Вам также может понравиться

- International Portfolio InvestmentsДокумент39 страницInternational Portfolio InvestmentsAshish SaxenaОценок пока нет

- Lecture SixДокумент10 страницLecture SixSaviusОценок пока нет

- The Capital Asset Pricing Model (CAPM)Документ31 страницаThe Capital Asset Pricing Model (CAPM)Tanmay AbhijeetОценок пока нет

- International Portfolio Investment: Reading: Chapter 15Документ39 страницInternational Portfolio Investment: Reading: Chapter 15Tabish ArrhythmiaОценок пока нет

- Foreign Portfolio Investments: Submitted By: Devika V B Vilson Femi - Pius Ferzana Rehman Gishma Paulson Hasna M AДокумент31 страницаForeign Portfolio Investments: Submitted By: Devika V B Vilson Femi - Pius Ferzana Rehman Gishma Paulson Hasna M AMaria U DavidОценок пока нет

- International Portfolio TheoryДокумент27 страницInternational Portfolio TheoryDaleesha SanyaОценок пока нет

- Unit 5 SAPMДокумент26 страницUnit 5 SAPMMathangi VОценок пока нет

- 4 - Problem - Set FRM - PS PDFДокумент3 страницы4 - Problem - Set FRM - PS PDFValentin IsОценок пока нет

- Modern Portfolio Theory: Session IV & VДокумент30 страницModern Portfolio Theory: Session IV & VAmit Singh RanaОценок пока нет

- Module 2 CAPMДокумент11 страницModule 2 CAPMTanvi DevadigaОценок пока нет

- Answers To Concepts in Review: S R R NДокумент5 страницAnswers To Concepts in Review: S R R NJerine TanОценок пока нет

- International Financial Management PgapteДокумент50 страницInternational Financial Management Pgapterameshmba100% (1)

- MARKOWITZ Portfolio TheoryДокумент32 страницыMARKOWITZ Portfolio TheoryDicky IrawanОценок пока нет

- The Global Cost and Availability of Capital: QuestionsДокумент7 страницThe Global Cost and Availability of Capital: QuestionsluckybellaОценок пока нет

- The Global Cost and Availability of Capital: QuestionsДокумент7 страницThe Global Cost and Availability of Capital: QuestionsluckybellaОценок пока нет

- 03.risk and Return IIIДокумент6 страниц03.risk and Return IIIMaithri Vidana KariyakaranageОценок пока нет

- IFA NAZUWA (69875) Tutorial 2Документ6 страницIFA NAZUWA (69875) Tutorial 2Ifa Nazuwa ZaidilОценок пока нет

- CH 12 Risk, Return and Capital BudgetingДокумент5 страницCH 12 Risk, Return and Capital BudgetingFrancisco Alomia0% (1)

- Fundamentals of Multinational Finance Moffett Stonehill 4th Edition Solutions ManualДокумент7 страницFundamentals of Multinational Finance Moffett Stonehill 4th Edition Solutions ManualMikeOsbornenjoi100% (38)

- f55 ER Ch15 International Portfolio InvestmentsДокумент26 страницf55 ER Ch15 International Portfolio InvestmentsDamodarSinghОценок пока нет

- Portfolio Theory 1Документ65 страницPortfolio Theory 1arsenengimbwaОценок пока нет

- Solution Manual For Principles of Managerial Finance Brief 8th Edition ZutterДокумент35 страницSolution Manual For Principles of Managerial Finance Brief 8th Edition ZutterThomasStoutqpoa100% (40)

- Corporate Finance AssignmentДокумент5 страницCorporate Finance AssignmentInam SwatiОценок пока нет

- Risk AversionДокумент8 страницRisk AversionFreddie Asiedu LarbiОценок пока нет

- Module 6 Introduction To Risk and Return Lecture SlidesДокумент61 страницаModule 6 Introduction To Risk and Return Lecture SlidesZohaib AliОценок пока нет

- And Changes Them According The Risk-Return Profited of The AssetsДокумент7 страницAnd Changes Them According The Risk-Return Profited of The Assetssd5239Оценок пока нет

- Chapter 3Документ16 страницChapter 3Esraa TarekОценок пока нет

- Competitive Advantage in Investing: Building Winning Professional PortfoliosОт EverandCompetitive Advantage in Investing: Building Winning Professional PortfoliosОценок пока нет

- Capital MArket MCQДокумент11 страницCapital MArket MCQSoumit DasОценок пока нет

- Graham3e ppt07Документ31 страницаGraham3e ppt07Lim Yu ChengОценок пока нет

- D - Tutorial 7 (Solutions)Документ10 страницD - Tutorial 7 (Solutions)AlfieОценок пока нет

- Chapter 2Документ61 страницаChapter 2Meseret HailemichaelОценок пока нет

- Inter TradeДокумент15 страницInter Tradesatya_somani_1Оценок пока нет

- Group 4 - Optimal Portfolio SelectionДокумент23 страницыGroup 4 - Optimal Portfolio SelectionCindy permatasariОценок пока нет

- CF Lecture 3 Risk and Return v1Документ44 страницыCF Lecture 3 Risk and Return v1Tâm NhưОценок пока нет

- Chapter 8 - Introduction To Asset Pricing ModelsДокумент53 страницыChapter 8 - Introduction To Asset Pricing Modelsmustafa-memon-7379100% (3)

- Ch6 Risk Aversion and Capital Allocation To Risky AssetsДокумент28 страницCh6 Risk Aversion and Capital Allocation To Risky AssetsAmanda Rizki BagastaОценок пока нет

- Investments Chapter 5Документ11 страницInvestments Chapter 5b00812473Оценок пока нет

- Capital Market Theory-Topic FiveДокумент62 страницыCapital Market Theory-Topic FiveRita NyairoОценок пока нет

- Homework Fin InvestmentДокумент5 страницHomework Fin Investmentdamtuan11012000Оценок пока нет

- Lecture 13Документ31 страницаLecture 13Fazli WadoodОценок пока нет

- 4 MPT and Index ModelsДокумент56 страниц4 MPT and Index ModelssrishtiОценок пока нет

- Investment Analysis and Portfolio ManagementДокумент33 страницыInvestment Analysis and Portfolio ManagementUqaila Mirza0% (1)

- Session 5Документ17 страницSession 5maha khanОценок пока нет

- 0522 Capital Allocation UNIT 5Документ69 страниц0522 Capital Allocation UNIT 5fadiismaОценок пока нет

- Portfolio Management 1Документ28 страницPortfolio Management 1Sattar Md AbdusОценок пока нет

- CapmДокумент51 страницаCapmlathachilОценок пока нет

- Portfolio Managemet InternalДокумент6 страницPortfolio Managemet Internalasutoshpradhan36Оценок пока нет

- Volatility Modelling: Next ChapterДокумент33 страницыVolatility Modelling: Next ChapterMujeeb Ul Rahman MrkhosoОценок пока нет

- Investment Analysis and Portfolio Management: Lecture Presentation SoftwareДокумент77 страницInvestment Analysis and Portfolio Management: Lecture Presentation SoftwarekhandakeralihossainОценок пока нет

- Chapter 1 FMДокумент47 страницChapter 1 FMabdellaОценок пока нет

- Capital Asset Pricing ModelДокумент18 страницCapital Asset Pricing ModelSonalir RaghuvanshiОценок пока нет

- Sapm Unit 4Документ33 страницыSapm Unit 4Vi Pin SinghОценок пока нет

- Chapter 9 Faculty WebsitesДокумент19 страницChapter 9 Faculty WebsitesStudy PinkОценок пока нет

- Chapter 15 SAQДокумент3 страницыChapter 15 SAQLouise AngelouОценок пока нет

- Topic 5Документ5 страницTopic 5黄芷琦Оценок пока нет

- 7 - Riks and LeverageДокумент36 страниц7 - Riks and LeveragePagatpat, Apple Grace C.Оценок пока нет

- AFC3240 Topic 09 S1 2011Документ17 страницAFC3240 Topic 09 S1 2011sittmoОценок пока нет

- AFC3240 Topic 07 S1 2011Документ12 страницAFC3240 Topic 07 S1 2011sittmoОценок пока нет

- AFC3240 Topic 03 S1 2011Документ36 страницAFC3240 Topic 03 S1 2011sittmoОценок пока нет

- International Parity Relationship: Topic 4Документ32 страницыInternational Parity Relationship: Topic 4sittmoОценок пока нет

- AFC3240 NotesДокумент18 страницAFC3240 NotessittmoОценок пока нет

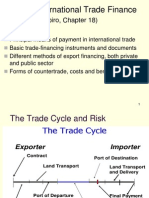

- Topic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)Документ15 страницTopic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)sittmoОценок пока нет

- AFC3240 Topic 01 S2 2010Документ18 страницAFC3240 Topic 01 S2 2010sittmoОценок пока нет

- AFC3240 Topic 06 S1 2011Документ27 страницAFC3240 Topic 06 S1 2011sittmoОценок пока нет

- Sec 03Документ24 страницыSec 03sittmoОценок пока нет

- Topic Determination of Exchange Rate: Balance of Payments (BOP)Документ27 страницTopic Determination of Exchange Rate: Balance of Payments (BOP)sittmoОценок пока нет

- Sec 01Документ35 страницSec 01sittmoОценок пока нет

- Solving Inhomogenous Recurrence Relations 2Документ2 страницыSolving Inhomogenous Recurrence Relations 2sittmoОценок пока нет

- Section 2 Section 2 Intervention in Markets Intervention in MarketsДокумент18 страницSection 2 Section 2 Intervention in Markets Intervention in MarketssittmoОценок пока нет

- Solving Inhomogenous Recurrence Relations 3Документ4 страницыSolving Inhomogenous Recurrence Relations 3sittmoОценок пока нет

- Sec 04Документ32 страницыSec 04sittmoОценок пока нет

- Solving Inhomogenous Recurrence RelationsДокумент3 страницыSolving Inhomogenous Recurrence Relationssittmo0% (1)

- Lesson Plan 9th Grade ScienceДокумент2 страницыLesson Plan 9th Grade Scienceapi-316973807Оценок пока нет

- Safety Competency TrainingДокумент21 страницаSafety Competency TrainingsemajamesОценок пока нет

- Take The MMPI Test Online For Free: Hypnosis Articles and InformationДокумент14 страницTake The MMPI Test Online For Free: Hypnosis Articles and InformationUMINAH0% (1)

- Indian Entrepreneur Fund PresentationДокумент44 страницыIndian Entrepreneur Fund PresentationHARIHARAN AОценок пока нет

- Art Analysis Ap EuroДокумент5 страницArt Analysis Ap Euroapi-269743889Оценок пока нет

- Quiz 4Документ5 страницQuiz 4Diegiitho Acevedo MartiinezОценок пока нет

- KWPL07 RankinДокумент28 страницKWPL07 RankinBoogy GrimОценок пока нет

- Cost Study On SHEET-FED PRESS OPERATIONSДокумент525 страницCost Study On SHEET-FED PRESS OPERATIONSalexbilchuk100% (1)

- SWOC AnalysisДокумент5 страницSWOC AnalysisSyakirah HeartnetОценок пока нет

- Additive ManufactДокумент61 страницаAdditive ManufactAnca Maria TruscaОценок пока нет

- Public Procurement Rules 2004Документ35 страницPublic Procurement Rules 2004Mubashir SheheryarОценок пока нет

- International Business of Pizza HutДокумент13 страницInternational Business of Pizza Hutpratikdotia9100% (2)

- Ageing Baby BoomersДокумент118 страницAgeing Baby Boomersstephloh100% (1)

- 2 BA British and American Life and InstitutionsДокумент3 страницы2 BA British and American Life and Institutionsguest1957Оценок пока нет

- Let ReviewДокумент9 страницLet ReviewBaesittieeleanor MamualasОценок пока нет

- Flowers For The Devil - A Dark V - Vlad KahanyДокумент435 страницFlowers For The Devil - A Dark V - Vlad KahanyFizzah Sardar100% (6)

- Complaint - California Brewing v. 3 Daughters BreweryДокумент82 страницыComplaint - California Brewing v. 3 Daughters BreweryDarius C. GambinoОценок пока нет

- Environmental Education Strategy (2010-2014) : United Republic of TanzaniaДокумент63 страницыEnvironmental Education Strategy (2010-2014) : United Republic of Tanzaniaalli sheeranОценок пока нет

- A Will Eternal - Book 1Документ1 295 страницA Will Eternal - Book 1Hitsuin Movies100% (1)

- Atlas of Pollen and Spores and Their Parent Taxa of MT Kilimanjaro and Tropical East AfricaДокумент86 страницAtlas of Pollen and Spores and Their Parent Taxa of MT Kilimanjaro and Tropical East AfricaEdilson Silva100% (1)

- Excuse Letter For Grade 7 ElectionsДокумент4 страницыExcuse Letter For Grade 7 ElectionsRaymund ArcosОценок пока нет

- Java Programming - Module2021Документ10 страницJava Programming - Module2021steven hernandezОценок пока нет

- Daftar PustakaДокумент2 страницыDaftar PustakaBang UsopОценок пока нет

- Bell Atlantic Corp v. TwomblyДокумент4 страницыBell Atlantic Corp v. Twomblylfei1216Оценок пока нет

- Teaching The GospelДокумент50 страницTeaching The GospelgabrielpoulsonОценок пока нет

- 750-366 Hawk 1000 07 13 PDFДокумент82 страницы750-366 Hawk 1000 07 13 PDFAlexis CruzОценок пока нет

- Fritz Perls in Berlin 1893 1933 ExpressiДокумент11 страницFritz Perls in Berlin 1893 1933 ExpressiLeonardo Leite0% (1)

- BHCS31352F Mentor ViQ Specsheet - R24Документ8 страницBHCS31352F Mentor ViQ Specsheet - R24Jocélio A. TavaresОценок пока нет

- Global Value Chain: Shikha GuptaДокумент19 страницGlobal Value Chain: Shikha GuptaRushilОценок пока нет

- APPELANTДокумент30 страницAPPELANTTAS MUNОценок пока нет