Вам также может понравиться

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Word Business Case TemplateДокумент5 страницWord Business Case TemplateSanthosh Kumar Setty100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- People V CaparasДокумент3 страницыPeople V CaparasFrederick Xavier LimОценок пока нет

- CAT UniversityДокумент31 страницаCAT Universityaskvishnu7112Оценок пока нет

- DOLE v. Maritime Company of The PhilsДокумент2 страницыDOLE v. Maritime Company of The PhilsFrederick Xavier LimОценок пока нет

- CIR V CTA Manila GolfДокумент2 страницыCIR V CTA Manila GolfFrederick Xavier LimОценок пока нет

- CIR V CTA Manila GolfДокумент2 страницыCIR V CTA Manila GolfFrederick Xavier LimОценок пока нет

- A Guide To Calculating Return On Investment (ROI) - InvestopediaДокумент9 страницA Guide To Calculating Return On Investment (ROI) - InvestopediaBob KaneОценок пока нет

- Espinoza V UOBДокумент1 страницаEspinoza V UOBFrederick Xavier LimОценок пока нет

- Retail Math'Sppt1Документ40 страницRetail Math'Sppt1nataraj105100% (8)

- People v. Almazan DigestДокумент1 страницаPeople v. Almazan DigestFrederick Xavier LimОценок пока нет

- Assignment 11 Managerial AccountingДокумент9 страницAssignment 11 Managerial AccountingFaisal AlsharifiОценок пока нет

- Macaslang V ZamoraДокумент3 страницыMacaslang V ZamoraFrederick Xavier LimОценок пока нет

- B ST XI Subhash Dey All Chapters PPTs Teaching Made EasierДокумент1 627 страницB ST XI Subhash Dey All Chapters PPTs Teaching Made EasierAarush GuptaОценок пока нет

- Stott Pilates (PDFDrive) PDFДокумент99 страницStott Pilates (PDFDrive) PDFpaperhurtsОценок пока нет

- Automation ROIДокумент10 страницAutomation ROIskodliОценок пока нет

- Rabuco V VillegasДокумент2 страницыRabuco V VillegasFrederick Xavier LimОценок пока нет

- Pasag V ParochaДокумент3 страницыPasag V ParochaFrederick Xavier LimОценок пока нет

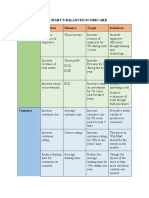

- Wal-Mart's Balanced ScorecardДокумент3 страницыWal-Mart's Balanced ScorecardCấn Thu HuyềnОценок пока нет

- Margarejo v. Escoses DigestДокумент1 страницаMargarejo v. Escoses DigestFrederick Xavier LimОценок пока нет

- D'Armoured v. OrpiaДокумент2 страницыD'Armoured v. OrpiaFrederick Xavier LimОценок пока нет

- Internship Report On Shakarganj Sugar Mill by SYED AHMAD MUSTAFAДокумент21 страницаInternship Report On Shakarganj Sugar Mill by SYED AHMAD MUSTAFAAhmad Mustafa100% (2)

- Cafe BoxДокумент21 страницаCafe BoxJhoanna Mary PescasioОценок пока нет

- PP V Candido DigestДокумент1 страницаPP V Candido DigestFrederick Xavier LimОценок пока нет

- Asset Management - Whole-Life Management of Physical AssetsДокумент285 страницAsset Management - Whole-Life Management of Physical AssetsAbhishek Goud Byrey100% (1)

- Marimperio v. CAДокумент5 страницMarimperio v. CAFrederick Xavier LimОценок пока нет

- Dela Vega V BallilosДокумент2 страницыDela Vega V BallilosFrederick Xavier LimОценок пока нет

- CIR V Gonzales 2010Документ4 страницыCIR V Gonzales 2010Frederick Xavier LimОценок пока нет

- Alitalia V IacДокумент3 страницыAlitalia V IacFrederick Xavier LimОценок пока нет

- Required Document ChecklistДокумент3 страницыRequired Document ChecklistFrederick Xavier LimОценок пока нет

- Peak Ventures V Villareal DigestДокумент1 страницаPeak Ventures V Villareal DigestFrederick Xavier LimОценок пока нет

- CMDI V CAДокумент3 страницыCMDI V CAFrederick Xavier LimОценок пока нет

- DBP Pool V Radio MindanaoДокумент3 страницыDBP Pool V Radio MindanaoFrederick Xavier LimОценок пока нет

- Estates Reyes V CIR (CTA)Документ2 страницыEstates Reyes V CIR (CTA)Frederick Xavier LimОценок пока нет

- Raz V IACДокумент2 страницыRaz V IACFrederick Xavier Lim100% (1)

- Chua Yek Hong V IACДокумент2 страницыChua Yek Hong V IACFrederick Xavier LimОценок пока нет

- HomeWork MCS-Nurul Sari (1101002048) - Case 5.1 5.4Документ5 страницHomeWork MCS-Nurul Sari (1101002048) - Case 5.1 5.4Nurul SariОценок пока нет

- Bowling Green Sports FacilityДокумент10 страницBowling Green Sports Facilityapi-377831528Оценок пока нет

- KMBN 301 Strategic Management Unit 5Документ20 страницKMBN 301 Strategic Management Unit 5kumar sahityaОценок пока нет

- FA Poject Nestle Vs EngroДокумент27 страницFA Poject Nestle Vs EngroNaveed Alei Shah67% (3)

- Saffer 2010 Chapter3 PDFДокумент26 страницSaffer 2010 Chapter3 PDFFabiano RamosОценок пока нет

- Case StudyДокумент32 страницыCase StudyAdee ButtОценок пока нет

- The Capital Adequacy Ratio in Pension FundsДокумент7 страницThe Capital Adequacy Ratio in Pension FundsInternational Journal of Innovative Science and Research TechnologyОценок пока нет

- Responsibility Accounting QuizДокумент4 страницыResponsibility Accounting QuizSetty HakeemaОценок пока нет

- Carrefour Expansion To Pakistan: International Business Management (MGT 521) Spring 2017-2018 (Term B)Документ23 страницыCarrefour Expansion To Pakistan: International Business Management (MGT 521) Spring 2017-2018 (Term B)WerchampiomsОценок пока нет

- ROI ChecklistДокумент2 страницыROI ChecklistTarig TahaОценок пока нет

- What Is The Anderson Model of Learning Evaluation?Документ9 страницWhat Is The Anderson Model of Learning Evaluation?துர்காதேவி சௌந்தரராஜன்100% (1)

- UNIT 1 - Planning & Evaluating OperationsДокумент22 страницыUNIT 1 - Planning & Evaluating OperationsGurneet Singh7113Оценок пока нет

- Responsibility Accounting AssignmentДокумент5 страницResponsibility Accounting AssignmentMikah LabacoОценок пока нет

- SaaS Acronyms Defined and Explained 6 PDFДокумент1 страницаSaaS Acronyms Defined and Explained 6 PDFRitin mahajanОценок пока нет

- ENTREP Lesson 5-7Документ10 страницENTREP Lesson 5-7FruitySaladОценок пока нет

- 123Документ1 страница123kristineОценок пока нет

- Test Maf651Документ4 страницыTest Maf651Zoe McKenzieОценок пока нет

- Performance 6.10Документ2 страницыPerformance 6.10George BulikiОценок пока нет