Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Investment & Risk ManagementДокумент5 страницInvestment & Risk ManagementE-sabat RizviОценок пока нет

- Toyocrypto Customer Source of Wealth Declaration Form PDFДокумент2 страницыToyocrypto Customer Source of Wealth Declaration Form PDFMuhammad Amin AfifudinОценок пока нет

- Problems and Solutions in Cash FlowsДокумент5 страницProblems and Solutions in Cash Flowsitishaagrawal41100% (1)

- Activity - Capital Investment AnalysisДокумент5 страницActivity - Capital Investment AnalysisKATHRYN CLAUDETTE RESENTEОценок пока нет

- Foundations of Finance 9th Edition Keown Solutions Manual DownloadДокумент25 страницFoundations of Finance 9th Edition Keown Solutions Manual DownloadEugene Gaines100% (21)

- One Up On Wall Street: Book CondensationДокумент10 страницOne Up On Wall Street: Book CondensationAardityam SharmaОценок пока нет

- Business Research Methods: Problem Definition and The Research ProposalДокумент27 страницBusiness Research Methods: Problem Definition and The Research Proposalitishaagrawal41Оценок пока нет

- Concept of TakeoverДокумент11 страницConcept of Takeoveritishaagrawal41Оценок пока нет

- MotivesДокумент25 страницMotivesitishaagrawal41Оценок пока нет

- Merger of Reliance Industries 1Документ10 страницMerger of Reliance Industries 1itishaagrawal41Оценок пока нет

- How Merger Takes Place Between Two Companies?Документ3 страницыHow Merger Takes Place Between Two Companies?itishaagrawal41Оценок пока нет

- Business Research Methods: MeasurementДокумент18 страницBusiness Research Methods: Measurementitishaagrawal41Оценок пока нет

- Comprimise, Arrangement and Amalgamation NotesДокумент6 страницComprimise, Arrangement and Amalgamation Notesitishaagrawal41Оценок пока нет

- Chapter 1 - Introduction To Business CommunicationДокумент18 страницChapter 1 - Introduction To Business Communicationitishaagrawal41Оценок пока нет

- Experimental ResearchДокумент74 страницыExperimental Researchitishaagrawal41Оценок пока нет

- Types of Research & Research ProcessДокумент32 страницыTypes of Research & Research Processitishaagrawal41Оценок пока нет

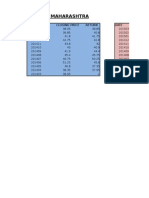

- Bank of Maharashtra: Closing Price Return DateДокумент4 страницыBank of Maharashtra: Closing Price Return Dateitishaagrawal41Оценок пока нет

- Transactions Related To Operating ActivitiesДокумент2 страницыTransactions Related To Operating Activitiesitishaagrawal41Оценок пока нет

- Chapter 9 - Preparing and Delivering PresentationsДокумент37 страницChapter 9 - Preparing and Delivering Presentationsitishaagrawal41100% (1)

- CH 4 Job AnalysisДокумент28 страницCH 4 Job Analysisitishaagrawal41Оценок пока нет

- CH 1 Brand AmbassadorsДокумент26 страницCH 1 Brand Ambassadorsitishaagrawal41Оценок пока нет

- Government Budget AndBalance of PaymentsДокумент17 страницGovernment Budget AndBalance of Paymentsitishaagrawal41Оценок пока нет

- The Introduction of Islamic Finance in MalaysiaДокумент2 страницыThe Introduction of Islamic Finance in Malaysiaafiffarhan2100% (1)

- CH 01Документ53 страницыCH 01Ismadth2918388Оценок пока нет

- Chapter 7 - An Introduction To Portfolio ManagementДокумент23 страницыChapter 7 - An Introduction To Portfolio ManagementImejah FaviОценок пока нет

- General Management ReportДокумент62 страницыGeneral Management ReportPraveen Chanpa100% (1)

- Investment Strategy CaseДокумент16 страницInvestment Strategy Caseamitgurus100% (2)

- FINE3015 2122 - CourseOutline Sem1Документ2 страницыFINE3015 2122 - CourseOutline Sem1Wang Hon YuenОценок пока нет

- JSW Steel IR 2018-19 Final PDFДокумент424 страницыJSW Steel IR 2018-19 Final PDFSweta SinhaОценок пока нет

- Dias Information FileДокумент8 страницDias Information FileLorcan BondОценок пока нет

- MC Investor Presentation VF Q3 23Документ24 страницыMC Investor Presentation VF Q3 23l91179909Оценок пока нет

- Course Syllabus InvДокумент10 страницCourse Syllabus InvMeaza BalchaОценок пока нет

- 8 Financial Literacy Lesson1Документ6 страниц8 Financial Literacy Lesson1hlmd.blogОценок пока нет

- CFO or COO or CAO or Director or Finance ExecutiveДокумент4 страницыCFO or COO or CAO or Director or Finance Executiveapi-79290895Оценок пока нет

- Roth IRA Investing Starter KitДокумент17 страницRoth IRA Investing Starter KitHuliaОценок пока нет

- IntroductiontoTechnicalAnalysisandChartingwww - Nooreshtech.co .In 2 PDFДокумент28 страницIntroductiontoTechnicalAnalysisandChartingwww - Nooreshtech.co .In 2 PDFrohitОценок пока нет

- CFI - Accounting Fact Sheet PDFДокумент1 страницаCFI - Accounting Fact Sheet PDFClaudia FilipОценок пока нет

- Solution Manual For Portfolio Construction Management and Protection 5th Edition by StrongДокумент35 страницSolution Manual For Portfolio Construction Management and Protection 5th Edition by Strongemigrate.tegumentxy6c6100% (50)

- Hiring Finance RolesДокумент1 страницаHiring Finance RolesSAKSHAM SINGHОценок пока нет

- Tesla Forecasting 2020-3Документ19 страницTesla Forecasting 2020-3Santiago Prada CruzОценок пока нет

- Chapter 2 INTEREST RATE DETERMINATION AND STRUCTUREДокумент1 страницаChapter 2 INTEREST RATE DETERMINATION AND STRUCTUREBrandon LumibaoОценок пока нет

- URC Financial Analysis 2013Документ35 страницURC Financial Analysis 2013heheheheОценок пока нет

- Reading 5 Portfolio MathematicsДокумент14 страницReading 5 Portfolio MathematicsNghia Tuan NghiaОценок пока нет

- Theories of Dividend PolicyДокумент13 страницTheories of Dividend PolicyNavneet NandaОценок пока нет

- The Following Balance Sheet Has Been Produced For Litz CorporatiДокумент1 страницаThe Following Balance Sheet Has Been Produced For Litz CorporatiAmit PandeyОценок пока нет

- 3 Objections On MusharkahДокумент3 страницы3 Objections On MusharkahAmna IrfanОценок пока нет

- BDK Engineering Industries Put LTD HubliДокумент80 страницBDK Engineering Industries Put LTD HubliRuishabh RunwalОценок пока нет