59 страниц10 Risk and Return - Student VersionKalyani GogoiОценок пока нет

- Investment Analysis and Portfolio Management (ACFN 632) : Chapter 5 - Performance EvaluationДокумент25 страницInvestment Analysis and Portfolio Management (ACFN 632) : Chapter 5 - Performance EvaluationhabtamuОценок пока нет

- Chapter 5.pptx Risk and ReturnДокумент25 страницChapter 5.pptx Risk and ReturnKevin Kivanc IlgarОценок пока нет

- D - Tutorial 3 (Solutions)Документ8 страницD - Tutorial 3 (Solutions)AlfieОценок пока нет

- Fin 435Документ73 страницыFin 435rimujaved11Оценок пока нет

- Investemnts Answers To Problem Set 6Документ6 страницInvestemnts Answers To Problem Set 6chu chenОценок пока нет

- Unit5 SapmДокумент4 страницыUnit5 SapmBhaskaran BalamuraliОценок пока нет

- Discount Rate or Hurdle Rate Module 7 (Class 24)Документ18 страницDiscount Rate or Hurdle Rate Module 7 (Class 24)Vineet Agarwal100% (1)

- EMBA Chapter5Документ38 страницEMBA Chapter5Mehrab RehmanОценок пока нет

- Session 4 Portfolio Performance EvaluationДокумент55 страницSession 4 Portfolio Performance Evaluationrobin robinОценок пока нет

- Sharpe RatioДокумент7 страницSharpe RatioSindhuja PalanichamyОценок пока нет

- FMChapter 4Документ3 страницыFMChapter 4Amit SukhaniОценок пока нет

- Ecf350 FPD 10 2021 1Документ33 страницыEcf350 FPD 10 2021 1elishankampila3500Оценок пока нет

- Chapter - 4 Data AnalysisДокумент56 страницChapter - 4 Data AnalysisSAGAR KHATUAОценок пока нет

- Ratios in Mutual FundsДокумент6 страницRatios in Mutual FundsAnshu SinghОценок пока нет

- Tutorial 3-IpmДокумент6 страницTutorial 3-IpmNguyễn Phương ThảoОценок пока нет

- Introduction To Financial Economics Financial Markets-Types Interest Rates Theory - Influence Financial Instruments Financial InstitutionsДокумент10 страницIntroduction To Financial Economics Financial Markets-Types Interest Rates Theory - Influence Financial Instruments Financial InstitutionsChinmay ShirsatОценок пока нет

- FEMAДокумент51 страницаFEMAChinmay Shirsat50% (2)

- 02 B&i-2010fДокумент9 страниц02 B&i-2010fChinmay ShirsatОценок пока нет

- Raising Long-Term Finance: Chinmay Shirsat (M1212) ASHWYN RAO (M1209)Документ22 страницыRaising Long-Term Finance: Chinmay Shirsat (M1212) ASHWYN RAO (M1209)Chinmay ShirsatОценок пока нет

- Relative Valuations FINALДокумент44 страницыRelative Valuations FINALChinmay ShirsatОценок пока нет

- Fabex NewsДокумент1 страницаFabex NewsChinmay ShirsatОценок пока нет

- Fabex Share Price Movement FinalДокумент20 страницFabex Share Price Movement FinalChinmay ShirsatОценок пока нет

- Fabex Price MovementДокумент17 страницFabex Price MovementChinmay ShirsatОценок пока нет

- Rules of FabexДокумент7 страницRules of FabexChinmay ShirsatОценок пока нет

- Fabex: The Stock Exchange Simulation Out Line of The ProgrammeДокумент1 страницаFabex: The Stock Exchange Simulation Out Line of The ProgrammeChinmay ShirsatОценок пока нет

- HOW Engaged Are My Employees?Документ8 страницHOW Engaged Are My Employees?Chinmay ShirsatОценок пока нет

- Balancing Fiscal Consolidation With Growth: Uncertainty Over GAARДокумент42 страницыBalancing Fiscal Consolidation With Growth: Uncertainty Over GAARChinmay ShirsatОценок пока нет

- Cap Budegt ProbsДокумент4 страницыCap Budegt ProbsAR Ananth Rohith BhatОценок пока нет

- Business Plan Format Commercial BankДокумент5 страницBusiness Plan Format Commercial Bankassefamenelik1100% (2)

- Derivatives: A Presentation by Harita Chanda Sneha Rampalli Nilesh KotereДокумент15 страницDerivatives: A Presentation by Harita Chanda Sneha Rampalli Nilesh KotereNilesh KotereОценок пока нет

- PDFДокумент188 страницPDFmcampuzaОценок пока нет

- Net Present Value (NPV) vs. Internal Rate of Return (IRR)Документ14 страницNet Present Value (NPV) vs. Internal Rate of Return (IRR)Mahmoud MorsiОценок пока нет

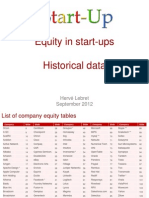

- Equity Split in Start-Up With Venture Capital - LebretДокумент177 страницEquity Split in Start-Up With Venture Capital - LebretHerve LebretОценок пока нет

- Navigating The Dynamics of Finance - A Brief OverviewДокумент1 страницаNavigating The Dynamics of Finance - A Brief Overviewsyedmoeen2001Оценок пока нет

- Tax-Smart Investing: What Australian Property Investors Need To KnowДокумент6 страницTax-Smart Investing: What Australian Property Investors Need To KnowYing ShiОценок пока нет

- Teil 6 Foreclosure FraudДокумент26 страницTeil 6 Foreclosure FraudNathan BeamОценок пока нет

- A G Gardiner EssaysДокумент50 страницA G Gardiner Essayszzcpllaeg100% (2)

- Busfin Final FinalДокумент36 страницBusfin Final FinalSheena Mae PeraltaОценок пока нет

- Specom 8Документ2 страницыSpecom 8jon jonОценок пока нет

- Ratios Analysis Notes AND ONE SOLVED QUIZДокумент6 страницRatios Analysis Notes AND ONE SOLVED QUIZDaisy Wangui100% (1)

- Chapter 01 Multinational Financial Management An OverviewДокумент6 страницChapter 01 Multinational Financial Management An OverviewmahraОценок пока нет

- In Vertical Mergers and Acquisition What Synergies Exist?Документ5 страницIn Vertical Mergers and Acquisition What Synergies Exist?Sanam TОценок пока нет

- Technical Derivatives 03-04-2024Документ6 страницTechnical Derivatives 03-04-2024fazalrehanОценок пока нет

- Chapter 5Документ4 страницыChapter 5Kishor R MusaleОценок пока нет

- Chapter 2 Premium LiabilityДокумент18 страницChapter 2 Premium LiabilityClarissa Atillano FababairОценок пока нет

- Business Advisor - December 25, 2012 - PreviewДокумент30 страницBusiness Advisor - December 25, 2012 - PreviewD. MuraliОценок пока нет

- Forex For Beginners Anna CoullingДокумент1 страницаForex For Beginners Anna CoullingQueОценок пока нет

- Fin546 Article Review ZainoorДокумент4 страницыFin546 Article Review ZainoorZAINOOR IKMAL MAISARAH MOHAMAD NOORОценок пока нет

- Testing Weak Form Efficiency For Indian Derivatives MarketДокумент4 страницыTesting Weak Form Efficiency For Indian Derivatives MarketVasantha NaikОценок пока нет

- Topic 1Документ5 страницTopic 1fazlinhashimОценок пока нет

- Lecture 4 - The Term Structure of Interest RatesДокумент14 страницLecture 4 - The Term Structure of Interest RatesDung ThùyОценок пока нет

- Online Trading ProposalДокумент14 страницOnline Trading ProposalAlex CurtoisОценок пока нет

- Project On NJ India Invest PVT LTDДокумент68 страницProject On NJ India Invest PVT LTDbabloo200650% (2)

- Ratio AnalysisДокумент71 страницаRatio AnalysisSubramanya DgОценок пока нет