Вам также может понравиться

- EscrowДокумент5 страницEscrowAdarsh ChhajedОценок пока нет

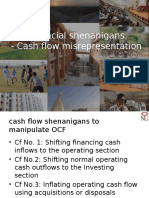

- Financial Shenanigans CashflowsДокумент19 страницFinancial Shenanigans CashflowsAdarsh ChhajedОценок пока нет

- Financial Shenanigans EMДокумент17 страницFinancial Shenanigans EMAdarsh ChhajedОценок пока нет

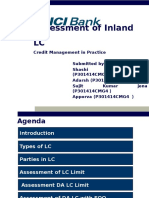

- Inland LCДокумент9 страницInland LCAdarsh ChhajedОценок пока нет

- Qis & MsodДокумент16 страницQis & MsodAdarsh Chhajed50% (2)

- Amul IndiaДокумент3 страницыAmul IndiaAdarsh ChhajedОценок пока нет

- PNBДокумент30 страницPNBAdarsh ChhajedОценок пока нет

- Financial InstrumentsДокумент26 страницFinancial InstrumentsAdarsh ChhajedОценок пока нет

- Project Cash FlowsДокумент2 страницыProject Cash FlowsAdarsh Chhajed20% (5)

- SSG GROUPДокумент22 страницыSSG GROUPAdarsh ChhajedОценок пока нет

- Future Option AnlysisДокумент18 страницFuture Option AnlysisAdarsh ChhajedОценок пока нет

- Quiz 2solutionДокумент10 страницQuiz 2solutionAdarsh ChhajedОценок пока нет

- AirAsia CaseДокумент22 страницыAirAsia CaseAdarsh Chhajed100% (1)

- Financial InstrumentsДокумент26 страницFinancial InstrumentsAdarsh ChhajedОценок пока нет

- Annualized Net Income GrowthДокумент25 страницAnnualized Net Income GrowthAdarsh Chhajed0% (2)

- Accenture A New Era in Banking Cloud ComputingДокумент20 страницAccenture A New Era in Banking Cloud ComputingAdarsh Chhajed100% (1)

- Quiz 3Документ8 страницQuiz 3Adarsh ChhajedОценок пока нет

- Ratio Analysis Questions and AnswersДокумент3 страницыRatio Analysis Questions and Answersjosh cruzОценок пока нет

- TATA 69 Annual ReportДокумент216 страницTATA 69 Annual ReportdryfruitsОценок пока нет

- Auto Parts Final SheetДокумент27 страницAuto Parts Final SheetAdarsh ChhajedОценок пока нет

- Finalquestionnaire 130722171232 Phpapp02Документ2 страницыFinalquestionnaire 130722171232 Phpapp02harmanguliani88100% (1)

- Economic & Market position before the Big Bull scam: License Raj & ScamsДокумент8 страницEconomic & Market position before the Big Bull scam: License Raj & ScamsAdarsh ChhajedОценок пока нет

- Stress Patterns in EnglishДокумент2 страницыStress Patterns in EnglishAdarsh ChhajedОценок пока нет

- Cloud Computing For Banksdoc1333Документ9 страницCloud Computing For Banksdoc1333Adarsh ChhajedОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Project Profile For Remica Woven Sack Tape Line 90MM With Hot Air Oven For 5.5 Tone - Per DayДокумент8 страницProject Profile For Remica Woven Sack Tape Line 90MM With Hot Air Oven For 5.5 Tone - Per DayShivang BhavsarОценок пока нет

- Chapter 7 in Class Practice SolutionДокумент12 страницChapter 7 in Class Practice Solution919282902Оценок пока нет

- Operating Activities:: What Are The Classification of Cash Flow?Документ5 страницOperating Activities:: What Are The Classification of Cash Flow?samm yuuОценок пока нет

- Exercises on Computation of Interest for Hire Purchase and Installment SystemsДокумент18 страницExercises on Computation of Interest for Hire Purchase and Installment SystemsHarsha Baby100% (1)

- Suspense QuestionsДокумент15 страницSuspense QuestionsChaiz MineОценок пока нет

- Chapter 3Документ24 страницыChapter 3izai vitorОценок пока нет

- Akuntansi Keuangan Lanjutan - Baker (10 E)Документ1 086 страницAkuntansi Keuangan Lanjutan - Baker (10 E)Nabila Nur IzzaОценок пока нет

- Track Software Inc ManFinДокумент28 страницTrack Software Inc ManFinLiyana Chua100% (1)

- MBA604 - Financial Reporting and AnalysisДокумент319 страницMBA604 - Financial Reporting and AnalysisShivam singhОценок пока нет

- Chapter 25 (10) Capital Investment Analysis: ObjectivesДокумент40 страницChapter 25 (10) Capital Investment Analysis: ObjectivesJames BarzoОценок пока нет

- Income Taxation - Regular Income Tax 2Документ5 страницIncome Taxation - Regular Income Tax 2Drew BanlutaОценок пока нет

- Learn Annuity Method of DepreciationДокумент3 страницыLearn Annuity Method of DepreciationKristin ByrdОценок пока нет

- Audit Planning: SGB & CДокумент17 страницAudit Planning: SGB & CMelanie SamsonaОценок пока нет

- Accounting: Paper 0452/01 Multiple ChoiceДокумент15 страницAccounting: Paper 0452/01 Multiple ChoiceItai Nigel ZembeОценок пока нет

- Contingent LiabilityДокумент4 страницыContingent LiabilityProspero Jerome IntanoОценок пока нет

- 14-Notes To The Financial Statements - UKДокумент80 страниц14-Notes To The Financial Statements - UKdana_dumitru_13Оценок пока нет

- Cebb Accounting Review Center PPT - 11.08.19Документ54 страницыCebb Accounting Review Center PPT - 11.08.19Clarissa Estolloso100% (3)

- Final DrillДокумент19 страницFinal DrillKurumi 06Оценок пока нет

- Syllabus - Ec t82 - Industrial Management and Engineering EconomicsДокумент1 страницаSyllabus - Ec t82 - Industrial Management and Engineering EconomicsPRADEEP JОценок пока нет

- St. Anthony's College Financial Accounting HomeworkДокумент12 страницSt. Anthony's College Financial Accounting HomeworkMaria Jessa HernaezОценок пока нет

- Solution Manual For Foundations of Financial Management Block Hirt Danielsen 15th EditionДокумент24 страницыSolution Manual For Foundations of Financial Management Block Hirt Danielsen 15th EditionCassandraHurstarzm100% (46)

- FAR.2950 - Interim Financial ReportingДокумент3 страницыFAR.2950 - Interim Financial ReportingEdmark LuspeОценок пока нет

- Financial StatementДокумент8 страницFinancial StatementDarwin Dionisio ClementeОценок пока нет

- Chapter 19Документ16 страницChapter 19Leen AlnussayanОценок пока нет

- Exploration For Evaluatio of Mineral ResourcesДокумент8 страницExploration For Evaluatio of Mineral ResourcesRОценок пока нет

- Taxation of Corporate IncomeДокумент22 страницыTaxation of Corporate IncomeBendyОценок пока нет

- Consolidated FS Chapter 4Документ16 страницConsolidated FS Chapter 4Charlene Bolandres100% (1)

- Glossary HHPДокумент337 страницGlossary HHPhendrysubaОценок пока нет

- Mount Moreland Hospital: Perform Financial CalculationsДокумент9 страницMount Moreland Hospital: Perform Financial CalculationsJacob Sheridan0% (1)

- Coc Level 3 4TH RoundДокумент15 страницCoc Level 3 4TH Roundsolomon asfawОценок пока нет