Вам также может понравиться

- Taxation Corporate Tax Indirect Tax Personal Tax Tax Authority ThailandДокумент2 страницыTaxation Corporate Tax Indirect Tax Personal Tax Tax Authority ThailandAaron Joy Dominguez PutianОценок пока нет

- Thailand TaxationДокумент14 страницThailand Taxationde4zyОценок пока нет

- Thailand AsДокумент3 страницыThailand AsAaron Joy Dominguez PutianОценок пока нет

- Philippnes TPДокумент18 страницPhilippnes TPAaron Joy Dominguez PutianОценок пока нет

- Philippines AsДокумент3 страницыPhilippines AsAaron Joy Dominguez PutianОценок пока нет

- South Korea Accounting StandardsДокумент2 страницыSouth Korea Accounting StandardsAaron Joy Dominguez PutianОценок пока нет

- KoreaДокумент21 страницаKoreaChimgeeChmgeОценок пока нет

- Accounting StandardsДокумент3 страницыAccounting StandardsAaron Joy Dominguez PutianОценок пока нет

- BOA Revision in CPA Exam SubjectsДокумент6 страницBOA Revision in CPA Exam SubjectsAaron Joy Dominguez PutianОценок пока нет

- Japan Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreДокумент15 страницJapan Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreKris MehtaОценок пока нет

- Accounting Standards Taxation ContdДокумент41 страницаAccounting Standards Taxation ContdAaron Joy Dominguez PutianОценок пока нет

- Accounting Standards Taxation ContdДокумент41 страницаAccounting Standards Taxation ContdAaron Joy Dominguez PutianОценок пока нет

- China Accounting StandardsДокумент3 страницыChina Accounting StandardsAaron Joy Dominguez PutianОценок пока нет

- China TPДокумент18 страницChina TPAaron Joy Dominguez PutianОценок пока нет

- Accounting Standards and Taxatio1Документ7 страницAccounting Standards and Taxatio1Aaron Joy Dominguez PutianОценок пока нет

- Boa Tos FarДокумент1 страницаBoa Tos FarAaron Joy Dominguez PutianОценок пока нет

- BOA TOS TaxДокумент2 страницыBOA TOS TaxMr. CopernicusОценок пока нет

- BOA Syllabus MASДокумент3 страницыBOA Syllabus MASLouie de la TorreОценок пока нет

- Boa Tos MasДокумент3 страницыBoa Tos MasAaron Joy Dominguez PutianОценок пока нет

- BOA School Insp Pp1Документ6 страницBOA School Insp Pp1Aaron Joy Dominguez PutianОценок пока нет

- BOA Syllabus FARДокумент3 страницыBOA Syllabus FARLouie de la TorreОценок пока нет

- Boa Syllabus RFBTДокумент4 страницыBoa Syllabus RFBTAaron Joy Dominguez PutianОценок пока нет

- Boa Pres (GTB)Документ24 страницыBoa Pres (GTB)Aaron Joy Dominguez PutianОценок пока нет

- Accounting Standards and Taxation: A. European Union I. Accounting Standards Adoption of IFRS by European UnionДокумент12 страницAccounting Standards and Taxation: A. European Union I. Accounting Standards Adoption of IFRS by European UnionAaron Joy Dominguez PutianОценок пока нет

- Non For Profit OrganizationДокумент11 страницNon For Profit OrganizationAaron Joy Dominguez PutianОценок пока нет

- BOA School Insp PPДокумент14 страницBOA School Insp PPAaron Joy Dominguez PutianОценок пока нет

- Boa MraДокумент14 страницBoa MraAaron Joy Dominguez PutianОценок пока нет

- BOA Intership ProgramДокумент18 страницBOA Intership ProgramAaron Joy Dominguez PutianОценок пока нет

- Advac 2Документ5 страницAdvac 2Aaron Joy Dominguez PutianОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

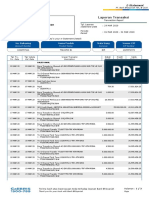

- Laporan Transaksi: No. Rekening Nama Produk Mata Uang Nomor CIFДокумент3 страницыLaporan Transaksi: No. Rekening Nama Produk Mata Uang Nomor CIFAlfiIchaОценок пока нет

- Base Tables in APДокумент6 страницBase Tables in APdevender143Оценок пока нет

- Invoice: Charge DetailsДокумент2 страницыInvoice: Charge DetailsAnna BanaОценок пока нет

- IT2021112401011404338Документ13 страницIT2021112401011404338ali aabisОценок пока нет

- Adobe Scan Mar 24, 2023Документ1 страницаAdobe Scan Mar 24, 2023SIDDHANT KUMARОценок пока нет

- Summary Notes On Regular Allowable Itemized Deductions - CompressДокумент4 страницыSummary Notes On Regular Allowable Itemized Deductions - CompressRochel Ada-olОценок пока нет

- Answer KeyДокумент4 страницыAnswer KeyDynОценок пока нет

- 1927297165Документ1 страница1927297165Ayush SrivastavОценок пока нет

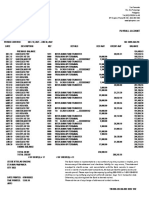

- Bpi Bank StatementДокумент1 страницаBpi Bank Statementbktsuna0201Оценок пока нет

- Literature Review On Adoption of Digital Payment SystemДокумент7 страницLiterature Review On Adoption of Digital Payment SystemNigin G KariattОценок пока нет

- Tax Invoice: Gati Kintetsu Express Private LimitedДокумент1 страницаTax Invoice: Gati Kintetsu Express Private Limitedsibesh nandiОценок пока нет

- ThirdPartyRetrieveDocument - Asp 5Документ4 страницыThirdPartyRetrieveDocument - Asp 5Elizabeth HilsonОценок пока нет

- GST Implications On Sale of Developed Plots and JDA For Plotted Development of Land CA Yashwant KasarДокумент23 страницыGST Implications On Sale of Developed Plots and JDA For Plotted Development of Land CA Yashwant KasarShashikant WadkarОценок пока нет

- Quote 2020-10-7Документ1 страницаQuote 2020-10-7Miguel CuisiaОценок пока нет

- The Institute of Chartered Accountants of Nepal: Suggested Answers of Income Tax and VATДокумент8 страницThe Institute of Chartered Accountants of Nepal: Suggested Answers of Income Tax and VATDipen AdhikariОценок пока нет

- PDFДокумент2 страницыPDFkumar Ranjan 22Оценок пока нет

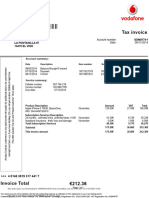

- Spain Vodavone 2 PDFДокумент1 страницаSpain Vodavone 2 PDFNext ServiceОценок пока нет

- Global Remittance:: SGD (Singapore Dollar) Is An Eligible Currency For Wire Transfers.21Документ7 страницGlobal Remittance:: SGD (Singapore Dollar) Is An Eligible Currency For Wire Transfers.21Susmita JakkinapalliОценок пока нет

- Direct Tax Laws & International Taxation Mock Test Paper SeriesДокумент11 страницDirect Tax Laws & International Taxation Mock Test Paper SeriesDeepsikha maitiОценок пока нет

- Fixedline and Broadband Services: Your Account Summary This Month'S ChargesДокумент2 страницыFixedline and Broadband Services: Your Account Summary This Month'S ChargesJeneshОценок пока нет

- Withholding Tax (Eng)Документ10 страницWithholding Tax (Eng)WN TV programsОценок пока нет

- Meter Readings For Meter ID 7751533786: Present Reading 01-02-2017 1147.11 1275.33 .168 0.92Документ1 страницаMeter Readings For Meter ID 7751533786: Present Reading 01-02-2017 1147.11 1275.33 .168 0.92Shahid MОценок пока нет

- I. General Principles Basic Concepts: 342 1 Cooley 72-73.) Article X, Sec 5, 1987 ConstitutionДокумент113 страницI. General Principles Basic Concepts: 342 1 Cooley 72-73.) Article X, Sec 5, 1987 ConstitutionRhaj Łin Kuei100% (1)

- Pay Slip For The Month of April 2018Документ1 страницаPay Slip For The Month of April 2018srini reddyОценок пока нет

- The University of Lahore: Regular Fee VoucherДокумент1 страницаThe University of Lahore: Regular Fee VoucherTalha KhanОценок пока нет

- Fees Structure 20212022 PDFДокумент3 страницыFees Structure 20212022 PDFAhmedОценок пока нет

- Ir 292Документ22 страницыIr 292samsujОценок пока нет

- Notice Pay - Amneal-Pharmaceuticals-Pvt.-Ltd.-GST-AAR-GujratДокумент7 страницNotice Pay - Amneal-Pharmaceuticals-Pvt.-Ltd.-GST-AAR-Gujratashim1Оценок пока нет

- Form Refund-Transfer Request-V180903Документ1 страницаForm Refund-Transfer Request-V180903Catarina GitaОценок пока нет

- Realme 8 (Cyber Silver, 128 GB) : Grand Total 13749.00Документ1 страницаRealme 8 (Cyber Silver, 128 GB) : Grand Total 13749.00amit sharmaОценок пока нет