Вам также может понравиться

- PPE PPT - Ch10Документ81 страницаPPE PPT - Ch10ssreya80Оценок пока нет

- Lecture - 6 - Long - Term - Assets - NUS ACC1002 2020 SpringДокумент49 страницLecture - 6 - Long - Term - Assets - NUS ACC1002 2020 SpringZenyui100% (1)

- Adjusting Accounts and Preparing Financial Statements: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinДокумент58 страницAdjusting Accounts and Preparing Financial Statements: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinYvonne Teo Yee VoonОценок пока нет

- Reporting and Interpreting Property, Plant and Equipment Natural Resources and IntangiblesДокумент29 страницReporting and Interpreting Property, Plant and Equipment Natural Resources and IntangiblesHammad ShamsiОценок пока нет

- Review of Chapter 6Документ54 страницыReview of Chapter 6BookAddict721Оценок пока нет

- Chap 10Документ43 страницыChap 10Boo LeОценок пока нет

- Chapter 10 Plant Assets, Natural Resources, and Intangible Assets (13 E)Документ18 страницChapter 10 Plant Assets, Natural Resources, and Intangible Assets (13 E)Raa100% (1)

- Chapter 10 SolutionsДокумент70 страницChapter 10 SolutionsLy VõОценок пока нет

- Long Live AssetsДокумент16 страницLong Live AssetsLu CasОценок пока нет

- ACC 1100 Days 14&15 Long-Lived Assets PDFДокумент25 страницACC 1100 Days 14&15 Long-Lived Assets PDFYevhenii VdovenkoОценок пока нет

- Week 12 - Capex and DepreciationДокумент55 страницWeek 12 - Capex and DepreciationajenggОценок пока нет

- Ifsa Chapter9Документ42 страницыIfsa Chapter9Iwan PutraОценок пока нет

- Chapter 9 Feb.19Документ69 страницChapter 9 Feb.19AaaОценок пока нет

- Preparing Financial Statements: © The Mcgraw-Hill Companies, Inc., 2007 Mcgraw-Hill/IrwinДокумент34 страницыPreparing Financial Statements: © The Mcgraw-Hill Companies, Inc., 2007 Mcgraw-Hill/IrwinQuynhGiao Nguyen TaОценок пока нет

- LECTURE NOTES - DepreciationДокумент28 страницLECTURE NOTES - Depreciationhua chen yuОценок пока нет

- Horngrens Accounting 10Th Edition Nobles Solutions Manual Full Chapter PDFДокумент36 страницHorngrens Accounting 10Th Edition Nobles Solutions Manual Full Chapter PDFelizabeth.hayes136100% (11)

- Plant Assets: Created by Ina IndrianaДокумент23 страницыPlant Assets: Created by Ina IndrianadewiestiОценок пока нет

- Chapters 8 and 9: Capital Budgeting: Ppts To Accompany Fundamentals of Corporate Finance 6E by Ross Et AlДокумент42 страницыChapters 8 and 9: Capital Budgeting: Ppts To Accompany Fundamentals of Corporate Finance 6E by Ross Et AlAbel100% (1)

- Financial Accounting Information For Decisions 6th Edition Wild Solutions ManualДокумент44 страницыFinancial Accounting Information For Decisions 6th Edition Wild Solutions Manualfinnhuynhqvzp2c100% (23)

- Plant Assets, Natural Resources and Intangibles: QuestionsДокумент42 страницыPlant Assets, Natural Resources and Intangibles: QuestionsCh Radeel MurtazaОценок пока нет

- Acounting Aacounting Aacounting Aacounting AДокумент8 страницAcounting Aacounting Aacounting Aacounting AFrankyLimОценок пока нет

- Taller Uno Acco 112Документ44 страницыTaller Uno Acco 112api-274120622Оценок пока нет

- BUSI 353 Assignment #6 General Instructions For All AssignmentsДокумент4 страницыBUSI 353 Assignment #6 General Instructions For All AssignmentsTan0% (1)

- MGMT 026 Chapter 10 SlidesДокумент46 страницMGMT 026 Chapter 10 SlidesBánh BaoОценок пока нет

- Introduction To Accounting 2 Modul 3 Plant Assets, Natural Resources, and Intangible AssetsДокумент23 страницыIntroduction To Accounting 2 Modul 3 Plant Assets, Natural Resources, and Intangible AssetsHABTAMU TULUОценок пока нет

- Lecture11 - Mar15 Long-Term Assets, Depreciation (Deferred Taxes) PDFДокумент6 страницLecture11 - Mar15 Long-Term Assets, Depreciation (Deferred Taxes) PDFjasminetsoОценок пока нет

- CHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)Документ20 страницCHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)VerrelyОценок пока нет

- Depreciation of Fixed AssetsДокумент13 страницDepreciation of Fixed Assetsρεrvy αlcнεмisτ (ραρi)Оценок пока нет

- Adjusting Entries Depreciation MethodДокумент11 страницAdjusting Entries Depreciation MethodClarissa Rivera VillalobosОценок пока нет

- Session 6 Long Term Assets - HandoutДокумент18 страницSession 6 Long Term Assets - HandoutPranav KumarОценок пока нет

- Capital and Revenue ExpenditureДокумент22 страницыCapital and Revenue ExpenditureTimi Dele100% (1)

- Accounting For Property, Plant, and EquipmentДокумент33 страницыAccounting For Property, Plant, and Equipmentnatinaelbahiru74Оценок пока нет

- Capital Budgeting DecisionsfДокумент120 страницCapital Budgeting DecisionsfJudith Ann EscobarОценок пока нет

- Long - Lived AssetsДокумент25 страницLong - Lived AssetsJeff KinutsОценок пока нет

- Chapter Three PPE Copy 2Документ15 страницChapter Three PPE Copy 2nachmarket30Оценок пока нет

- Depreciation Notes - Advanced AccountingДокумент16 страницDepreciation Notes - Advanced AccountingSam ChinthaОценок пока нет

- Final Exam, s2, 2019-FINALДокумент13 страницFinal Exam, s2, 2019-FINALReenalОценок пока нет

- Cost Accumulation For Job-Shop & Batch Production OperationsДокумент60 страницCost Accumulation For Job-Shop & Batch Production Operationstrillion5Оценок пока нет

- Plant Assets, Natural Resources, and Intangible AssetsДокумент48 страницPlant Assets, Natural Resources, and Intangible AssetsTiloma M. Zannat100% (1)

- Chap 016Документ69 страницChap 016Pooja Grover ShandilyaОценок пока нет

- Topic 6: Job Order CostingДокумент51 страницаTopic 6: Job Order CostingNa RaunaОценок пока нет

- ABEN125 - Lecture 2Документ18 страницABEN125 - Lecture 2PEARL ANGELIE UMBAОценок пока нет

- CR Questions Nov 18 Questions FinalДокумент18 страницCR Questions Nov 18 Questions Finalswarna dasОценок пока нет

- IFA Chapter 5Документ68 страницIFA Chapter 5kqk07829Оценок пока нет

- Chapter 9 PowerPointДокумент101 страницаChapter 9 PowerPointcheuleee100% (2)

- Depreciation 140513051242 Phpapp02Документ22 страницыDepreciation 140513051242 Phpapp020612001Оценок пока нет

- AIS16Exercises SCДокумент6 страницAIS16Exercises SCSarah GherdaouiОценок пока нет

- Jun18l1fra-C04 QaДокумент6 страницJun18l1fra-C04 QajuanОценок пока нет

- ACC101 Chapter8newДокумент19 страницACC101 Chapter8newLaras Sukma Nurani TirtawidjajaОценок пока нет

- Tutorial Solution Week 06Документ4 страницыTutorial Solution Week 06itmansaigonОценок пока нет

- Financial Accounting IIДокумент13 страницFinancial Accounting IITimi DeleОценок пока нет

- Basic Financial Model - User ManualДокумент5 страницBasic Financial Model - User ManualnexoseОценок пока нет

- Cost Management and Decision MakingДокумент56 страницCost Management and Decision MakingIsh SelinОценок пока нет

- 31.job Costing (Exercise Questions)Документ6 страниц31.job Costing (Exercise Questions)Harinesh PandyaОценок пока нет

- Baf 223 Accounting For Labilities - Depreciation NotesДокумент5 страницBaf 223 Accounting For Labilities - Depreciation Notesaroridouglas880Оценок пока нет

- 10 PpeДокумент53 страницы10 PpeSalsa Byla100% (1)

- Week 7 Case 19 - 28Документ2 страницыWeek 7 Case 19 - 28Sekar Wulan OktaviaОценок пока нет

- Homework AssignmentДокумент11 страницHomework AssignmentHenny DeWillisОценок пока нет

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageОт EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageРейтинг: 5 из 5 звезд5/5 (1)

- Reporting and Analyzing Equity: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinДокумент58 страницReporting and Analyzing Equity: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinYvonne Teo Yee VoonОценок пока нет

- Lecture 7 - Law of ContractsДокумент19 страницLecture 7 - Law of ContractsYvonne Teo Yee VoonОценок пока нет

- Lecture 2 - Civil Dispute ResolutionДокумент16 страницLecture 2 - Civil Dispute ResolutionYvonne Teo Yee VoonОценок пока нет

- Reporting and Analyzing Long-Term Liabilities: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinДокумент47 страницReporting and Analyzing Long-Term Liabilities: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinYvonne Teo Yee VoonОценок пока нет

- Lecture 14 - Employment LawДокумент12 страницLecture 14 - Employment LawYvonne Teo Yee VoonОценок пока нет

- Reporting and Analyzing Receivables: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinДокумент52 страницыReporting and Analyzing Receivables: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinYvonne Teo Yee VoonОценок пока нет

- Reporting and Analyzing Inventories: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinДокумент61 страницаReporting and Analyzing Inventories: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinYvonne Teo Yee VoonОценок пока нет

- VIVO - SHELL LIMITED Credit ReportДокумент19 страницVIVO - SHELL LIMITED Credit Reportsergiu botezОценок пока нет

- Igcse Depreciation - QuestionsДокумент50 страницIgcse Depreciation - QuestionsMuhammad MunaamОценок пока нет

- MAS - Working Capital ManagementДокумент7 страницMAS - Working Capital ManagementMary Dale Joie BocalaОценок пока нет

- Financial Comparirison Between Private and Public BankДокумент9 страницFinancial Comparirison Between Private and Public BankAmit PratapОценок пока нет

- MCQ Accounting StandardДокумент13 страницMCQ Accounting StandardNgân GiangОценок пока нет

- CH 02Документ12 страницCH 02Charles Decripito FloresОценок пока нет

- Credit Risk Analysis - Janani PrakashДокумент46 страницCredit Risk Analysis - Janani PrakashJanani Prakash87% (15)

- C10 Making Capital Investment DecisionshhhДокумент11 страницC10 Making Capital Investment DecisionshhhQuang Minh NguyễnОценок пока нет

- Chapter 16 - LeasingДокумент31 страницаChapter 16 - LeasingSakthi VelОценок пока нет

- Capstone - Edmonton Capital Project PrioritizationДокумент41 страницаCapstone - Edmonton Capital Project PrioritizationMahesh KumarОценок пока нет

- Divestiture SДокумент26 страницDivestiture SJoshua JoelОценок пока нет

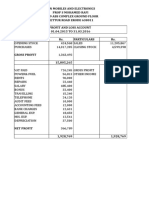

- Sun Mobiles and Electronics Prop S Mohamed Rafi No.19 Abs Complex Ground Floor Mettur Road Erode 638011 Profit and Loss Account 01.04.2015 TO 31.03.2016 Particulars Rs. Particulars RsДокумент6 страницSun Mobiles and Electronics Prop S Mohamed Rafi No.19 Abs Complex Ground Floor Mettur Road Erode 638011 Profit and Loss Account 01.04.2015 TO 31.03.2016 Particulars Rs. Particulars RssamaadhuОценок пока нет

- F2 Revision SummariesДокумент97 страницF2 Revision Summarieswakomoli100% (2)

- John Sagan - Toward A Theory of Working Capital Management (1955)Документ10 страницJohn Sagan - Toward A Theory of Working Capital Management (1955)Pedro VazОценок пока нет

- Financial Accounting - From Its Basics To Financial Reporting and Analysis (2020, Cambridge Scholars Publishing)Документ445 страницFinancial Accounting - From Its Basics To Financial Reporting and Analysis (2020, Cambridge Scholars Publishing)al chemiste100% (1)

- SAA Versus TAA 2009-01Документ5 страницSAA Versus TAA 2009-01domomwambiОценок пока нет

- Chapter 5 - Test BankДокумент17 страницChapter 5 - Test Bankhipduggy100% (2)

- Final ProjectДокумент59 страницFinal ProjectshelarnamdevОценок пока нет

- Financial Management Notes SRK UNIT 2Документ13 страницFinancial Management Notes SRK UNIT 2Pruthvi RajОценок пока нет

- Balance Sheet For Intel CorpДокумент2 страницыBalance Sheet For Intel CorpriskyindraОценок пока нет

- Kvs Jaipur Xii Acc QP & Ms (2nd PB) 23-24 (Set-1)Документ11 страницKvs Jaipur Xii Acc QP & Ms (2nd PB) 23-24 (Set-1)Sanjay PanickerОценок пока нет

- Accounting Methods For GoodwillДокумент4 страницыAccounting Methods For GoodwillaskmeeОценок пока нет

- MIS Essentials 4th Edition Kroenke Solutions Manual DownloadДокумент14 страницMIS Essentials 4th Edition Kroenke Solutions Manual DownloadLouise Roth100% (13)

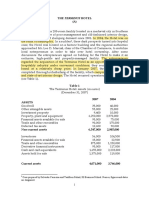

- Terminus Hotel-AДокумент4 страницыTerminus Hotel-AVrinda MalikОценок пока нет

- Anlisis Soal Kasus PT BerkahДокумент7 страницAnlisis Soal Kasus PT Berkahputri nobellaОценок пока нет

- Personal Financial Planning Personal Financial PlanningДокумент35 страницPersonal Financial Planning Personal Financial Planningsabarais100% (3)

- Business Plan - TOCДокумент19 страницBusiness Plan - TOCdprosenjitОценок пока нет

- 2607y Maliyyə Hesabatı SABAH (En)Документ34 страницы2607y Maliyyə Hesabatı SABAH (En)leylaОценок пока нет

- Sapphire Corporation Limited Annual Report 2015Документ118 страницSapphire Corporation Limited Annual Report 2015WeR1 Consultants Pte LtdОценок пока нет

- Financial Management June 2010 Marks PlanДокумент7 страницFinancial Management June 2010 Marks Plankarlr9Оценок пока нет