Вам также может понравиться

- Metbio Trainingdoc Sama541633 28-06-2010Документ29 страницMetbio Trainingdoc Sama541633 28-06-2010Prerna GuptaОценок пока нет

- Poor Track Record of Shareholder Protection in IndiaДокумент20 страницPoor Track Record of Shareholder Protection in IndiaPrerna GuptaОценок пока нет

- L.L.M/M.L. Degree Examination May 2014: (Branch I: Contracts Including Merchantile Law)Документ2 страницыL.L.M/M.L. Degree Examination May 2014: (Branch I: Contracts Including Merchantile Law)Prerna GuptaОценок пока нет

- Private: Minority ShareholdersДокумент4 страницыPrivate: Minority ShareholdersPrerna GuptaОценок пока нет

- CRPCДокумент17 страницCRPCPrerna Gupta100% (1)

- Amity Business School Bba-Ll.B: Sem-VIДокумент4 страницыAmity Business School Bba-Ll.B: Sem-VIPrerna GuptaОценок пока нет

- Steps in OD: Name of InstitutionДокумент3 страницыSteps in OD: Name of InstitutionPrerna GuptaОценок пока нет

- Poor Track Record of ShareholdersДокумент8 страницPoor Track Record of ShareholdersPrerna GuptaОценок пока нет

- Adoption of Child in India With Special Reference To HindusДокумент18 страницAdoption of Child in India With Special Reference To HindusPrerna GuptaОценок пока нет

- Company Law ProjectДокумент23 страницыCompany Law ProjectPrerna Gupta100% (1)

- MemorialДокумент30 страницMemorialPrerna GuptaОценок пока нет

- Restriction On Transfer of SharesДокумент20 страницRestriction On Transfer of SharesPrerna GuptaОценок пока нет

- 5 Year PlanДокумент32 страницы5 Year PlanPrerna GuptaОценок пока нет

- Indian Business EnvironmentДокумент18 страницIndian Business EnvironmentPrerna GuptaОценок пока нет

- Eggless Strawberry Cream CakeДокумент2 страницыEggless Strawberry Cream CakePrerna GuptaОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- International Marketing Asia Pacific 3rd Edition Czinkota Test BankДокумент11 страницInternational Marketing Asia Pacific 3rd Edition Czinkota Test BankMichaelRothpdytk100% (13)

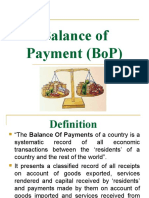

- Mbf14e Chap03 Bop PbmsДокумент10 страницMbf14e Chap03 Bop PbmsPablo MelchorОценок пока нет

- Final Exam On Different Economic Strategies Between France and TürkiyeДокумент2 страницыFinal Exam On Different Economic Strategies Between France and Türkiyecenkay.uyanОценок пока нет

- Accounting Concept of Currency Chest TransactionДокумент1 страницаAccounting Concept of Currency Chest TransactionAjoydeep DasОценок пока нет

- Ansi ListДокумент293 страницыAnsi ListMeggy Villanueva67% (6)

- Economic GeographyДокумент6 страницEconomic GeographyAdjepoleОценок пока нет

- Socio 101 Lesson 2Документ13 страницSocio 101 Lesson 2Hans Kimberly V. DavidОценок пока нет

- World Montary System, 1972Документ52 страницыWorld Montary System, 1972Can UludağОценок пока нет

- Torq Aifta 070 IssuedДокумент11 страницTorq Aifta 070 IssuedSuraj KapseОценок пока нет

- ETOДокумент26 страницETOabcОценок пока нет

- Foreign Exchange MarketДокумент14 страницForeign Exchange MarketCarmela Anne SampianoОценок пока нет

- International Monetary SystemsДокумент27 страницInternational Monetary SystemsArun ChhikaraОценок пока нет

- Hindering Trade DiversionДокумент4 страницыHindering Trade DiversionAnne S. YenОценок пока нет

- SOC101 ReportДокумент20 страницSOC101 ReportLorimae NicolasОценок пока нет

- SADC Trade GuideДокумент44 страницыSADC Trade GuideSoundMan56100% (1)

- Incoterms 2010: Fca Usa Airport Fca Aircraft CPT Foreign Airport CIP Foreign AirportДокумент1 страницаIncoterms 2010: Fca Usa Airport Fca Aircraft CPT Foreign Airport CIP Foreign AirportAdhyartha KerafОценок пока нет

- World Trade Organization: CriticismДокумент44 страницыWorld Trade Organization: Criticismrain06021992Оценок пока нет

- S10 107 TWNДокумент3 страницыS10 107 TWNJinko JankoОценок пока нет

- Chapter 1Документ20 страницChapter 1Jubayer 3DОценок пока нет

- Bricks and Mortar in A Borderless World: Globalization, The Backlash, and The Multinational EnterpriseДокумент3 страницыBricks and Mortar in A Borderless World: Globalization, The Backlash, and The Multinational EnterpriseMohd Shahbaz HusainОценок пока нет

- Sales OrderДокумент320 страницSales OrderKOTARI PURNACHANDRARAOОценок пока нет

- International Flow of FundsДокумент31 страницаInternational Flow of FundsNetflix 0001Оценок пока нет

- SBI - Post Merger List of OLD and NEW BIC For Erstwhile Associate BanksДокумент8 страницSBI - Post Merger List of OLD and NEW BIC For Erstwhile Associate BanksTamil GoodReturnsОценок пока нет

- Questions and Answers For Macroeconomy On Wed. 23.3 The Open EconomyДокумент9 страницQuestions and Answers For Macroeconomy On Wed. 23.3 The Open EconomymarcjeansОценок пока нет

- Unit 1 Balance of PaymentДокумент32 страницыUnit 1 Balance of PaymentAnusha kanmaniОценок пока нет

- IMF Special Drawing RightsДокумент3 страницыIMF Special Drawing RightsJialu LiuОценок пока нет

- Madura IFM10e TB Ch02-1Документ4 страницыMadura IFM10e TB Ch02-1Le Ngoc HienОценок пока нет

- ECO372 Week 5 International Trade and FiananceДокумент6 страницECO372 Week 5 International Trade and FiananceWellThisIsDifferentОценок пока нет

- ECON 3023 CH 13Документ22 страницыECON 3023 CH 13Rafina AzizОценок пока нет

- MGT 445 - Chapter 1 - NotesДокумент9 страницMGT 445 - Chapter 1 - NotesKatie WilliamsОценок пока нет