Вам также может понравиться

- P - Fraud Risk InquiriesДокумент4 страницыP - Fraud Risk InquiriesHis HerОценок пока нет

- FRAUD Risk Assessment TemplateДокумент10 страницFRAUD Risk Assessment TemplaterickmortyОценок пока нет

- Ex-Logitech CFO Accused of Inflating Income Through Improper AccountingДокумент3 страницыEx-Logitech CFO Accused of Inflating Income Through Improper AccountingAgung KurniawanОценок пока нет

- Out - 28 IT FraudДокумент41 страницаOut - 28 IT FraudNur P UtamiОценок пока нет

- Fraud IndicatorsДокумент26 страницFraud IndicatorsIena SharinaОценок пока нет

- Managing Fraud Risks with the Fraud DiamondДокумент5 страницManaging Fraud Risks with the Fraud DiamondveranitaОценок пока нет

- A BILL To Terminate The Home Affordable Modification Program of The Department of The TreasuryДокумент4 страницыA BILL To Terminate The Home Affordable Modification Program of The Department of The TreasuryForeclosure FraudОценок пока нет

- Fraud 101Документ3 страницыFraud 101YesCFOОценок пока нет

- IBM Banking: Financial Crime SolutionsДокумент2 страницыIBM Banking: Financial Crime SolutionsIBMBankingОценок пока нет

- ACFE FinTech Fraud Summit PresentationДокумент16 страницACFE FinTech Fraud Summit PresentationCrowdfundInsider100% (1)

- Research Paper (Comparative Analysis of Global Financial Laws)Документ17 страницResearch Paper (Comparative Analysis of Global Financial Laws)Soumya SaranjiОценок пока нет

- Introduction, Conceptual Framework of The Study & Research DesignДокумент16 страницIntroduction, Conceptual Framework of The Study & Research DesignSтυριd・ 3尺ㄖ尺Оценок пока нет

- Investment PlanningДокумент18 страницInvestment PlanningNitesh BhaktaОценок пока нет

- Fraud Detection & ControlДокумент104 страницыFraud Detection & ControlHenry Hardoon100% (2)

- Fraud Pentagon Theory Influences Detection of Financial Statement FraudДокумент14 страницFraud Pentagon Theory Influences Detection of Financial Statement FraudChill GouvtfrondОценок пока нет

- Computer Fraud and Abuse TechniquesДокумент12 страницComputer Fraud and Abuse TechniquesSufrizal ChaniagoОценок пока нет

- Money LaundringДокумент21 страницаMoney LaundringHaris MashoodОценок пока нет

- Fraud in AccountingДокумент10 страницFraud in AccountingDwi Putra Rachmad AbdillahОценок пока нет

- Forensic AccountingДокумент12 страницForensic Accountingrazali mohammed0% (1)

- Fraud Prevention and Detection StrategiesДокумент30 страницFraud Prevention and Detection StrategiesTan DizzleОценок пока нет

- AKMEN Relevant CostДокумент25 страницAKMEN Relevant Costriadi wolfОценок пока нет

- Accounting Information System - Chapter 2Документ88 страницAccounting Information System - Chapter 2Melisa May Ocampo AmpiloquioОценок пока нет

- Fraud Detection in Banking Using Data MiningДокумент5 страницFraud Detection in Banking Using Data MiningMeena BhagatОценок пока нет

- Understanding IC and COSO 2013Документ37 страницUnderstanding IC and COSO 2013fred_barillo09100% (1)

- Forensic vs Investigative Audit GuideДокумент44 страницыForensic vs Investigative Audit GuideRegsa Agstaria100% (1)

- Fi 10032020Документ46 страницFi 10032020CA. (Dr.) Rajkumar Satyanarayan AdukiaОценок пока нет

- FraudДокумент7 страницFraudnhsajibОценок пока нет

- Internet Fraud 6monthreport 2000 AДокумент14 страницInternet Fraud 6monthreport 2000 AFlaviub23Оценок пока нет

- Fraud Prevention and DetectionДокумент3 страницыFraud Prevention and DetectionTahir AbbasОценок пока нет

- Fraud AuditingДокумент38 страницFraud AuditingTauqeer100% (3)

- Fraud Prevention PolicyДокумент2 страницыFraud Prevention PolicyAbhishek KumarОценок пока нет

- FisДокумент27 страницFisForeclosure Fraud100% (1)

- Continuous Fraud DetectionДокумент23 страницыContinuous Fraud Detectionbudi.hw748Оценок пока нет

- Regtech Problem StatementsДокумент72 страницыRegtech Problem StatementsVenp Pe100% (1)

- Data-Driven Fraud Detection: Bwanika NajibДокумент34 страницыData-Driven Fraud Detection: Bwanika NajibdhynaОценок пока нет

- Eliminating Corporate Fraud Through Strong GovernanceДокумент11 страницEliminating Corporate Fraud Through Strong GovernanceAakanksha MunjhalОценок пока нет

- Fraud DetectionДокумент9 страницFraud DetectionBon Carlo Medina MelocotonОценок пока нет

- Forensic Accounting FinДокумент33 страницыForensic Accounting FinakanshagОценок пока нет

- Adaptive Fraud DetectionДокумент4 страницыAdaptive Fraud DetectionBigmano Kc100% (1)

- Managing fraud risk at Summit ConsultingДокумент48 страницManaging fraud risk at Summit ConsultingMustapha MugisaОценок пока нет

- Fraud Audit - Kelompok 10 - Consumen Fraud - FinalДокумент56 страницFraud Audit - Kelompok 10 - Consumen Fraud - Finalmeilisa nugrahaОценок пока нет

- Anti-Fraud Strategy Technical NoteДокумент35 страницAnti-Fraud Strategy Technical NotePUTRI DAMAYANTI PANJAITAN TBA100% (1)

- Acfe Anti Fraud Technology 110652Документ28 страницAcfe Anti Fraud Technology 110652Jorge AmayaОценок пока нет

- Albrecht Chap 18Документ36 страницAlbrecht Chap 18Mairene CastroОценок пока нет

- Demat Account Fraud - How To Safeguard Against Demat Account FraudДокумент2 страницыDemat Account Fraud - How To Safeguard Against Demat Account FraudJayaprakash Muthuvat100% (1)

- Fraud Risk Document With AppendixДокумент17 страницFraud Risk Document With AppendixNathalie PadillaОценок пока нет

- FL 5th DCA Summary Judgment Reversed - Stephanie J. Crown V Chase Home FinanceДокумент3 страницыFL 5th DCA Summary Judgment Reversed - Stephanie J. Crown V Chase Home FinanceForeclosure FraudОценок пока нет

- 191 Cases: Fraud in NonprofitsДокумент2 страницы191 Cases: Fraud in NonprofitsYus CeballosОценок пока нет

- Agent Compliance Due Diligence ProcedureДокумент17 страницAgent Compliance Due Diligence ProcedureTran Maithoa100% (1)

- Functions and Roles of the Financial SystemДокумент33 страницыFunctions and Roles of the Financial SystemtanzirkhanОценок пока нет

- College Fraud Prevention PolicyДокумент4 страницыCollege Fraud Prevention PolicyFerdinand MangaoangОценок пока нет

- Fraud Risk Factors and Auditing Standards: An Integrated Identification of A Fraud Risk Management ModelДокумент270 страницFraud Risk Factors and Auditing Standards: An Integrated Identification of A Fraud Risk Management ModelAnupam BaliОценок пока нет

- CFDG Fraud Policy PDFДокумент6 страницCFDG Fraud Policy PDFSanath FernandoОценок пока нет

- Banking Presentation Final - 4Документ34 страницыBanking Presentation Final - 4Ganesh Nair100% (1)

- Fraud Control Jul08Документ46 страницFraud Control Jul08hmedlamineОценок пока нет

- Fraud Triangle ExplainedДокумент3 страницыFraud Triangle Explainedcoleen paraynoОценок пока нет

- Content Fraud BrainstormingДокумент6 страницContent Fraud BrainstormingHaris BurneyОценок пока нет

- Satyam ScamДокумент4 страницыSatyam ScamNitin Kumar100% (3)

- Arenglish2013 14Документ148 страницArenglish2013 14Nitin KumarОценок пока нет

- Telecom: U. B. DesaiДокумент30 страницTelecom: U. B. DesaiNitin KumarОценок пока нет

- ECG ReportДокумент1 страницаECG ReportNitin KumarОценок пока нет

- Success Factors For SDWTДокумент1 страницаSuccess Factors For SDWTNitin KumarОценок пока нет

- Telecom IndustryДокумент47 страницTelecom IndustryNitin KumarОценок пока нет

- DDDДокумент58 страницDDDNitin KumarОценок пока нет

- Telecom Industry - Section C.potxДокумент182 страницыTelecom Industry - Section C.potxNitin KumarОценок пока нет

- His Tor y of Telecommun Ica Tion in Ind Ia: India N Tel Eco M Sect orДокумент79 страницHis Tor y of Telecommun Ica Tion in Ind Ia: India N Tel Eco M Sect orapurvaaaОценок пока нет

- Telecom Industry1Документ47 страницTelecom Industry1Nitin KumarОценок пока нет

- A Project Report On Orgnoziation Study of Tata MotorsДокумент51 страницаA Project Report On Orgnoziation Study of Tata MotorsBabasab Patil (Karrisatte)Оценок пока нет

- Telecom Industry Group10Документ47 страницTelecom Industry Group10Nitin KumarОценок пока нет

- Telecom Industry: Consulting Club, IIM CalcuttaДокумент6 страницTelecom Industry: Consulting Club, IIM CalcuttaNitin KumarОценок пока нет

- Strengths WeaknessesДокумент2 страницыStrengths WeaknessesNitin KumarОценок пока нет

- 5Документ7 страниц5ashish.bms9Оценок пока нет

- About Cloud Computing and Application:: About Smart Grid SolutionДокумент2 страницыAbout Cloud Computing and Application:: About Smart Grid SolutionNitin KumarОценок пока нет

- Sesa Goa AR12-13 - WebДокумент148 страницSesa Goa AR12-13 - WebNitin KumarОценок пока нет

- DDDДокумент58 страницDDDNitin KumarОценок пока нет

- Q2Документ2 страницыQ2Nitin KumarОценок пока нет

- Q2Документ2 страницыQ2Nitin KumarОценок пока нет

- Strengths WeaknessesДокумент2 страницыStrengths WeaknessesNitin KumarОценок пока нет

- Seven Categories of The Business CriteriaДокумент17 страницSeven Categories of The Business CriteriaNitin KumarОценок пока нет

- About Cloud Computing and Application:: About Smart Grid SolutionДокумент2 страницыAbout Cloud Computing and Application:: About Smart Grid SolutionNitin KumarОценок пока нет

- Mbti Sahil Dua: Trait Score PercentileДокумент2 страницыMbti Sahil Dua: Trait Score PercentileNitin KumarОценок пока нет

- Question and Answer Samples and TechniquesДокумент8 страницQuestion and Answer Samples and TechniquesNitin KumarОценок пока нет

- FMEA Template: Item FunctionДокумент13 страницFMEA Template: Item FunctionNitin KumarОценок пока нет

- Question and Answer Samples and TechniquesДокумент8 страницQuestion and Answer Samples and TechniquesNitin KumarОценок пока нет

- Question and Answer Samples and TechniquesДокумент8 страницQuestion and Answer Samples and TechniquesNitin KumarОценок пока нет

- Question and Answer Samples and TechniquesДокумент8 страницQuestion and Answer Samples and TechniquesNitin KumarОценок пока нет

- Supply Chain Management (3rd Edition)Документ33 страницыSupply Chain Management (3rd Edition)Pranav VyasОценок пока нет

- Project Proposal: Title of The ProjectДокумент2 страницыProject Proposal: Title of The ProjectNitin KumarОценок пока нет

- Nandini Ji QuestionaireДокумент4 страницыNandini Ji QuestionaireANKIT SINGHОценок пока нет

- Duties and Responsibilities of Internal AuditorДокумент2 страницыDuties and Responsibilities of Internal AuditorNadeimkhan100% (6)

- Gross Revenue Sharing Pool AgreementДокумент15 страницGross Revenue Sharing Pool AgreementKnowledge GuruОценок пока нет

- ASM Nahidul Haque Assignment #6 ProblemsДокумент2 страницыASM Nahidul Haque Assignment #6 ProblemsNahid HawkОценок пока нет

- Absorption Vs VariableДокумент10 страницAbsorption Vs VariableRonie Macasabuang CardosaОценок пока нет

- Three and Five Stage DuPont Analysis of Maruti Suzuki, Mahindra & Mahindra, and Tata MotorsДокумент2 страницыThree and Five Stage DuPont Analysis of Maruti Suzuki, Mahindra & Mahindra, and Tata MotorsVimal AgrawalОценок пока нет

- Saiful Bari - 1531367060 - Internship ReportДокумент50 страницSaiful Bari - 1531367060 - Internship ReportMaria Iqbal Diya 1430598630Оценок пока нет

- CH 02Документ13 страницCH 02Harnita PriyaniОценок пока нет

- Certified Risk Management Professional (CRMP)Документ2 страницыCertified Risk Management Professional (CRMP)DesuyОценок пока нет

- MAS NotesДокумент3 страницыMAS NotesMaricon Rillera PatauegОценок пока нет

- P5-1A Dan P5-2AДокумент6 страницP5-1A Dan P5-2ASherly Meliana Geraldine100% (1)

- Appendix 14: Corporate Governance Code and Corporate Governance ReportДокумент31 страницаAppendix 14: Corporate Governance Code and Corporate Governance ReportVivianОценок пока нет

- 250+ Imp AuditДокумент289 страниц250+ Imp Auditboring filesОценок пока нет

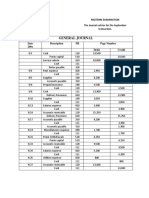

- General Journal: Eva D. Manalo BSHM-1 B3 Midterm Examination The Journal Entries For The September TransactionДокумент3 страницыGeneral Journal: Eva D. Manalo BSHM-1 B3 Midterm Examination The Journal Entries For The September TransactionKaren OribeОценок пока нет

- ACCA AA (F8) Course Notes PDFДокумент258 страницACCA AA (F8) Course Notes PDFayesha najam100% (2)

- Landbank of The PhilippinesДокумент33 страницыLandbank of The PhilippinesRejean Dela CruzОценок пока нет

- 1Z0-511 Exam DumpsДокумент6 страниц1Z0-511 Exam DumpsExamDumpsОценок пока нет

- Notes on adjustments to Financial StatementsДокумент4 страницыNotes on adjustments to Financial StatementsErynОценок пока нет

- Service - Journal-TB - Dr. Who ClinicДокумент11 страницService - Journal-TB - Dr. Who ClinicJasmine Acta67% (3)

- Answer Key (Adv - Acctg222) FINALДокумент6 страницAnswer Key (Adv - Acctg222) FINALAnonymous dbNSSxXPBОценок пока нет

- Deposit Slip PDFДокумент2 страницыDeposit Slip PDFLalit PardasaniОценок пока нет

- Guide to Internal Controls and Compliance for Securities BrokersДокумент25 страницGuide to Internal Controls and Compliance for Securities Brokerszubair_zОценок пока нет

- CP 3Документ50 страницCP 3Mohammad FaridОценок пока нет

- Question 1: (3 Points)Документ9 страницQuestion 1: (3 Points)Akmal ShahzadОценок пока нет

- PADAGDAGДокумент19 страницPADAGDAGKathleen Tatierra ArambalaОценок пока нет

- Economic Versus Non-Economic Factors: An Analysis of Corporate Tax ComplianceДокумент38 страницEconomic Versus Non-Economic Factors: An Analysis of Corporate Tax ComplianceNur Adilah RoslanОценок пока нет

- BallДокумент3 страницыBallYsabelle Yu YagoОценок пока нет

- CIR Appeals CTA Ruling on ICC Tax DeductionsДокумент4 страницыCIR Appeals CTA Ruling on ICC Tax DeductionsJane MarianОценок пока нет

- Bank of BarodaДокумент28 страницBank of BarodaVincent KaburuОценок пока нет

- Principles of GovernanceДокумент6 страницPrinciples of GovernanceJerome B. AgliamОценок пока нет