Вам также может понравиться

- CFA Course Key Concepts Risk Return Part ITITLE CFA Course Portfolio Concept Checkers Risk ReturnДокумент7 страницCFA Course Key Concepts Risk Return Part ITITLE CFA Course Portfolio Concept Checkers Risk ReturnAditya NugrohoОценок пока нет

- CApm DerivationДокумент27 страницCApm Derivationpaolo_nogueraОценок пока нет

- Capital Asset Pricing Model: Make smart investment decisions to build a strong portfolioОт EverandCapital Asset Pricing Model: Make smart investment decisions to build a strong portfolioРейтинг: 4.5 из 5 звезд4.5/5 (3)

- Chapter 8 - Introduction To Asset Pricing ModelsДокумент53 страницыChapter 8 - Introduction To Asset Pricing Modelsmustafa-memon-7379100% (3)

- Markowitz ModelДокумент63 страницыMarkowitz ModeldrramaiyaОценок пока нет

- Capital Market Theory: What Happens When A Risk-Free Asset Is Added To A Portfolio of Risky Assets?Документ5 страницCapital Market Theory: What Happens When A Risk-Free Asset Is Added To A Portfolio of Risky Assets?Padyala SriramОценок пока нет

- 0522 Capital Allocation UNIT 5Документ69 страниц0522 Capital Allocation UNIT 5fadiismaОценок пока нет

- Return and Risk:: Portfolio Theory AND Capital Asset Pricing Model (Capm)Документ52 страницыReturn and Risk:: Portfolio Theory AND Capital Asset Pricing Model (Capm)anna_alwanОценок пока нет

- Lecture-5 Investors Utility and CALДокумент26 страницLecture-5 Investors Utility and CALHabiba BiboОценок пока нет

- 14 Chapter 7Документ16 страниц14 Chapter 7tarek khanОценок пока нет

- Capital Asset Pricing Theory and Arbitrage Pricing TheoryДокумент19 страницCapital Asset Pricing Theory and Arbitrage Pricing TheoryMohammed ShafiОценок пока нет

- Mynotes - Lecture - 8.1 - MeanVariance - Capital AllocationДокумент3 страницыMynotes - Lecture - 8.1 - MeanVariance - Capital AllocationJoana ToméОценок пока нет

- CapmДокумент43 страницыCapmrocky bayasОценок пока нет

- Group 2 - Efficient Portfolio FormationДокумент29 страницGroup 2 - Efficient Portfolio FormationCindy permatasariОценок пока нет

- What Is A Portfolio?: Key TakeawaysДокумент7 страницWhat Is A Portfolio?: Key TakeawaysSabarni ChatterjeeОценок пока нет

- Portfolio Risk & Return: Calculating Expected Returns Using the Capital Allocation Line (CALДокумент54 страницыPortfolio Risk & Return: Calculating Expected Returns Using the Capital Allocation Line (CALalibuxjatoiОценок пока нет

- Portfolio Management - Capital Market TheoryДокумент2 страницыPortfolio Management - Capital Market Theorykegnata100% (2)

- Risk AversionДокумент8 страницRisk AversionFreddie Asiedu LarbiОценок пока нет

- Capm Vs Market ModelДокумент28 страницCapm Vs Market Modeldivyakud100% (1)

- 08 Risk and ReturnДокумент11 страниц08 Risk and Returnddrechsler9Оценок пока нет

- Capm 2Документ39 страницCapm 2rocky bayasОценок пока нет

- LECTURE 5b - Advances On Portfolio ManagementДокумент36 страницLECTURE 5b - Advances On Portfolio ManagementKim Hương Hoàng ThịОценок пока нет

- CML Vs SMLДокумент9 страницCML Vs SMLJoanna JacksonОценок пока нет

- Unit 5 SAPMДокумент26 страницUnit 5 SAPMMathangi VОценок пока нет

- Lecture # 6: Optimal Risky PortfolioДокумент36 страницLecture # 6: Optimal Risky PortfolioNguyễn VânОценок пока нет

- Financial Risk Management Problem Set 1Документ3 страницыFinancial Risk Management Problem Set 1Valentin IsОценок пока нет

- Investment Analysis and Portfolio Management: AssumptionsДокумент5 страницInvestment Analysis and Portfolio Management: AssumptionsMo ToОценок пока нет

- Arbitrage Pricing TheoryДокумент10 страницArbitrage Pricing TheoryarmailgmОценок пока нет

- Module 3-FM2Документ18 страницModule 3-FM2BeomiОценок пока нет

- Module 2 CAPMДокумент11 страницModule 2 CAPMTanvi DevadigaОценок пока нет

- Risk and Return: Capital Asset Pricing ModelДокумент25 страницRisk and Return: Capital Asset Pricing ModelRita NyairoОценок пока нет

- Investment Analysis and Portfolio Management: Lecture Presentation SoftwareДокумент77 страницInvestment Analysis and Portfolio Management: Lecture Presentation SoftwarekhandakeralihossainОценок пока нет

- Comsats Institute of Information Technology Islamabad: Page - 1Документ12 страницComsats Institute of Information Technology Islamabad: Page - 1Talha Abdul RaufОценок пока нет

- Chap 6Документ52 страницыChap 6Danial HemaniОценок пока нет

- FIN330 Chapter 17Документ21 страницаFIN330 Chapter 17NITHYA S MОценок пока нет

- Homework 1Документ3 страницыHomework 1wrt.ojtОценок пока нет

- Finman Risk and ReturnДокумент27 страницFinman Risk and ReturnJamelleОценок пока нет

- Problem Set 1Документ3 страницыProblem Set 1ikramraya0Оценок пока нет

- Chương 7 - QLDMĐTДокумент8 страницChương 7 - QLDMĐTNguyễn Thanh PhongОценок пока нет

- Chap006 Text BankДокумент14 страницChap006 Text BankAshraful AlamОценок пока нет

- Week 4 Lecture PDFДокумент69 страницWeek 4 Lecture PDFAkshat TiwariОценок пока нет

- Calculating portfolio risk and the CAPM modelДокумент4 страницыCalculating portfolio risk and the CAPM modelRachelОценок пока нет

- Corporate Finance HW 10Документ4 страницыCorporate Finance HW 10RachelОценок пока нет

- 03.risk and Return IIIДокумент6 страниц03.risk and Return IIIMaithri Vidana KariyakaranageОценок пока нет

- YhjhtyfyhfghfhfhfjhgsДокумент15 страницYhjhtyfyhfghfhfhfjhgsbabylovelylovelyОценок пока нет

- CAPM: Capital Asset Pricing Model ExplainedДокумент43 страницыCAPM: Capital Asset Pricing Model ExplainedProf.V.Vanaja sureshОценок пока нет

- Chapter 7 Portfolio Theory: Prepared By: Wael Shams EL-DinДокумент21 страницаChapter 7 Portfolio Theory: Prepared By: Wael Shams EL-DinmaheraldamatiОценок пока нет

- An Introduction To Asset Pricing Models: Questions To Be AnsweredДокумент45 страницAn Introduction To Asset Pricing Models: Questions To Be AnsweredEka Maisa YudistiraОценок пока нет

- Cfa Chapter 9 Problems: The Capital Asset Pricing ModelДокумент7 страницCfa Chapter 9 Problems: The Capital Asset Pricing ModelFagbola Oluwatobi Omolaja100% (1)

- Basic Principles: Amity Global Business SchoolДокумент32 страницыBasic Principles: Amity Global Business SchoolCharu AroraОценок пока нет

- Portfolio Management 1Документ28 страницPortfolio Management 1Sattar Md AbdusОценок пока нет

- Chapter 5 and 6 Security AnalysisДокумент5 страницChapter 5 and 6 Security AnalysisMohiuddin Al FarukОценок пока нет

- Diversification and Portfolio AnalysisДокумент14 страницDiversification and Portfolio AnalysisSaswati JaipuriaОценок пока нет

- 123 AwatgДокумент27 страниц123 AwatgPrasadi IidiotОценок пока нет

- SAPM Module 7Документ35 страницSAPM Module 7AnvibhaОценок пока нет

- Why Diversification Is KeyДокумент85 страницWhy Diversification Is Keymaulik18755Оценок пока нет

- Portfolio Theory ExplainedДокумент32 страницыPortfolio Theory ExplainedDicky IrawanОценок пока нет

- FDI in Pakistan PDFДокумент20 страницFDI in Pakistan PDFFazli WadoodОценок пока нет

- Labour and Employment Law-A Profile On PakistanДокумент13 страницLabour and Employment Law-A Profile On PakistanFazli WadoodОценок пока нет

- WBS Project Management PDFДокумент85 страницWBS Project Management PDFGilmer Patricio100% (1)

- Essential Elements of Effective TeamworkДокумент17 страницEssential Elements of Effective TeamworkFazli WadoodОценок пока нет

- MATO B PLAN FinalДокумент27 страницMATO B PLAN FinalJey MaxОценок пока нет

- Case Assignment 2Документ5 страницCase Assignment 2Ashish BhanotОценок пока нет

- International Financial Reporting Standards (IFRS) OverviewДокумент212 страницInternational Financial Reporting Standards (IFRS) OverviewVenkata Sambhasiva Rao Cheedella100% (1)

- Research proposal on fast food brand perception in VietnamДокумент5 страницResearch proposal on fast food brand perception in VietnamHuỳnh ChâuОценок пока нет

- Chapter 6 PDFДокумент28 страницChapter 6 PDFDiva CarissaОценок пока нет

- Using Procure To Order' To Source Buy Items Cross OrganizationsДокумент46 страницUsing Procure To Order' To Source Buy Items Cross OrganizationsNidhi SaxenaОценок пока нет

- Capsim Decisions AssistДокумент68 страницCapsim Decisions AssistRose KОценок пока нет

- Acct Principles and Assumption - Week1Документ4 страницыAcct Principles and Assumption - Week1Hà Chi NguyễnОценок пока нет

- 5.IAS 23 .Borrowing Cost Q&AДокумент12 страниц5.IAS 23 .Borrowing Cost Q&AAbdulkarim Hamisi KufakunogaОценок пока нет

- Ma. Theresa R. TrinidadДокумент3 страницыMa. Theresa R. TrinidadJoshua CalaОценок пока нет

- Adjusting Journal EntriesДокумент11 страницAdjusting Journal EntriesKatrina RomasantaОценок пока нет

- 8 Identifying Market Segments and TargetsДокумент33 страницы8 Identifying Market Segments and TargetsSepti A. PratiwiОценок пока нет

- Investors Perception Towards The Mutual Funds - Reliance SecuritiesДокумент83 страницыInvestors Perception Towards The Mutual Funds - Reliance Securitiesorsashok100% (2)

- Ukpr19 Disney Emea BriefДокумент2 страницыUkpr19 Disney Emea Briefapi-457838992Оценок пока нет

- University of California PE and VC IRR ReturnsДокумент5 страницUniversity of California PE and VC IRR Returnsdavidsun1988Оценок пока нет

- Case Radiance Transaction Level PricingДокумент10 страницCase Radiance Transaction Level PricingSanya TОценок пока нет

- Week 5 Chapter 11Документ6 страницWeek 5 Chapter 11CIA190116 STUDENTОценок пока нет

- Infomercial ProjectДокумент6 страницInfomercial ProjectMichele McNickleОценок пока нет

- Drilll 7 ReceivablesДокумент4 страницыDrilll 7 ReceivablesEDELYN PoblacionОценок пока нет

- Name: Nikhil P. PalanДокумент7 страницName: Nikhil P. PalanVinit BhindeОценок пока нет

- Caf 8 Cma Autumn 2020Документ5 страницCaf 8 Cma Autumn 2020Hassnain SardarОценок пока нет

- Understanding Income Statements EPS CalculationsДокумент39 страницUnderstanding Income Statements EPS CalculationsKeshav KaplushОценок пока нет

- Introduction To Economics - ppt1Документ13 страницIntroduction To Economics - ppt1Akshay HemanthОценок пока нет

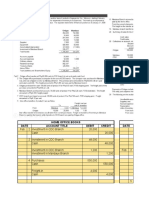

- Home Office Books Mandaue Books Date Account Title Debit Credit DateДокумент27 страницHome Office Books Mandaue Books Date Account Title Debit Credit DateVon Andrei MedinaОценок пока нет

- MarketLineIC CanadaManagementMarketingConsultancy 201122Документ42 страницыMarketLineIC CanadaManagementMarketingConsultancy 201122michelleee2064 yuОценок пока нет

- Post Fin2004 Final Sem 2 2010Документ11 страницPost Fin2004 Final Sem 2 2010Bi ChenОценок пока нет

- CH 2Документ19 страницCH 2yebegashetОценок пока нет

- Rupali Bank StatementДокумент1 страницаRupali Bank StatementMd YousufОценок пока нет

- Cost Accounting - Chapter 10Документ14 страницCost Accounting - Chapter 10xxxxxxxxx67% (6)

- Jungle Scout Amazon Vs Walmart Report 2021Документ18 страницJungle Scout Amazon Vs Walmart Report 2021Emil RiosОценок пока нет