Вам также может понравиться

- SodaPDF-merged-Merging ResultДокумент15 страницSodaPDF-merged-Merging ResultzhuzhОценок пока нет

- Debit Aliran Metode RationalДокумент3 страницыDebit Aliran Metode RationalAnggun Vita MutiaraОценок пока нет

- Budget Presentation 15.09.2011Документ12 страницBudget Presentation 15.09.2011Raja RamОценок пока нет

- Corporate Finance - Exercises Session 1 - SolutionsДокумент5 страницCorporate Finance - Exercises Session 1 - SolutionsLouisRemОценок пока нет

- Rancob Hitung ManualДокумент8 страницRancob Hitung ManualAsnurОценок пока нет

- Oferta PDFДокумент67 страницOferta PDFAlexandru GhineaОценок пока нет

- Floodable Ni AlcaydeДокумент149 страницFloodable Ni AlcaydeAndronicoll Mayuga NovalОценок пока нет

- Polaroid CorporationДокумент14 страницPolaroid CorporationMandley SourabhОценок пока нет

- Ujian SOPДокумент136 страницUjian SOPsugendengalОценок пока нет

- Revised Xcel From AvniДокумент5 страницRevised Xcel From AvniHannah BlackОценок пока нет

- Investment Ass#6 - Daniyal Ali 18u00265Документ3 страницыInvestment Ass#6 - Daniyal Ali 18u00265Daniyal Ali100% (1)

- Lab4 FahmiGilangMadani 120110170024 Jumat10.30 KakAlissaДокумент7 страницLab4 FahmiGilangMadani 120110170024 Jumat10.30 KakAlissaFahmi GilangОценок пока нет

- Asignación A Cargo Del DecenteДокумент9 страницAsignación A Cargo Del DecenteGaby C.Оценок пока нет

- All in RatesДокумент17 страницAll in Ratesrkacquaye100% (1)

- Solution To Campbell Lo Mackinlay PDFДокумент71 страницаSolution To Campbell Lo Mackinlay PDFstaimouk0% (1)

- Waste ManagementДокумент18 страницWaste ManagementsmikaramОценок пока нет

- RSI CalculationsДокумент36 страницRSI CalculationsG. S. YadavОценок пока нет

- Math 101 Business and Consumer LoansДокумент31 страницаMath 101 Business and Consumer LoansAdi Garcia ArcenasОценок пока нет

- Home Work Excel SolutionДокумент16 страницHome Work Excel SolutionSunil KumarОценок пока нет

- NPV CalculationДокумент19 страницNPV CalculationmschotoОценок пока нет

- Continental CarriersДокумент3 страницыContinental CarriersCharleneОценок пока нет

- Chapter 10 Discounted DividendДокумент5 страницChapter 10 Discounted Dividendmahnoor javaidОценок пока нет

- Solution To 4.13Документ5 страницSolution To 4.13Niyati ShahОценок пока нет

- Table 8 Demographic Structure and MacroeconomyДокумент3 страницыTable 8 Demographic Structure and MacroeconomyzhuzhОценок пока нет

- Coca Cola Financial AnalysisДокумент4 страницыCoca Cola Financial AnalysisMohammad AliОценок пока нет

- Progres CL Nova Agt 16Документ37 страницProgres CL Nova Agt 16Aziz PediansyahОценок пока нет

- Pertemuan 4 - Contoh Perhitungan Tanpa NgelinkДокумент13 страницPertemuan 4 - Contoh Perhitungan Tanpa NgelinkNabila HusniatiОценок пока нет

- Rights IssueДокумент18 страницRights Issuemuthum44499335Оценок пока нет

- SolutionsДокумент3 страницыSolutionsSwathi JayaprakashОценок пока нет

- Tugas Klompok JerryДокумент9 страницTugas Klompok Jerryfajar sulaimanОценок пока нет

- Modelo WilsonДокумент14 страницModelo WilsonB. Lizet NuñezОценок пока нет

- Word Debit Aliran Metode RationalДокумент9 страницWord Debit Aliran Metode RationalAnggun Vita MutiaraОценок пока нет

- 2.4 Unsteady-State Pressure Distribution Calculations in Directional WellДокумент10 страниц2.4 Unsteady-State Pressure Distribution Calculations in Directional Wellسحر سلامتیانОценок пока нет

- Stanley BetДокумент113 страницStanley Betpetrica20Оценок пока нет

- Assignment 2 Question 1: 1A) Statement of Comprehensive IncomeДокумент17 страницAssignment 2 Question 1: 1A) Statement of Comprehensive IncomesmaОценок пока нет

- Development Sales Lacking: Wheelock Properties (S)Документ7 страницDevelopment Sales Lacking: Wheelock Properties (S)Theng RogerОценок пока нет

- Risk and Portfolio Management Spring 2011: Statistical ArbitrageДокумент66 страницRisk and Portfolio Management Spring 2011: Statistical ArbitrageSwapan ChakrabortyОценок пока нет

- Sample ValuationДокумент18 страницSample Valuationprasha99Оценок пока нет

- Detail P&L Jan Feb Mar Apr May: To ControlДокумент33 страницыDetail P&L Jan Feb Mar Apr May: To ControlmadhujayarajОценок пока нет

- Rain Water Basin DesignДокумент11 страницRain Water Basin DesignSturza AnastasiaОценок пока нет

- CANSLIM - PlantationДокумент17 страницCANSLIM - Plantationtok janggutОценок пока нет

- Ie8b05277 Si 001Документ20 страницIe8b05277 Si 001Nipun ChopraОценок пока нет

- Fixed Income Nmims BLR s6Документ22 страницыFixed Income Nmims BLR s6harshit.dwivedi320Оценок пока нет

- 6 CHP 13 14 15 SolutionДокумент21 страница6 CHP 13 14 15 SolutionBijay AgrawalОценок пока нет

- Coca-Cola Co: FinancialsДокумент6 страницCoca-Cola Co: FinancialsSibghaОценок пока нет

- Table 1a Two-Sided Critical Z-Values (: FunctionsДокумент5 страницTable 1a Two-Sided Critical Z-Values (: FunctionsJeffОценок пока нет

- LAPORAN UJI INDERAWI - Sri Sabili Rohmah - 173020109 - KEL.D - SCORINGДокумент4 страницыLAPORAN UJI INDERAWI - Sri Sabili Rohmah - 173020109 - KEL.D - SCORINGbudi rahmatОценок пока нет

- Ifa Completed Full AnswerДокумент25 страницIfa Completed Full AnswerEileen Wong100% (2)

- Ejercicio de Tirante Normal Con Flujo UniformeДокумент6 страницEjercicio de Tirante Normal Con Flujo UniformeMaira IbarguenОценок пока нет

- Baûng Tính Theùp Cho Phaàn Töû CoätДокумент3 страницыBaûng Tính Theùp Cho Phaàn Töû CoätNguyen Quoc LamОценок пока нет

- Tabel 3.1 Perhitungan Gumbel: Bab Iii Debit Banjir Rancangan Q50 THДокумент3 страницыTabel 3.1 Perhitungan Gumbel: Bab Iii Debit Banjir Rancangan Q50 THSari RahmawatiОценок пока нет

- Microsoft ValuationДокумент4 страницыMicrosoft ValuationcorvettejrwОценок пока нет

- Earth: Current Previous Close 2013 TP Exp Return Support Resistance CGR 2012 N/RДокумент4 страницыEarth: Current Previous Close 2013 TP Exp Return Support Resistance CGR 2012 N/RCamarada RojoОценок пока нет

- Acceleration of a geared system experiment: ω (j) / ω (i) = t (i) / t (j)Документ11 страницAcceleration of a geared system experiment: ω (j) / ω (i) = t (i) / t (j)jihad hasanОценок пока нет

- Descargas Rios LambayequeДокумент36 страницDescargas Rios LambayequeAngel AcuñaОценок пока нет

- EXCEL Modeli Upravljanja Troškovima - HP - XI - 2013Документ16 страницEXCEL Modeli Upravljanja Troškovima - HP - XI - 2013Ana MarkovićОценок пока нет

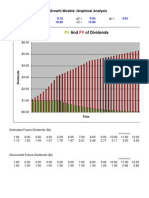

- And of Dividends: Divgraph: The Dividend Growth Models: Graphical AnalysisДокумент10 страницAnd of Dividends: Divgraph: The Dividend Growth Models: Graphical AnalysisSara LeeОценок пока нет

- Macro Economics: A Simplified Detailed Edition for Students Understanding Fundamentals of MacroeconomicsОт EverandMacro Economics: A Simplified Detailed Edition for Students Understanding Fundamentals of MacroeconomicsОценок пока нет

- KFC DeliveryДокумент1 страницаKFC DeliveryArthur HoОценок пока нет

- Black Litterman ModelДокумент20 страницBlack Litterman ModelpaufabraОценок пока нет

- Mother Rice Cooker WarrantyДокумент1 страницаMother Rice Cooker WarrantyArthur HoОценок пока нет

- Cointegration Portfolios of European Equities For Index Tracking and Market Neutral StrategiesДокумент21 страницаCointegration Portfolios of European Equities For Index Tracking and Market Neutral StrategiesHenry ChowОценок пока нет

- Merrill Lynch - How To Read A Financial ReportДокумент53 страницыMerrill Lynch - How To Read A Financial Reportstephenspw92% (12)

- Price Indices For Hong Kong Property Market (1999 100)Документ1 страницаPrice Indices For Hong Kong Property Market (1999 100)Arthur HoОценок пока нет

- Cointegration Portfolios of European Equities For Index Tracking and Market Neutral StrategiesДокумент21 страницаCointegration Portfolios of European Equities For Index Tracking and Market Neutral StrategiesHenry ChowОценок пока нет

- March 2009 Home Builder PDFДокумент0 страницMarch 2009 Home Builder PDFArthur HoОценок пока нет

- East America Special and Orlan Do: HighlightsДокумент2 страницыEast America Special and Orlan Do: HighlightsArthur HoОценок пока нет

- Financial Statement AnalysisДокумент2 страницыFinancial Statement AnalysisArthur HoОценок пока нет

- Bond School 2013Документ20 страницBond School 2013Arthur HoОценок пока нет

- PFE PfizerДокумент12 страницPFE PfizerArthur HoОценок пока нет

- Position Sizing 123Документ4 страницыPosition Sizing 123Arthur HoОценок пока нет

- FT 101Документ1 страницаFT 101Arthur HoОценок пока нет

- Nestle 2012 Financial StatementsДокумент118 страницNestle 2012 Financial StatementshemantbaidОценок пока нет

- Risk Management in Future ContractsДокумент4 страницыRisk Management in Future Contractsareesakhtar100% (1)

- GEOGRAPHICAL IDENTIFICATION TO Jamaican Blue Mountain CoffeeДокумент1 страницаGEOGRAPHICAL IDENTIFICATION TO Jamaican Blue Mountain Coffee052 Sachchidanand Singh100% (1)

- ASCC #2 Location of WWF in Conc SlabsДокумент1 страницаASCC #2 Location of WWF in Conc SlabsKen SuОценок пока нет

- Astm E1757 01Документ2 страницыAstm E1757 01Ankit MaharshiОценок пока нет

- All Alerts For 17 Jan - ChartinkДокумент17 страницAll Alerts For 17 Jan - Chartinkkashinath09Оценок пока нет

- Icma.: PakistanДокумент3 страницыIcma.: Pakistangfxexpert36Оценок пока нет

- Accountancy Review: Assignment Lpu Review For Submission After April 30, 2020Документ5 страницAccountancy Review: Assignment Lpu Review For Submission After April 30, 2020jackie delos santosОценок пока нет

- All Sister Concern ProfileДокумент15 страницAll Sister Concern Profileanowar hossainОценок пока нет

- Foreign Currency Derivatives Group 7Документ53 страницыForeign Currency Derivatives Group 7Shean BucayОценок пока нет

- ComparitiveДокумент6 страницComparitivesanath vsОценок пока нет

- World BankДокумент47 страницWorld Bankhung TranОценок пока нет

- Tma Members List South Circle 2022-2023Документ15 страницTma Members List South Circle 2022-2023acube.printerОценок пока нет

- Global Alternating Pressure Mattress Industry 2015 Market Research Report 9dimen PDFДокумент4 страницыGlobal Alternating Pressure Mattress Industry 2015 Market Research Report 9dimen PDFRemi DesouzaОценок пока нет

- Determinants of Interest Rate Spreads Among Licensed Commercial Banks in KenyaДокумент8 страницDeterminants of Interest Rate Spreads Among Licensed Commercial Banks in KenyaViverОценок пока нет

- Benefits and Costs of FDIДокумент4 страницыBenefits and Costs of FDImarriette joy abadОценок пока нет

- List of CasesДокумент17 страницList of CasesANANYAОценок пока нет

- Guest Reservation Form and Details (Bamba)Документ13 страницGuest Reservation Form and Details (Bamba)Angel BambaОценок пока нет

- Tourism in RomaniaДокумент8 страницTourism in RomaniaEdit SpitaОценок пока нет

- Tourism Statistics2019Документ10 страницTourism Statistics2019Atish KissoonОценок пока нет

- Sara Semar - 043647655 - Tugas 3 Bahasa Inggris Niaga ADBI4201Документ3 страницыSara Semar - 043647655 - Tugas 3 Bahasa Inggris Niaga ADBI4201Francesc Richard WengerОценок пока нет

- 61365annualreport Icai 2019 20 EnglishДокумент124 страницы61365annualreport Icai 2019 20 EnglishSãñ DëëpОценок пока нет

- Bank Market PowerДокумент18 страницBank Market PowerWahyutri IndonesiaОценок пока нет

- CACS1 Updates Version 2.3Документ2 страницыCACS1 Updates Version 2.3trishitalalaОценок пока нет

- Analysis of The Economic Survey 2022-23Документ39 страницAnalysis of The Economic Survey 2022-23Umair NeoronОценок пока нет

- 4 5915484905189411272Документ1 страница4 5915484905189411272Henok Fikadu100% (1)

- DoubleBTCGuide23 PDFДокумент92 страницыDoubleBTCGuide23 PDFAbdull KajoОценок пока нет

- The Great Depression NotesДокумент3 страницыThe Great Depression NotesAthena GuzmanОценок пока нет

- MCQS InvestmentДокумент3 страницыMCQS Investmentaashir chОценок пока нет

- The Theory of The Firm: An Overview of The Economic Mainstream, Revised EditionДокумент331 страницаThe Theory of The Firm: An Overview of The Economic Mainstream, Revised EditionPaul WalkerОценок пока нет

- M21 HL Paper 3 IB1 Mark SchemeДокумент8 страницM21 HL Paper 3 IB1 Mark SchemeJane ChangОценок пока нет