Вам также может понравиться

- Aryaduta Hotel - Heart of Contemporary IndonesiaДокумент1 страницаAryaduta Hotel - Heart of Contemporary IndonesiaJahja AjaОценок пока нет

- Jahja - Leadership Week in Beijing - Reflection PaperДокумент3 страницыJahja - Leadership Week in Beijing - Reflection PaperJahja AjaОценок пока нет

- Group 5 - Grolsch GloballyДокумент3 страницыGroup 5 - Grolsch GloballyJahja AjaОценок пока нет

- WAC Apollo Hospitals - JahjaДокумент2 страницыWAC Apollo Hospitals - JahjaJahja Aja0% (1)

- Boiler Installation Project 1Документ3 страницыBoiler Installation Project 1Jahja AjaОценок пока нет

- Group 5 - Grolsch GloballyДокумент3 страницыGroup 5 - Grolsch GloballyJahja AjaОценок пока нет

- HRДокумент29 страницHRJahja AjaОценок пока нет

- WAC Understanding Political Polls - JahjaДокумент2 страницыWAC Understanding Political Polls - JahjaJahja AjaОценок пока нет

- Exam International MarketingДокумент1 страницаExam International MarketingJahja AjaОценок пока нет

- Finance 3 Essay ExamДокумент2 страницыFinance 3 Essay ExamJahja AjaОценок пока нет

- HRДокумент29 страницHRJahja AjaОценок пока нет

- Boiler Installation Project 1Документ3 страницыBoiler Installation Project 1Jahja AjaОценок пока нет

- Nestlé Management Trainee ProgramДокумент10 страницNestlé Management Trainee ProgramRiki Risandi100% (1)

- Ses 9 - Nissan's Carlos GhosnДокумент14 страницSes 9 - Nissan's Carlos GhosnJahja Aja100% (1)

- Accenture HR Shared Services Foundation Integrated Talent ManagementДокумент12 страницAccenture HR Shared Services Foundation Integrated Talent ManagementJahja AjaОценок пока нет

- Finance 3 Essay ExamДокумент2 страницыFinance 3 Essay ExamJahja AjaОценок пока нет

- Prof Faustino's speech on the fifth 'P' of marketingДокумент5 страницProf Faustino's speech on the fifth 'P' of marketingJahja AjaОценок пока нет

- KPI Dictionary Vol2 PreviewДокумент12 страницKPI Dictionary Vol2 PreviewJahja Aja100% (1)

- Marketing Final Examination 01Документ4 страницыMarketing Final Examination 01Jahja AjaОценок пока нет

- Income Statement: Multi-Step FormatДокумент1 страницаIncome Statement: Multi-Step FormatJahja AjaОценок пока нет

- KPI Dictionary Vol1 PreviewДокумент12 страницKPI Dictionary Vol1 PreviewJahja Aja64% (11)

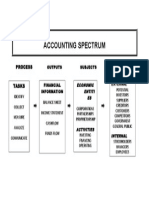

- Accounting SpectrumДокумент1 страницаAccounting SpectrumJahja AjaОценок пока нет

- Accounting SpectrumДокумент1 страницаAccounting SpectrumJahja AjaОценок пока нет

- Wendys AnalysisДокумент31 страницаWendys AnalysisJahja Aja100% (1)

- Sample Strategy MapsДокумент10 страницSample Strategy MapsJahja AjaОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Horngren 9th Edition Solutions Ch2Документ119 страницHorngren 9th Edition Solutions Ch2flowerkm80% (5)

- 2012 Syllabus 11 AccountancyДокумент4 страницы2012 Syllabus 11 AccountancyYadira TerryОценок пока нет

- Posted Sols Ch12Документ13 страницPosted Sols Ch12Jerry WongОценок пока нет

- Self Study Solutions Chapter 3Документ27 страницSelf Study Solutions Chapter 3flowerkmОценок пока нет

- Accounting 2Документ6 страницAccounting 2ANDRES MIGUEL ZAMBRANO DURANОценок пока нет

- IRCON leave rules summaryДокумент13 страницIRCON leave rules summarypriyanka joshiОценок пока нет

- Retail Banking in IndiaДокумент38 страницRetail Banking in IndiaYaadrahulkumar MoharanaОценок пока нет

- Maybank Islamic Account StatementДокумент13 страницMaybank Islamic Account StatementAdeela fazlinОценок пока нет

- Creditors Reconciliation WorksheetДокумент23 страницыCreditors Reconciliation WorksheetMuto riroОценок пока нет

- Oracle GL ConceptsДокумент53 страницыOracle GL ConceptsKhurram HussainОценок пока нет

- CRC-ACE REVIEW SCHOOL AUDITING PROBLEMSДокумент8 страницCRC-ACE REVIEW SCHOOL AUDITING PROBLEMSLuzviminda Maruzzo100% (2)

- Chapter 7 Practice ProblemsДокумент6 страницChapter 7 Practice Problemsaccounting prob100% (1)

- Icfr ChklistДокумент16 страницIcfr Chklistananda_joshi5178100% (1)

- Problems Audit of Property Plant and Equipmentdocx PresentДокумент10 страницProblems Audit of Property Plant and Equipmentdocx PresentDominic RomeroОценок пока нет

- Dwnload Full Intermediate Accounting 19th Edition Stice Test Bank PDFДокумент35 страницDwnload Full Intermediate Accounting 19th Edition Stice Test Bank PDFspitznoglecorynn100% (7)

- Finance For Non Finance ManagersДокумент288 страницFinance For Non Finance ManagersZachary HuffmanОценок пока нет

- Types of Accounting RecordsДокумент3 страницыTypes of Accounting RecordsMatthewJoshuaSosito100% (2)

- Financial Accounting Chapter 3Документ50 страницFinancial Accounting Chapter 3abhinav2018Оценок пока нет

- Wey IFRS 4e PPT Ch05 (Accountingfor Merchandise Operations)Документ88 страницWey IFRS 4e PPT Ch05 (Accountingfor Merchandise Operations)Ruiran CuiОценок пока нет

- DK Goel Solutions Class 11 Chapter 9 Journal Entry ExamplesДокумент44 страницыDK Goel Solutions Class 11 Chapter 9 Journal Entry Examplesvishwas jagrawalОценок пока нет

- Advanced Accounting Part 2 Dayag 2015 Chapter 12Документ17 страницAdvanced Accounting Part 2 Dayag 2015 Chapter 12crispyy turon100% (1)

- PROBLEMS ON LIABILITIES AND CURRENTLY MATURING OBLIGATIONSДокумент29 страницPROBLEMS ON LIABILITIES AND CURRENTLY MATURING OBLIGATIONSDivine CuasayОценок пока нет

- Quiz 1: Introduction To Accounting and BookkeepingДокумент37 страницQuiz 1: Introduction To Accounting and BookkeepingDiana Rose BassigОценок пока нет

- Journal Entries For Long Lived AssetsДокумент2 страницыJournal Entries For Long Lived AssetsMary100% (20)

- Manage SEPA payments and filesДокумент4 страницыManage SEPA payments and filesninadgoodОценок пока нет

- ADBM – Full Time Financial Accounting Multiple Choice QuestionsДокумент8 страницADBM – Full Time Financial Accounting Multiple Choice QuestionsAshika JayaweeraОценок пока нет

- 11th Accountancy Study Material em 1Документ25 страниц11th Accountancy Study Material em 1yaseenОценок пока нет

- Account Statement From 1 Oct 2020 To 30 Sep 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент14 страницAccount Statement From 1 Oct 2020 To 30 Sep 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAartiОценок пока нет

- Chapter 4 AccountingДокумент22 страницыChapter 4 AccountingChan Man SeongОценок пока нет

- August 20 DiscussionДокумент26 страницAugust 20 DiscussionJOSCEL SYJONGTIANОценок пока нет