Вам также может понравиться

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)От EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Рейтинг: 3.5 из 5 звезд3.5/5 (17)

- Financial Planning and ForecastingДокумент25 страницFinancial Planning and ForecastingAhsan100% (2)

- Financial Planning and ForecastingДокумент24 страницыFinancial Planning and ForecastingMikee Ballesteros ManzanoОценок пока нет

- Chapter 17 - Financial Planning & ForecastingДокумент20 страницChapter 17 - Financial Planning & ForecastingammoiОценок пока нет

- Financial Planning and ForecastingДокумент35 страницFinancial Planning and Forecastingphyu sweОценок пока нет

- Financial Planning and Forecasting: Pro Forma Financial StatementsДокумент8 страницFinancial Planning and Forecasting: Pro Forma Financial StatementsLevi Lazareno EugenioОценок пока нет

- AFNДокумент34 страницыAFNJeffreyNaguimbing100% (1)

- Financial Management - I: Financial Planning and Forecasting Financial StatementsДокумент28 страницFinancial Management - I: Financial Planning and Forecasting Financial StatementsOnal RautОценок пока нет

- Lecture 6 AFN Equation 26102020 063217pmДокумент14 страницLecture 6 AFN Equation 26102020 063217pmomar hashmiОценок пока нет

- Financial PlanningДокумент28 страницFinancial Planningdabigshow85Оценок пока нет

- ch02 Financial Statement, Cash Flows and TaxesДокумент30 страницch02 Financial Statement, Cash Flows and TaxesAffan AhmedОценок пока нет

- 17Документ4 страницы17Serene Nicole Villena75% (4)

- Illustration On AFN (FE 12)Документ39 страницIllustration On AFN (FE 12)Jessica Adharana KurniaОценок пока нет

- Financial Planning and Forecasting Financial Statements: Answers To End-Of-Chapter QuestionsДокумент9 страницFinancial Planning and Forecasting Financial Statements: Answers To End-Of-Chapter QuestionsArpit BhawsarОценок пока нет

- TM 10 - Financial Planning and ForecastingДокумент29 страницTM 10 - Financial Planning and ForecastingTul KuntullОценок пока нет

- AC517Документ11 страницAC517Inaia ScottОценок пока нет

- 14Документ9 страниц14Rudine Pak MulОценок пока нет

- Long-Term Financial Planning: Plans: Strategic, Operating, and Financial Pro Forma Financial StatementsДокумент50 страницLong-Term Financial Planning: Plans: Strategic, Operating, and Financial Pro Forma Financial StatementsSyed MohdОценок пока нет

- Financial Planning and ForecastingДокумент15 страницFinancial Planning and ForecastingHery PrambudiОценок пока нет

- 2.0 FIN Plan & Forecasting v1Документ62 страницы2.0 FIN Plan & Forecasting v1Omer CrestianiОценок пока нет

- AFNpostДокумент27 страницAFNpostRoyalyn LaureanoОценок пока нет

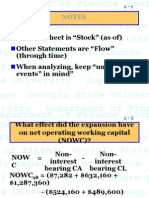

- Balance Sheet Is "Stock" (As Of) Other Statements Are "Flow" (Through Time) When Analyzing, Keep "Unusual Events" in Mind"Документ22 страницыBalance Sheet Is "Stock" (As Of) Other Statements Are "Flow" (Through Time) When Analyzing, Keep "Unusual Events" in Mind"kegnataОценок пока нет

- Solutions Nss NC 17Документ13 страницSolutions Nss NC 17lethiphuongdan50% (2)

- Investment VI FINC 404 Company ValuationДокумент52 страницыInvestment VI FINC 404 Company ValuationMohamed MadyОценок пока нет

- Financial Statements, Cash Flow, and TaxesДокумент30 страницFinancial Statements, Cash Flow, and TaxesSumitMadnaniОценок пока нет

- CH 02Документ30 страницCH 02AhsanОценок пока нет

- Financial Forecasting SamarakoonДокумент33 страницыFinancial Forecasting SamarakoonEyael ShimleasОценок пока нет

- Problems 1st PartДокумент17 страницProblems 1st PartValentin JallaisОценок пока нет

- Financial Statements, Cash Flow, and TaxesДокумент29 страницFinancial Statements, Cash Flow, and TaxesHooriaKhanОценок пока нет

- Tugas Kelompok 1Документ6 страницTugas Kelompok 1Bought By UsОценок пока нет

- FM12 CH 14 Mini CaseДокумент7 страницFM12 CH 14 Mini CaseYousry El-FoweyОценок пока нет

- Excercice 7.3 CorrectДокумент5 страницExcercice 7.3 CorrectKimberlyGayborОценок пока нет

- Exercise 3. Cash Flows Statements and WorkingДокумент8 страницExercise 3. Cash Flows Statements and WorkingQuang Dũng NguyễnОценок пока нет

- 17 Answers To All ProblemsДокумент25 страниц17 Answers To All ProblemsRaşitÖnerОценок пока нет

- 17 Answers To All ProblemsДокумент25 страниц17 Answers To All ProblemsAarti J100% (1)

- 17 Answers To All ProblemsДокумент25 страниц17 Answers To All ProblemsRaşitÖnerОценок пока нет

- Shahnai - 2279 - 4080 - 1 - Chap 2 Financial Planning & ForecastingДокумент48 страницShahnai - 2279 - 4080 - 1 - Chap 2 Financial Planning & ForecastingShahzad C7Оценок пока нет

- Solutions To End-Of-Chapter ProblemsДокумент22 страницыSolutions To End-Of-Chapter ProblemsKalyani GogoiОценок пока нет

- Financial Planning and Forecasting Pro Forma Financial StatementsДокумент22 страницыFinancial Planning and Forecasting Pro Forma Financial StatementsCOLONEL ZIKRIA0% (1)

- Cruz Janna Kassandra Midterm Practice ProblemsДокумент6 страницCruz Janna Kassandra Midterm Practice ProblemsMiguel PultaОценок пока нет

- Financial Planning and Forecasting Financial Statements: Answers To End-Of-Chapter QuestionsДокумент10 страницFinancial Planning and Forecasting Financial Statements: Answers To End-Of-Chapter QuestionsBilal RazzaqОценок пока нет

- Financial Planning and Forecasting - Solved Q&AДокумент6 страницFinancial Planning and Forecasting - Solved Q&ARex CalibreОценок пока нет

- Chapter 03Документ29 страницChapter 03andi.w.rahardjoОценок пока нет

- Financial Planning and Forecasting Financial StatementsДокумент46 страницFinancial Planning and Forecasting Financial StatementsRimpy SondhОценок пока нет

- Concepts Review and Critical Thinking Questions 4Документ6 страницConcepts Review and Critical Thinking Questions 4fnrbhcОценок пока нет

- Financial Planning and ForecastingДокумент22 страницыFinancial Planning and ForecastingArif SharifОценок пока нет

- EFM2e, CH 04, SlidesДокумент16 страницEFM2e, CH 04, SlidesMaria DevinaОценок пока нет

- Finders Valves and Controls Inc.Документ4 страницыFinders Valves and Controls Inc.raulzaragoza0422100% (1)

- Case Study - Financial Statement AnaysisДокумент8 страницCase Study - Financial Statement Anaysisssimi137Оценок пока нет

- Financial Planning and ForecastingДокумент16 страницFinancial Planning and ForecastingAzain UsmanОценок пока нет

- Far Chap 5 SolДокумент53 страницыFar Chap 5 SolCaterpillarОценок пока нет

- Chapter+2 3Документ14 страницChapter+2 3kanasanОценок пока нет

- Solution Manual For Fundamentals of Corporate Finance 10Th Edition by Ross Westerfield Jordan Isbn 0078034639 9780078034633 Full Chapter PDFДокумент33 страницыSolution Manual For Fundamentals of Corporate Finance 10Th Edition by Ross Westerfield Jordan Isbn 0078034639 9780078034633 Full Chapter PDFjudy.pierce330100% (12)

- Financial Statements, Cash Flow, and TaxesДокумент40 страницFinancial Statements, Cash Flow, and TaxesKamran Ali AnsariОценок пока нет

- Investment Analysis and Portfolio Management 2012Документ61 страницаInvestment Analysis and Portfolio Management 2012Nelson Ivan Acosta100% (1)

- Practice Technicals 1Документ75 страницPractice Technicals 1tiger100% (1)

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryОт EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryОценок пока нет

- How to Read a Financial Report: Wringing Vital Signs Out of the NumbersОт EverandHow to Read a Financial Report: Wringing Vital Signs Out of the NumbersОценок пока нет

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryОт EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryОценок пока нет

- Catalina Rivas in The Holy MassДокумент5 страницCatalina Rivas in The Holy MassIngrid CaobleclolalОценок пока нет

- TMP - 10878-MEMO DBM NBC No. 580 DTD April 22, 2020526450378Документ2 страницыTMP - 10878-MEMO DBM NBC No. 580 DTD April 22, 2020526450378Ingrid CaobleclolalОценок пока нет

- Novena ST Vincent FerrerДокумент2 страницыNovena ST Vincent Ferrercaressestelito100% (3)

- Novena ST Vincent FerrerДокумент2 страницыNovena ST Vincent Ferrercaressestelito100% (3)

- COA Charts of Account C2004-002 - AnnexAДокумент17 страницCOA Charts of Account C2004-002 - AnnexAJohn Dale MondejarОценок пока нет

- Yummy Meals 2016Документ108 страницYummy Meals 2016Ingrid Caobleclolal100% (2)

- PPSAS 31 - Intangible Assets Oct - 18 2013Документ3 страницыPPSAS 31 - Intangible Assets Oct - 18 2013Ingrid CaobleclolalОценок пока нет

- URS Training - As of SEPT292017Документ158 страницURS Training - As of SEPT292017Ingrid CaobleclolalОценок пока нет

- SSS - Maternity Benefits ComputationДокумент2 страницыSSS - Maternity Benefits ComputationIngrid CaobleclolalОценок пока нет

- PPSAS 20 - Related Party Disclosures Oct-18 2013Документ3 страницыPPSAS 20 - Related Party Disclosures Oct-18 2013Ingrid CaobleclolalОценок пока нет

- Budgeting 101 26janДокумент25 страницBudgeting 101 26janIngrid CaobleclolalОценок пока нет

- PPSAS 02 - Cash Flows Statements Oct-18 2013Документ3 страницыPPSAS 02 - Cash Flows Statements Oct-18 2013Ingrid CaobleclolalОценок пока нет

- GlossaryДокумент16 страницGlossaryEmmanuel AbadОценок пока нет

- PPSAS 32 - Service Concession Oct - 18 2013Документ3 страницыPPSAS 32 - Service Concession Oct - 18 2013Ingrid CaobleclolalОценок пока нет

- PPSAS 03 - Changes in P & E and Errors Oct - 18 2013Документ3 страницыPPSAS 03 - Changes in P & E and Errors Oct - 18 2013Ingrid CaobleclolalОценок пока нет

- Philippine Public Sector Accounting Standard 12 InventoriesДокумент3 страницыPhilippine Public Sector Accounting Standard 12 InventoriesIngrid Caobleclolal100% (1)

- Preface To PPSAS 10-18 2013Документ4 страницыPreface To PPSAS 10-18 2013Ingrid CaobleclolalОценок пока нет

- PPSAS 05 - Borrowing Cost Oct-18 2013Документ3 страницыPPSAS 05 - Borrowing Cost Oct-18 2013Ingrid CaobleclolalОценок пока нет

- Philippine Public Sector Accounting Standard 8 Interest in Joint VenturesДокумент3 страницыPhilippine Public Sector Accounting Standard 8 Interest in Joint VenturesIngrid CaobleclolalОценок пока нет

- Philippine Public Sector Accounting Standards 9 Revenue From Exchange TransactionsДокумент3 страницыPhilippine Public Sector Accounting Standards 9 Revenue From Exchange TransactionsIngrid CaobleclolalОценок пока нет

- FM Final Case March 2015Документ5 страницFM Final Case March 2015Ingrid CaobleclolalОценок пока нет

- Budgeting 101 26janДокумент25 страницBudgeting 101 26janIngrid CaobleclolalОценок пока нет

- Procurement Planning and MonitoringДокумент53 страницыProcurement Planning and MonitoringIngrid Caobleclolal85% (13)

- PPSAS 04 - Effects of Forex Oct-18 2013Документ3 страницыPPSAS 04 - Effects of Forex Oct-18 2013Ingrid CaobleclolalОценок пока нет

- Financial Ratio Analysis PDFДокумент22 страницыFinancial Ratio Analysis PDFIngrid CaobleclolalОценок пока нет

- Unclaimed Balances LawДокумент17 страницUnclaimed Balances LawFritchel Mae QuicosОценок пока нет

- Audit Check ListДокумент8 страницAudit Check ListpriyeshОценок пока нет

- The Elliott Wave PrincipleДокумент4 страницыThe Elliott Wave PrincipledewanibipinОценок пока нет

- Ketan RathodДокумент92 страницыKetan RathodKetan RathodОценок пока нет

- Investment Triangle TriangleДокумент2 страницыInvestment Triangle TriangleramakrishnanОценок пока нет

- Export Advance Payment - Branch ProposalДокумент2 страницыExport Advance Payment - Branch ProposalKumar SwamyОценок пока нет

- PRIDE INTERNATIONAL INC 10-K (Annual Reports) 2009-02-25Документ142 страницыPRIDE INTERNATIONAL INC 10-K (Annual Reports) 2009-02-25http://secwatch.com100% (5)

- Revenue Memo Ruling 02-2002Документ20 страницRevenue Memo Ruling 02-2002Annie SibayanОценок пока нет

- Arbitrage Pricing TheoryДокумент16 страницArbitrage Pricing Theorya_karimОценок пока нет

- Preliminary PagesДокумент17 страницPreliminary PagesvanexoxoОценок пока нет

- Daftar Akun Pt. Manunggal (Hilma)Документ4 страницыDaftar Akun Pt. Manunggal (Hilma)Adhitya RamadhanОценок пока нет

- 4 L GST Certificate New PDFДокумент3 страницы4 L GST Certificate New PDFSuhas SuviОценок пока нет

- Chapter 6 Financial Estimates and ProjectionsДокумент19 страницChapter 6 Financial Estimates and ProjectionskabibhandariОценок пока нет

- Nestle India Valuation ReportДокумент10 страницNestle India Valuation ReportSIDDHANT MOHAPATRAОценок пока нет

- Tvs CreditДокумент1 страницаTvs CreditorugalluОценок пока нет

- Salary Pay Slip Model PDF FreeДокумент1 страницаSalary Pay Slip Model PDF FreeAYUSH PRADHANОценок пока нет

- Loblaws Annual Report 2019Документ138 страницLoblaws Annual Report 2019Anupriyam RanjitОценок пока нет

- Local Budget Circular No. 111 - Manual On The Setting Up and Operation of Local Economic Enterprises (Lees)Документ3 страницыLocal Budget Circular No. 111 - Manual On The Setting Up and Operation of Local Economic Enterprises (Lees)Glaiza RafaОценок пока нет

- Step by Step Sap GL User ManualДокумент109 страницStep by Step Sap GL User Manualkapil_73Оценок пока нет

- Chapter4 IA Midterm BuenaventuraДокумент10 страницChapter4 IA Midterm BuenaventuraAnonnОценок пока нет

- Haberberg and Rieple: Strategic ManagementДокумент20 страницHaberberg and Rieple: Strategic ManagementMilan MisraОценок пока нет

- Graduated - Tax Base Is Net Income 8% - Tax Base Is Gross IncomeДокумент9 страницGraduated - Tax Base Is Net Income 8% - Tax Base Is Gross IncomeFrancis Kyle Cagalingan SubidoОценок пока нет

- Solution Manual For Intermediate Accounting IFRS 4th Edition by Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield Chapter 1 - 24Документ70 страницSolution Manual For Intermediate Accounting IFRS 4th Edition by Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield Chapter 1 - 24marcuskenyatta27550% (2)

- Mbaproject - Kotak Sec PDFДокумент63 страницыMbaproject - Kotak Sec PDFNAWAZ SHAIKHОценок пока нет

- CS FORM 7 ClearanceДокумент8 страницCS FORM 7 ClearanceKristelle Dee MijaresОценок пока нет

- Plan807 Charu 15Документ3 страницыPlan807 Charu 15Sambhaji KoliОценок пока нет

- LTDДокумент3 страницыLTDAustine CamposОценок пока нет

- The Standard Trade Model: Slides Prepared by Thomas BishopДокумент56 страницThe Standard Trade Model: Slides Prepared by Thomas BishopNguyên BùiОценок пока нет

- Gill Wilkins Technology Transfer For Renewable Energy Overcoming Barriers in Developing CountriesДокумент256 страницGill Wilkins Technology Transfer For Renewable Energy Overcoming Barriers in Developing CountriesmshameliОценок пока нет

- CH 09Документ94 страницыCH 09ayu utamiОценок пока нет