Вам также может понравиться

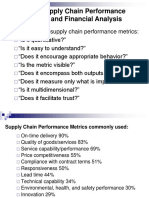

- Chapter 5: Supply Chain Performance Measurement and Financial AnalysisДокумент10 страницChapter 5: Supply Chain Performance Measurement and Financial Analysisyuvraj216Оценок пока нет

- Lakshmi Mittal - Lakshmi Mittal: " Steel King " " Steel King "Документ25 страницLakshmi Mittal - Lakshmi Mittal: " Steel King " " Steel King "yuvraj216Оценок пока нет

- Soft Skillsthe Term Soft Skills Is A Broad Topic. Below Are Some Sample Categories That Might BeДокумент2 страницыSoft Skillsthe Term Soft Skills Is A Broad Topic. Below Are Some Sample Categories That Might Beyuvraj216Оценок пока нет

- Income Statement: RatiosДокумент6 страницIncome Statement: Ratiosyuvraj216Оценок пока нет

- Discount Rate Growth Rate 2015: Total Intrinsic ValueДокумент11 страницDiscount Rate Growth Rate 2015: Total Intrinsic Valueyuvraj216Оценок пока нет

- The U.S. Treasury: Types of Markets and Auctions Petar Petrov ECON 1465, Fall 2010 Brown UniversityДокумент19 страницThe U.S. Treasury: Types of Markets and Auctions Petar Petrov ECON 1465, Fall 2010 Brown Universityyuvraj216Оценок пока нет

- Unemployment in YouthДокумент13 страницUnemployment in Youthyuvraj216Оценок пока нет

- Business Ethics On Airtel: Submitted ToДокумент26 страницBusiness Ethics On Airtel: Submitted Toyuvraj216Оценок пока нет

- Relative Valuation: JK Tyres 5.57 MRF 9.27 Ceat 9.44 TVS 12.35 Goodyear India 11.31Документ2 страницыRelative Valuation: JK Tyres 5.57 MRF 9.27 Ceat 9.44 TVS 12.35 Goodyear India 11.31yuvraj216Оценок пока нет

- System Collapse: The Case of Long Term Capital Management (LTCM)Документ17 страницSystem Collapse: The Case of Long Term Capital Management (LTCM)yuvraj216Оценок пока нет

- Bharti Airtel Limited, Commonly Known As Airtel, Is An IndianДокумент25 страницBharti Airtel Limited, Commonly Known As Airtel, Is An Indianyuvraj216Оценок пока нет

- A Seminar Report On: "Swing Bowling in Cricket"Документ4 страницыA Seminar Report On: "Swing Bowling in Cricket"yuvraj216Оценок пока нет

- Negi NavДокумент2 страницыNegi Navyuvraj216Оценок пока нет

- Atulauto Hbjcapital 131120103110 Phpapp01Документ32 страницыAtulauto Hbjcapital 131120103110 Phpapp01yuvraj216Оценок пока нет

- Prit SynopsisДокумент1 страницаPrit Synopsisyuvraj216Оценок пока нет

- 2.after Moa and Aoa Inc 8Документ2 страницы2.after Moa and Aoa Inc 8yuvraj216Оценок пока нет

- Airtel Code of EthicsДокумент13 страницAirtel Code of Ethicsyuvraj216Оценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- ALHAMBRA CIGAR Vs SECДокумент3 страницыALHAMBRA CIGAR Vs SECIraОценок пока нет

- CIR Vs Team PhilippinesДокумент4 страницыCIR Vs Team PhilippinesJennylyn Biltz AlbanoОценок пока нет

- GPPB Resolution 29-2014 Pcab LicenseДокумент5 страницGPPB Resolution 29-2014 Pcab LicenserubydelacruzОценок пока нет

- Membership Purchase - AgreementДокумент5 страницMembership Purchase - AgreementThomas Headen III100% (1)

- Electrical Design PrinciplesДокумент12 страницElectrical Design PrinciplesLJ IDANE ARANASОценок пока нет

- Organizational EthicsДокумент19 страницOrganizational EthicsSanna KazmiОценок пока нет

- Australian Standard: Health and Safety at Work - Principles and PracticesДокумент10 страницAustralian Standard: Health and Safety at Work - Principles and PracticesM. Gunawan BudisusilaОценок пока нет

- Maintenance Section - Module 2-A D.O. No. 41, S. 2016 Amended Policy Guidelines On The Maintenance of National Roads and BridgesДокумент3 страницыMaintenance Section - Module 2-A D.O. No. 41, S. 2016 Amended Policy Guidelines On The Maintenance of National Roads and BridgesHatdugОценок пока нет

- New RegistrationДокумент2 страницыNew RegistrationSadiri Roy D AragonОценок пока нет

- Corporate Governance in China-Final PaperДокумент19 страницCorporate Governance in China-Final PaperLillian KobusingyeОценок пока нет

- 13th Month Pay LawДокумент7 страниц13th Month Pay LawOrlando O. Calundan100% (1)

- Finance New SiДокумент5 страницFinance New SiTheFamous SalmanОценок пока нет

- LET 6e-TB-Ch03Документ24 страницыLET 6e-TB-Ch03sulemanОценок пока нет

- Right of Pre-Emption in Muslim Law & Land Laws of BangladeshДокумент12 страницRight of Pre-Emption in Muslim Law & Land Laws of BangladeshbaneaminОценок пока нет

- KOPPERS INC 10-K (Annual Reports) 2009-02-20Документ288 страницKOPPERS INC 10-K (Annual Reports) 2009-02-20http://secwatch.com100% (2)

- Ppa 2011Документ150 страницPpa 2011Elias100% (1)

- Parking Streetsmarts: City of Houston ParkhoustonДокумент22 страницыParking Streetsmarts: City of Houston ParkhoustonWilson LimpoОценок пока нет

- Draft Del Act New Classes CEN TC154 Aggregates For SCsДокумент48 страницDraft Del Act New Classes CEN TC154 Aggregates For SCshalexing5957Оценок пока нет

- UNDP Financial Regulations and RulesДокумент58 страницUNDP Financial Regulations and RulesBaigalmaa NyamtserenОценок пока нет

- FLS011 Application For PenCon Special STLДокумент2 страницыFLS011 Application For PenCon Special STLwillienorОценок пока нет

- Test Bank For Accounting Information Systems 1e by Turner and WeickgenanntДокумент16 страницTest Bank For Accounting Information Systems 1e by Turner and Weickgenanntcynthiaacostabsjeiaxmqk100% (37)

- CarriageДокумент12 страницCarriageHasanОценок пока нет

- Hipaa 101 Fact SheetДокумент3 страницыHipaa 101 Fact SheetKaleem ShaikОценок пока нет

- Bill of Lading 2 PDFДокумент2 страницыBill of Lading 2 PDFAnonymous pj1Zz073Оценок пока нет

- UTP Outline & NotesДокумент85 страницUTP Outline & NotesCassandra BestОценок пока нет

- Executive Order 11004Документ3 страницыExecutive Order 11004Jeremy GreenОценок пока нет

- Pekamco Nda&NcaДокумент2 страницыPekamco Nda&NcaAhmer JalilОценок пока нет

- Abbott Lab Vs AlcarazДокумент12 страницAbbott Lab Vs AlcarazKornessa ParasОценок пока нет

- Corporate Identity ManualДокумент49 страницCorporate Identity Manualmysubicbay100% (1)

- 2018 BNP Paribas Integrated ReportДокумент56 страниц2018 BNP Paribas Integrated ReportKotha Anil Reddy (PGDM 18-20)Оценок пока нет