Вам также может понравиться

- SRC: Exempt Securities, Exempt Transactions, and Mandatory Tender OfferДокумент7 страницSRC: Exempt Securities, Exempt Transactions, and Mandatory Tender OfferDeus DulayОценок пока нет

- Securities Regulation CodeДокумент75 страницSecurities Regulation CodeTan Mark AndrewОценок пока нет

- Notes On SECURITIES REGULATION CODEДокумент18 страницNotes On SECURITIES REGULATION CODEcharmagne cuevasОценок пока нет

- SEC Regulation Code Protects InvestorsДокумент7 страницSEC Regulation Code Protects InvestorsRj ArevadoОценок пока нет

- REVISED SECURITIES ACT REVIEWERДокумент11 страницREVISED SECURITIES ACT REVIEWERJunyvil TumbagaОценок пока нет

- Securities Regulation CodeДокумент8 страницSecurities Regulation CodeOscar Ryan SantillanОценок пока нет

- RA 8799 Securities and Regulation CodeДокумент24 страницыRA 8799 Securities and Regulation CodeShalom May Catedrilla0% (1)

- Securities Regulation Code CA51025 PDFДокумент31 страницаSecurities Regulation Code CA51025 PDFKiana FernandezОценок пока нет

- Securities Regulation Code ReviewerДокумент12 страницSecurities Regulation Code ReviewerJose LacasОценок пока нет

- Meetings, Stocks and Stockholders, Corporate Books and Records Under The Civil Code of The PhilippinesДокумент73 страницыMeetings, Stocks and Stockholders, Corporate Books and Records Under The Civil Code of The PhilippinesMimi VargasОценок пока нет

- The Securities and Regulation CodeДокумент11 страницThe Securities and Regulation CodeCacapablen GinОценок пока нет

- Banking and SPCL Divina NotesДокумент27 страницBanking and SPCL Divina NotesPrincess Janine SyОценок пока нет

- Foreign Investments ReviewerДокумент13 страницForeign Investments ReviewerRichard Alpert Bautista100% (3)

- SECURITIES REGULATION CODE (My Own ReviewerДокумент18 страницSECURITIES REGULATION CODE (My Own ReviewerMaritesCatayong100% (5)

- Securities Regulations CodeДокумент13 страницSecurities Regulations CodeYumi kosha50% (2)

- Pactum Commissorium Can Be Found in Article 2088 of The Civil Code Which ProvidesДокумент1 страницаPactum Commissorium Can Be Found in Article 2088 of The Civil Code Which ProvidesKryzzle Martin BoriОценок пока нет

- New Central Bank ActДокумент17 страницNew Central Bank ActKamil Ubungen Delos ReyesОценок пока нет

- Module 1-SRCДокумент67 страницModule 1-SRCAleah Jehan AbuatОценок пока нет

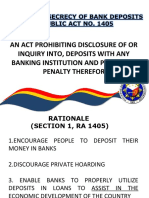

- The Law On Secrecy of Bank DepositsДокумент17 страницThe Law On Secrecy of Bank DepositsMakoy BixenmanОценок пока нет

- AOI SampleДокумент4 страницыAOI SampleBona Carmela BienОценок пока нет

- Truth in Lending ActДокумент12 страницTruth in Lending ActCoreine Imee ValledorОценок пока нет

- 39 Carpo v. ChuaДокумент2 страницы39 Carpo v. ChuaAngelette BulacanОценок пока нет

- Securities Regulation Code NotesДокумент99 страницSecurities Regulation Code NotesLRBОценок пока нет

- Commercial and Investment Bank OperationsДокумент51 страницаCommercial and Investment Bank OperationsjasonОценок пока нет

- Credit Deposit GuarantyДокумент6 страницCredit Deposit GuarantyJohn Lester LantinОценок пока нет

- Derivative SuitДокумент1 страницаDerivative SuitShannon Patricia SepianОценок пока нет

- PDIC Illustrative ProblemsДокумент5 страницPDIC Illustrative ProblemsDiscord HowОценок пока нет

- Corporate Doctrines ExplainedДокумент1 страницаCorporate Doctrines ExplainedAllan PatulotОценок пока нет

- Jurisdiction of Various Philippine CourtsДокумент11 страницJurisdiction of Various Philippine CourtsSHEKINAHFAITH REQUINTEL100% (1)

- Corporation - Reviewer MidtermДокумент9 страницCorporation - Reviewer MidtermJofrank David RiegoОценок пока нет

- Doctrine of Apparent AuthorityДокумент4 страницыDoctrine of Apparent Authorityonlineonrandomdays100% (1)

- Secrecy of Bank DepositsДокумент9 страницSecrecy of Bank DepositsMADEE VILLANUEVAОценок пока нет

- Law on Public Officers 1st Term Prof. Antonio P. Jamon JrДокумент8 страницLaw on Public Officers 1st Term Prof. Antonio P. Jamon JrChedeng KumaОценок пока нет

- New Central Bank ActДокумент39 страницNew Central Bank ActdollyccruzОценок пока нет

- Midterm WWW Compiled 2016 - Atty. EspedidoДокумент50 страницMidterm WWW Compiled 2016 - Atty. EspedidoD.F. de Lira100% (1)

- SECURITIES REGULATION CODEДокумент15 страницSECURITIES REGULATION CODEJett LabillesОценок пока нет

- Duties and Rights of AgentДокумент2 страницыDuties and Rights of AgentnishmaОценок пока нет

- TITLE XV Foreign Corporation SEC 140-153Документ16 страницTITLE XV Foreign Corporation SEC 140-153Chenna Mae ReyesОценок пока нет

- FRIA Class NotesДокумент14 страницFRIA Class NotesAnonymous wDganZОценок пока нет

- Ra 3591 - PdicДокумент7 страницRa 3591 - PdicIzobelle Pulgo100% (2)

- Foreign Corporations.: NotesДокумент16 страницForeign Corporations.: NotesvivivioletteОценок пока нет

- Republic Act No. 8792 "Electronic Commerce Act of 2000"Документ4 страницыRepublic Act No. 8792 "Electronic Commerce Act of 2000"E.D.JОценок пока нет

- Oblicon 1-5Документ17 страницOblicon 1-5Vanessa Evans CruzОценок пока нет

- SEC 29 VACANCIES IN THE OFFICE OF DIRECTOR OR TRUSTEEДокумент5 страницSEC 29 VACANCIES IN THE OFFICE OF DIRECTOR OR TRUSTEEWendell Leigh OasanОценок пока нет

- Partnership, Agency and Trust DefinitionДокумент27 страницPartnership, Agency and Trust DefinitionJairus LacabaОценок пока нет

- Persons and Family RelationДокумент2 страницыPersons and Family RelationJannyn RuanoОценок пока нет

- Jurists Lecture (Securities Regulation Code)Документ16 страницJurists Lecture (Securities Regulation Code)Lee Anne Yabut100% (1)

- General Banking LawДокумент25 страницGeneral Banking LawKristina AculladorОценок пока нет

- LOSS OF THING AND DEBT EXTINGUISHMENTДокумент61 страницаLOSS OF THING AND DEBT EXTINGUISHMENT.Оценок пока нет

- Court Observations Provide Insight Into Judicial SystemДокумент2 страницыCourt Observations Provide Insight Into Judicial SystemKarl Rigo AndrinoОценок пока нет

- Taxation and Due Process Under the Philippine ConstitutionДокумент15 страницTaxation and Due Process Under the Philippine Constitutionkimberly milagОценок пока нет

- Divina Notes On Revised Corporation CodeДокумент11 страницDivina Notes On Revised Corporation CodeGenevieve PenetranteОценок пока нет

- AMENDED IRR-RA 8799 - Amended Implementing Rules and Regulations of The Securities Regulation CodeДокумент139 страницAMENDED IRR-RA 8799 - Amended Implementing Rules and Regulations of The Securities Regulation CodeJane Catherine Rojo TiuОценок пока нет

- Reviewer General Banking LawДокумент15 страницReviewer General Banking LawThethan ArenaОценок пока нет

- BANK SECRECY LAW AND SAFETY DEPOSIT BOX DISPUTESДокумент7 страницBANK SECRECY LAW AND SAFETY DEPOSIT BOX DISPUTESArbee ArquizaОценок пока нет

- Torts and Damages 1Документ14 страницTorts and Damages 1pyrl divinagraciaОценок пока нет

- RFLB Reviewer (Module 3)Документ8 страницRFLB Reviewer (Module 3)Monica's iPadОценок пока нет

- Securities and Exchange Commission FunctionsДокумент5 страницSecurities and Exchange Commission FunctionsJeshiel Mae GeneralaoОценок пока нет

- Securities Regulation Code of The Philippines (R.A. 8799) PurposeДокумент11 страницSecurities Regulation Code of The Philippines (R.A. 8799) PurposeWilmar AbriolОценок пока нет

- The Securities and Exchange CommissionДокумент8 страницThe Securities and Exchange CommissionChristine CaridoОценок пока нет

- Waiver of Rights - SampleДокумент1 страницаWaiver of Rights - SampleAiken Alagban LadinesОценок пока нет

- ST Kiss The Miss Goodbye 8x10 1Документ1 страницаST Kiss The Miss Goodbye 8x10 1Aiken Alagban LadinesОценок пока нет

- Abstract of Tomato PlantationДокумент1 страницаAbstract of Tomato PlantationAiken Alagban LadinesОценок пока нет

- ClubsДокумент1 страницаClubsAiken Alagban LadinesОценок пока нет

- Christmas CardsДокумент1 страницаChristmas CardsAiken Alagban LadinesОценок пока нет

- Affidavit of LossДокумент1 страницаAffidavit of LossAiken Alagban LadinesОценок пока нет

- Cases - SourcesДокумент15 страницCases - SourcesAiken Alagban LadinesОценок пока нет

- SPA SampleДокумент2 страницыSPA SampleAiken Alagban LadinesОценок пока нет

- Entry of Appearance: (As Collaborating Counsel)Документ2 страницыEntry of Appearance: (As Collaborating Counsel)Aiken Alagban LadinesОценок пока нет

- Judicial Affidavit - SampleДокумент7 страницJudicial Affidavit - SampleAiken Alagban LadinesОценок пока нет

- Joint Affidavit of Discrepancy SampleДокумент1 страницаJoint Affidavit of Discrepancy SampleAiken Alagban Ladines100% (5)

- Materials UsedДокумент3 страницыMaterials UsedAiken Alagban LadinesОценок пока нет

- Joint affidavit clarifying true name of Ser John TumpagДокумент1 страницаJoint affidavit clarifying true name of Ser John TumpagAiken Alagban LadinesОценок пока нет

- Effective Communication As A Means To Global PeacДокумент2 страницыEffective Communication As A Means To Global PeacAiken Alagban Ladines100% (1)

- Compassion in Action - EditedДокумент1 страницаCompassion in Action - EditedAiken Alagban LadinesОценок пока нет

- Registered VotersДокумент1 страницаRegistered VotersAiken Alagban LadinesОценок пока нет

- Celebrating His Love - EditedДокумент1 страницаCelebrating His Love - EditedAiken Alagban LadinesОценок пока нет

- Affidavit of LossДокумент1 страницаAffidavit of LossAiken Alagban LadinesОценок пока нет

- Protect Children from Colds & Flu with VaccinesДокумент1 страницаProtect Children from Colds & Flu with VaccinesAiken Alagban LadinesОценок пока нет

- Answer - Reswri 2Документ6 страницAnswer - Reswri 2Aiken Alagban LadinesОценок пока нет

- Daily RemindersДокумент4 страницыDaily RemindersAiken Alagban LadinesОценок пока нет

- LTFRB Revised Rules of Practice and ProcedureДокумент25 страницLTFRB Revised Rules of Practice and ProcedureSJ San Juan100% (2)

- Revised Rules On Administrative Cases in The Civil ServiceДокумент43 страницыRevised Rules On Administrative Cases in The Civil ServiceMerlie Moga100% (29)

- Bar SchedДокумент1 страницаBar SchedAiken Alagban LadinesОценок пока нет

- Colds/Flu Prevention Through VaccinationДокумент1 страницаColds/Flu Prevention Through VaccinationAiken Alagban LadinesОценок пока нет

- Tax NotesДокумент6 страницTax NotesAiken Alagban LadinesОценок пока нет

- Galatians 5 Living by The Spirit's PowerДокумент1 страницаGalatians 5 Living by The Spirit's PowerAiken Alagban LadinesОценок пока нет

- Get Your First Passport: Requirements for New ApplicantsДокумент2 страницыGet Your First Passport: Requirements for New ApplicantsAiken Alagban LadinesОценок пока нет

- Resolution To Open Bank AccountsДокумент1 страницаResolution To Open Bank AccountsAiken Alagban LadinesОценок пока нет

- Code of Professional ResponsibilityДокумент3 страницыCode of Professional ResponsibilityAiken Alagban LadinesОценок пока нет

- Auditing and Assurance AssignmentДокумент18 страницAuditing and Assurance AssignmentJiya and Riddhi DugarОценок пока нет

- Corporate Case Analysis - BHAVNAДокумент9 страницCorporate Case Analysis - BHAVNAMunniBhavnaОценок пока нет

- Company Law Final 2012Документ9 страницCompany Law Final 2012Nosheen MalikОценок пока нет

- Automotive Industry: Code of Conduct Drugs and AlcoholДокумент9 страницAutomotive Industry: Code of Conduct Drugs and AlcoholHARSHIT KUMAR GUPTA 1923334Оценок пока нет

- CH 10 Financial Market (Case Studies) - NewДокумент6 страницCH 10 Financial Market (Case Studies) - NewPavithra AnupОценок пока нет

- Keown Perfin5 Im 12Документ13 страницKeown Perfin5 Im 12a_hslrОценок пока нет

- Vineet Sharma SIPДокумент40 страницVineet Sharma SIPSushant KumarОценок пока нет

- 2015 SRC Rules Table of ContentsДокумент13 страниц2015 SRC Rules Table of ContentsErika delos SantosОценок пока нет

- Telstra Business PrinciplesДокумент24 страницыTelstra Business PrinciplesTong WanОценок пока нет

- Letter About Carl IcahnДокумент4 страницыLetter About Carl IcahnCNBC.com100% (1)

- Regulatory Framework For Investors ProtectionДокумент32 страницыRegulatory Framework For Investors Protectionharsh sahuОценок пока нет

- Nism 3 A - Compliance - Last Day Revision Test 1Документ39 страницNism 3 A - Compliance - Last Day Revision Test 1Rohit Sharma50% (2)

- Corporate Formation and OrganizationДокумент18 страницCorporate Formation and OrganizationBernardine Andrew BeringОценок пока нет

- Motion to Dismiss Insider Trading ChargesДокумент84 страницыMotion to Dismiss Insider Trading Chargesbpk2001Оценок пока нет

- A Legal Perspective On Technology and The Capital Markets - Joshua MittsДокумент50 страницA Legal Perspective On Technology and The Capital Markets - Joshua MittsJuan Eduardo Gómez LondoñoОценок пока нет

- To Catch A Trader AnalysisДокумент1 страницаTo Catch A Trader AnalysisAlokОценок пока нет

- SWOT Analysis of Capital MarketДокумент6 страницSWOT Analysis of Capital Marketpassionmarket75% (4)

- Revision Kit CASE STUDY AnswersДокумент13 страницRevision Kit CASE STUDY AnswersmeeteshlalОценок пока нет

- Corporations OutlineДокумент4 страницыCorporations OutlineKeith DyerОценок пока нет

- Admin Law Week 5 DigestsДокумент22 страницыAdmin Law Week 5 DigestsAnn Mutya MapanoОценок пока нет

- 2016 Bravery Tips - Commercial Law PDFДокумент16 страниц2016 Bravery Tips - Commercial Law PDFKristal LeeОценок пока нет

- Wipro Project Engineer AppointmentДокумент18 страницWipro Project Engineer AppointmentShivam DwivediОценок пока нет

- National Stock of IndiaДокумент18 страницNational Stock of IndiaVipin KapoorОценок пока нет

- 4 - Ethics - IBBIДокумент16 страниц4 - Ethics - IBBIRajwinder Singh BansalОценок пока нет

- 4 Project - Report CoscoДокумент99 страниц4 Project - Report Coscojavs152567% (3)

- Eileen Segall of Tildenrow Partners: Long On ReachLocalДокумент0 страницEileen Segall of Tildenrow Partners: Long On ReachLocalcurrygoatОценок пока нет

- Airtel Code of EthicsДокумент13 страницAirtel Code of Ethicsyuvraj216Оценок пока нет

- RFLB Reviewer (Module 3)Документ8 страницRFLB Reviewer (Module 3)Monica's iPadОценок пока нет

- Witness List For Rajat K. Gupta TrialДокумент15 страницWitness List For Rajat K. Gupta TrialDealBookОценок пока нет

- A Study On Marketing Mix at HeritageДокумент75 страницA Study On Marketing Mix at HeritageNagireddy Kalluri50% (2)