Вам также может понравиться

- Option StrategiesДокумент9 страницOption StrategiesSatya Kumar100% (1)

- BondsДокумент55 страницBondsfecaxeyivuОценок пока нет

- Spotting Trend Reversals With MACDДокумент3 страницыSpotting Trend Reversals With MACDnypb2000100% (3)

- Valuation of BondsДокумент49 страницValuation of BondsSanjit SinhaОценок пока нет

- Technical Graphical Analysis EbookДокумент66 страницTechnical Graphical Analysis EbookAngeli Pirvulescu100% (5)

- Financial Risk Management: A Simple IntroductionОт EverandFinancial Risk Management: A Simple IntroductionРейтинг: 4.5 из 5 звезд4.5/5 (7)

- 5.1foreign Exchange Rate Determination and ForecastingДокумент34 страницы5.1foreign Exchange Rate Determination and ForecastingSanaFatimaОценок пока нет

- Chapter 6 - Bond Valuation and Interest RatesДокумент36 страницChapter 6 - Bond Valuation and Interest RatesAmeer B. BalochОценок пока нет

- 9.1 Operating ExposureДокумент28 страниц9.1 Operating ExposureSanaFatimaОценок пока нет

- Bond Yields DurationДокумент18 страницBond Yields DurationKaranbir Singh RandhawaОценок пока нет

- Overview of Capital MarketsДокумент31 страницаOverview of Capital MarketsDiwakar BhargavaОценок пока нет

- Applied Corporate Finance. What is a Company worth?От EverandApplied Corporate Finance. What is a Company worth?Рейтинг: 3 из 5 звезд3/5 (2)

- Chapter 12 Bond Portfolio MGMTДокумент41 страницаChapter 12 Bond Portfolio MGMTsharktale2828Оценок пока нет

- Yield Curve Analysis and Fixed-Income ArbitrageДокумент33 страницыYield Curve Analysis and Fixed-Income Arbitrageandrewfu1988Оценок пока нет

- Immunization StrategiesДокумент75 страницImmunization StrategiesSarang GuptaОценок пока нет

- Time Value of Money: Practical Application of Compounding & DiscountingДокумент32 страницыTime Value of Money: Practical Application of Compounding & DiscountingSaurabh RajputОценок пока нет

- Introduction To Capital MarketsДокумент46 страницIntroduction To Capital MarketsSushobhita Rath100% (4)

- Chap 014Документ79 страницChap 014hanguyenhihiОценок пока нет

- Securities TradingДокумент51 страницаSecurities TradingameetavoОценок пока нет

- Term Structure of Interest RatesДокумент21 страницаTerm Structure of Interest RatestoabhishekpalОценок пока нет

- Fixed Income - Toto - 7Документ44 страницыFixed Income - Toto - 7sagita fОценок пока нет

- Financial Management - Bonds 2014Документ34 страницыFinancial Management - Bonds 2014Joe ChungОценок пока нет

- Valuation of SecuritiesДокумент43 страницыValuation of SecuritiesVaidyanathan RavichandranОценок пока нет

- Lecture 3Документ29 страницLecture 3Nurfaiqah AmniОценок пока нет

- Business School: ACTL4303 AND ACTL5303 Asset Liability ManagementДокумент62 страницыBusiness School: ACTL4303 AND ACTL5303 Asset Liability ManagementBobОценок пока нет

- Interest Rate Models and Derivatives 2019Документ69 страницInterest Rate Models and Derivatives 2019Elisha MakoniОценок пока нет

- Debt - Investment Drivers & ApproachesДокумент26 страницDebt - Investment Drivers & ApproachesMisba KhanОценок пока нет

- Valuation of Securities: - Debentures (Bonds) - Preference Shares - Equity SharesДокумент42 страницыValuation of Securities: - Debentures (Bonds) - Preference Shares - Equity SharesVivek RoyОценок пока нет

- Lecture 6 - Interest Rates and Bond ValuationДокумент61 страницаLecture 6 - Interest Rates and Bond ValuationDaniel HakimОценок пока нет

- 0 20200519134342understanding of Loans and Bonds Part 2 PDFДокумент19 страниц0 20200519134342understanding of Loans and Bonds Part 2 PDFWalter WhiteОценок пока нет

- Chapter 8 Interest Risk IДокумент46 страницChapter 8 Interest Risk ISabrina Karim0% (1)

- Derivatives 5 MFIN SwapsДокумент59 страницDerivatives 5 MFIN SwapsNan XiangОценок пока нет

- Time Value of Money, Compounding and DiscountingДокумент6 страницTime Value of Money, Compounding and DiscountingAmenahОценок пока нет

- Corp FinДокумент45 страницCorp FinSoe Group 1Оценок пока нет

- Chapter 11 Bond Prices and YieldsДокумент36 страницChapter 11 Bond Prices and Yieldssharktale2828Оценок пока нет

- Chapter 2 - How To Calculate Present ValuesДокумент36 страницChapter 2 - How To Calculate Present ValuesDeok NguyenОценок пока нет

- Cost of CapitalДокумент19 страницCost of Capitalshraddha amatyaОценок пока нет

- Interest Rates and Bond Valuation: All Rights ReservedДокумент28 страницInterest Rates and Bond Valuation: All Rights ReservedFahad ChowdhuryОценок пока нет

- Time Value of Money (TVM)Документ5 страницTime Value of Money (TVM)Yesha Jade SaturiusОценок пока нет

- FM PPT 1Документ59 страницFM PPT 1nivethapraveenОценок пока нет

- YeahДокумент2 страницыYeahMoimen Dalinding UttoОценок пока нет

- Valuation of Bonds and SharesДокумент21 страницаValuation of Bonds and ShareszlnpjbcckbeqwnzgojОценок пока нет

- Term Structure and Risk StructureДокумент28 страницTerm Structure and Risk StructureAdina CasianaОценок пока нет

- Financial Management: by K Lubza NiharДокумент21 страницаFinancial Management: by K Lubza NiharAashutosh MishraОценок пока нет

- Finals HWK NotesДокумент24 страницыFinals HWK NotesbenОценок пока нет

- Interest Rates and Risk PremiumДокумент36 страницInterest Rates and Risk PremiumPrathiba PereraОценок пока нет

- WK13-14 Valuation and Rates of ReturnДокумент49 страницWK13-14 Valuation and Rates of ReturnJAEZAR PHILIP GRAGASINОценок пока нет

- Chapter 2 - Interest Rates - SДокумент117 страницChapter 2 - Interest Rates - STuong Vi Nguyen PhanОценок пока нет

- How To Calculate Present Values: Principles of Corporate FinanceДокумент41 страницаHow To Calculate Present Values: Principles of Corporate FinanceSalehEdelbiОценок пока нет

- Chapter 8 - The Term Structure of Interest RateДокумент28 страницChapter 8 - The Term Structure of Interest RateDuy MinhОценок пока нет

- Asset Liability ManagementДокумент32 страницыAsset Liability ManagementAshish ShahОценок пока нет

- Interest Rate Risk I (CH 8)Документ13 страницInterest Rate Risk I (CH 8)Mahbub TalukderОценок пока нет

- Providence College School of Business: FIN 417 Fixed Income Securities Fall 2021 Instructor: Matthew CallahanДокумент51 страницаProvidence College School of Business: FIN 417 Fixed Income Securities Fall 2021 Instructor: Matthew CallahanAlexander MaffeoОценок пока нет

- Discounted Cash Flow Valuation: Rights Reserved Mcgraw-Hill/IrwinДокумент48 страницDiscounted Cash Flow Valuation: Rights Reserved Mcgraw-Hill/IrwinEnna rajpootОценок пока нет

- AFM 204 - Class 7 Slides - Cost of EquityДокумент49 страницAFM 204 - Class 7 Slides - Cost of Equityasflkhaf2Оценок пока нет

- Bond ValuationДокумент46 страницBond ValuationNor Shakirah ShariffuddinОценок пока нет

- Week 2 Lecture Slides - Ch02Документ39 страницWeek 2 Lecture Slides - Ch02LuanОценок пока нет

- Bond Valuation 000000001Документ41 страницаBond Valuation 000000001Subrata BagОценок пока нет

- Session5 7Документ42 страницыSession5 7Abhishek KashyapОценок пока нет

- Chap 14Документ25 страницChap 14rana sarfaraxОценок пока нет

- Time Value of MoneyДокумент30 страницTime Value of MoneyMoshmi MazumdarОценок пока нет

- 05 Lecture - The Time Value of Money PDFДокумент26 страниц05 Lecture - The Time Value of Money PDFjgutierrez_castro7724Оценок пока нет

- Fundamentals of Corporate Finance, 2/e: Robert Parrino, Ph.D. David S. Kidwell, Ph.D. Thomas W. Bates, PH.DДокумент41 страницаFundamentals of Corporate Finance, 2/e: Robert Parrino, Ph.D. David S. Kidwell, Ph.D. Thomas W. Bates, PH.DKhánh Linh PhanОценок пока нет

- BVДокумент62 страницыBVKetan BhanushaliОценок пока нет

- The Structure of Interest RatesДокумент72 страницыThe Structure of Interest RatesMarwa HassanОценок пока нет

- Bonds and The Term Structure of Interest RatesДокумент29 страницBonds and The Term Structure of Interest RatesZUNERAKHALIDОценок пока нет

- 7 EFM Class 6 Financial NeedДокумент68 страниц7 EFM Class 6 Financial NeedSiu EricОценок пока нет

- Bond Evaluation - FinalДокумент14 страницBond Evaluation - FinalNishant PokleОценок пока нет

- Lancashire Business School: MD4003 - Management Theory and PracticeДокумент9 страницLancashire Business School: MD4003 - Management Theory and PracticeSanaFatimaОценок пока нет

- 7.0 Does Debt Policy MatterДокумент22 страницы7.0 Does Debt Policy MatterSanaFatimaОценок пока нет

- 6.0 Poyout PolicyДокумент28 страниц6.0 Poyout PolicySanaFatimaОценок пока нет

- 4.3 Q MiniCase Turkish Kriz (A)Документ6 страниц4.3 Q MiniCase Turkish Kriz (A)SanaFatimaОценок пока нет

- 2.2 FX MiniCase Venezuelan BolivarДокумент4 страницы2.2 FX MiniCase Venezuelan BolivarSanaFatimaОценок пока нет

- 5.2 Q JPMorgan Chase FXДокумент7 страниц5.2 Q JPMorgan Chase FXSanaFatimaОценок пока нет

- 3.1 International Parity ConditionsДокумент41 страница3.1 International Parity ConditionsSanaFatimaОценок пока нет

- Country RiskДокумент42 страницыCountry RiskmandarcoolОценок пока нет

- Blue Chip Stocks TipsДокумент16 страницBlue Chip Stocks TipsPinal MehtaОценок пока нет

- ID Analisis Rasio Keuangan Dan Metode EconoДокумент9 страницID Analisis Rasio Keuangan Dan Metode Econo1878 saiful 1927 bonek red devilОценок пока нет

- Reduction of Portfolio Through DiversificationДокумент28 страницReduction of Portfolio Through DiversificationDilshaad ShaikhОценок пока нет

- Questionnaire MДокумент4 страницыQuestionnaire MSubhasisChatterjeeОценок пока нет

- Rising Wedge Article PDFДокумент13 страницRising Wedge Article PDFKiran KrishnaОценок пока нет

- Forex 101Документ18 страницForex 101Geoffrey Castillon RamirezОценок пока нет

- S 26 eДокумент2 страницыS 26 eMichael WestОценок пока нет

- Balance of Payments: Chapter ThreeДокумент36 страницBalance of Payments: Chapter ThreeHu Jia QuenОценок пока нет

- Multibagger Stock Ideas2Документ16 страницMultibagger Stock Ideas2KannanОценок пока нет

- Qualifying Job Titles For FRM CertificationДокумент6 страницQualifying Job Titles For FRM CertificationAnoop TyagiОценок пока нет

- Chapter 1 - AFP313Документ34 страницыChapter 1 - AFP313Mah Chee SiongОценок пока нет

- K-10 Colgate Palmolive 1994-1992Документ96 страницK-10 Colgate Palmolive 1994-1992salwanahotmailcomОценок пока нет

- TCQTTTДокумент32 страницыTCQTTTdohongvinh40Оценок пока нет

- Mutual Fund ProjectДокумент35 страницMutual Fund ProjectKripal SinghОценок пока нет

- Za Test 8 KumarДокумент30 страницZa Test 8 KumarMia Omerika100% (1)

- The Profit and Loss Appropriation AccountДокумент4 страницыThe Profit and Loss Appropriation AccountSarthak GuptaОценок пока нет

- Cost-Volume-Profit Analysis: Slide 3-28Документ15 страницCost-Volume-Profit Analysis: Slide 3-28SambuttОценок пока нет

- Some ExercisesДокумент3 страницыSome ExercisesMinh Tâm NguyễnОценок пока нет

- Sanjeevani Forex Education RewДокумент34 страницыSanjeevani Forex Education RewfaiyazaslamОценок пока нет

- Coal TradersДокумент4 страницыCoal TradersDouglas SuarezОценок пока нет

- Forex Trading by Money Market, BNGДокумент69 страницForex Trading by Money Market, BNGsachinmehta1978Оценок пока нет

- UntitledДокумент15 страницUntitledkayal_vizhi_6Оценок пока нет

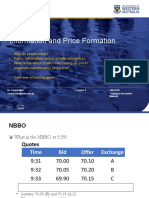

- Information and Price FormationДокумент36 страницInformation and Price FormationDylan AdrianОценок пока нет

- Foreign Currency TransactionsДокумент40 страницForeign Currency TransactionsJuliaMaiLeОценок пока нет