Вам также может понравиться

- Leasing: An OverviewДокумент18 страницLeasing: An OverviewNeha GoyalОценок пока нет

- Leases Slides - FinalДокумент34 страницыLeases Slides - FinalAnonymous n3n1Ae100% (1)

- Finama LeasingДокумент34 страницыFinama LeasingLoren Rosaria100% (1)

- Accounting For LeasesДокумент12 страницAccounting For LeasesvladsteinarminОценок пока нет

- As 19Документ23 страницыAs 19soumya_2688Оценок пока нет

- RMK Akm 2-CH 21Документ14 страницRMK Akm 2-CH 21Rio Capitano0% (1)

- Chapter 18 LeasingДокумент4 страницыChapter 18 LeasingTham Ru JieОценок пока нет

- LeasingДокумент17 страницLeasingvineet ranjanОценок пока нет

- 25 LeasingДокумент9 страниц25 Leasingddrechsler9Оценок пока нет

- Lease FinancingДокумент10 страницLease FinancingNishant SharmaОценок пока нет

- IAS AND IFRS Short NotesДокумент37 страницIAS AND IFRS Short NotesughaniОценок пока нет

- A Note On Comdisco - S Lease AccountingДокумент25 страницA Note On Comdisco - S Lease AccountingHussain HaidryОценок пока нет

- Lease and Intermediate Term Financing - Chapter 19Документ34 страницыLease and Intermediate Term Financing - Chapter 19MASPAK100% (1)

- Chapter 18 LEASES - Winter 2022 Canvas VersionДокумент63 страницыChapter 18 LEASES - Winter 2022 Canvas VersionJared ScottОценок пока нет

- Leasing ACF PresentДокумент22 страницыLeasing ACF PresentHameed WesabiОценок пока нет

- FRS 17Документ2 страницыFRS 17Derkoon LinОценок пока нет

- BFS - Leasing in IndiaДокумент29 страницBFS - Leasing in IndiaBhawana Choudhary50% (2)

- Ifrs 16 LeasesДокумент70 страницIfrs 16 Leasessikute kamongwaОценок пока нет

- Chapter 8 Leases Part 2Документ14 страницChapter 8 Leases Part 2maria isabellaОценок пока нет

- Accounting For Leases Fra 2012Документ8 страницAccounting For Leases Fra 2012Srishti ShawОценок пока нет

- Intro To Leasing NoteДокумент5 страницIntro To Leasing NoteZain FaheemОценок пока нет

- FARC Lesson3 (Lease)Документ18 страницFARC Lesson3 (Lease)SlicebearОценок пока нет

- ACCT201 Handout (Topic 6) - LiabilitiesДокумент36 страницACCT201 Handout (Topic 6) - LiabilitiesElvin TanОценок пока нет

- Marketing of Financial Services Leasing 1 PPT FinalДокумент17 страницMarketing of Financial Services Leasing 1 PPT Finaljohn_muellorОценок пока нет

- Corporate Reporting - SPRING 2021 ACC-344 Assignment # 03 Submitted ToДокумент5 страницCorporate Reporting - SPRING 2021 ACC-344 Assignment # 03 Submitted ToAliyya TaimurОценок пока нет

- Leases: International Accounting Standards (IAS 17)Документ13 страницLeases: International Accounting Standards (IAS 17)ashfakkadriОценок пока нет

- (Lecture 5) - Other Investment Appraisal DecisionsДокумент21 страница(Lecture 5) - Other Investment Appraisal DecisionsAjay Kumar Takiar100% (1)

- 21 Accounting For LeasesДокумент28 страниц21 Accounting For LeasesWisnuadi Sony PradanaОценок пока нет

- Relative Resource Manager 2Документ61 страницаRelative Resource Manager 2hannah8985Оценок пока нет

- Accounting For Leases IFRS 16 Vs IAS 17Документ20 страницAccounting For Leases IFRS 16 Vs IAS 17Obisike Emezi100% (2)

- Leasing As A Financing AlternativeДокумент35 страницLeasing As A Financing AlternativeHamza Najmi100% (1)

- CH.5 LeaseДокумент63 страницыCH.5 LeaseLidia SamuelОценок пока нет

- Accounting Standard 19Документ12 страницAccounting Standard 19Kamal HassanОценок пока нет

- Hybrid Financing: Preferred Stock, Leasing, Warrants, and ConvertiblesДокумент165 страницHybrid Financing: Preferred Stock, Leasing, Warrants, and ConvertiblesJewel Mae MercadoОценок пока нет

- CF Session 19-Lease FinancingДокумент9 страницCF Session 19-Lease FinancingRitika MehtaОценок пока нет

- SLFRS 16 - Leasing: Please Note: LKAS 17: LEASING (Will Not Be Questioned) - For Additional Information OnlyДокумент7 страницSLFRS 16 - Leasing: Please Note: LKAS 17: LEASING (Will Not Be Questioned) - For Additional Information Onlyganraj100% (1)

- Presented By:-Mohit Nath Mba 3 SemДокумент15 страницPresented By:-Mohit Nath Mba 3 SemMohit NathОценок пока нет

- Lease, HP, Project FinanceДокумент30 страницLease, HP, Project FinanceSneha Ashok100% (1)

- Capital Lease Vs Operating Lease PDFДокумент6 страницCapital Lease Vs Operating Lease PDFHassleBustОценок пока нет

- Chapter 12. LeasesДокумент24 страницыChapter 12. LeasesАйбар КарабековОценок пока нет

- Chapter 12 Lessee AccountingДокумент26 страницChapter 12 Lessee Accountingchesca marie penarandaОценок пока нет

- 26 As19Документ14 страниц26 As19Selvi balanОценок пока нет

- Chapter 2 - Additional Accounting Analysis - SVДокумент9 страницChapter 2 - Additional Accounting Analysis - SVK59 Le Nhat ThanhОценок пока нет

- Accounting For Leases and Hire Purchase Contract Final - DocxmaryДокумент41 страницаAccounting For Leases and Hire Purchase Contract Final - DocxmarySoledad Perez100% (1)

- Far 46 60Документ27 страницFar 46 60GuadzОценок пока нет

- Topic 1 Accounting For LeasesДокумент59 страницTopic 1 Accounting For LeasesAtira Shamsul Bahari100% (1)

- Lease Accounting: Dr.T.P.Ghosh Professor, MDI, GurgaonДокумент20 страницLease Accounting: Dr.T.P.Ghosh Professor, MDI, Gurgaonkmillat100% (1)

- Leasing (Compatibility Mode)Документ19 страницLeasing (Compatibility Mode)Sameer ThakurОценок пока нет

- Banking and NBFC - Module 5 NBFC Produtcs Lending BasedДокумент89 страницBanking and NBFC - Module 5 NBFC Produtcs Lending Basednandhakumark152Оценок пока нет

- Lease FinancingДокумент13 страницLease FinancingJay KishanОценок пока нет

- Leasing: Prepared by The FacultyДокумент17 страницLeasing: Prepared by The FacultymimiОценок пока нет

- Lease FinancingДокумент16 страницLease Financingparekhrahul9988% (8)

- Non Banking Financial Institutions: by Sudev Jyothisi FN-92 Scms-CochinДокумент18 страницNon Banking Financial Institutions: by Sudev Jyothisi FN-92 Scms-CochinSUDEVJYOTHISIОценок пока нет

- Lease 2nd SessionДокумент18 страницLease 2nd SessionMohammad AnikОценок пока нет

- (LA9) Lessee Accounting - RewrittenДокумент9 страниц(LA9) Lessee Accounting - RewrittenTyra LouwrensОценок пока нет

- Ch22 LeasingДокумент30 страницCh22 LeasingsaadsaaidОценок пока нет

- Winning the Office Leasing Game: Essential Strategies for Negotiating Your Office Lease Like an ExpertОт EverandWinning the Office Leasing Game: Essential Strategies for Negotiating Your Office Lease Like an ExpertОценок пока нет

- Project TerminationДокумент13 страницProject TerminationsakshiОценок пока нет

- Export Promotion Zone/Special Economic Zone (Epz/Sez) & Export Oriented Units (EOU)Документ17 страницExport Promotion Zone/Special Economic Zone (Epz/Sez) & Export Oriented Units (EOU)sakshiОценок пока нет

- Provisions Relating To Default in Furnishing Returns Under GSTДокумент2 страницыProvisions Relating To Default in Furnishing Returns Under GSTsakshiОценок пока нет

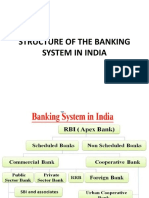

- Banking System in IndiaДокумент18 страницBanking System in IndiasakshiОценок пока нет

- Consumer Protection Act: Tushar Swami (609) Reshma Patil (610) Sarvesh Raj Singh (611) Sunket Anand PantДокумент41 страницаConsumer Protection Act: Tushar Swami (609) Reshma Patil (610) Sarvesh Raj Singh (611) Sunket Anand PantsakshiОценок пока нет

- Unit - 3 - Acma CMC 653Документ192 страницыUnit - 3 - Acma CMC 653sakshiОценок пока нет

- Unit - 1 - Acma CMC 653Документ128 страницUnit - 1 - Acma CMC 653sakshiОценок пока нет

- Meaning & Characteristics of A CompanyДокумент19 страницMeaning & Characteristics of A Companysakshi100% (2)

- Derivatives & Risk ManagementДокумент62 страницыDerivatives & Risk ManagementsakshiОценок пока нет

- Option Valuation ModelsДокумент37 страницOption Valuation ModelssakshiОценок пока нет

- Financial InstitutionsДокумент15 страницFinancial InstitutionssakshiОценок пока нет

- Articles of AssociationДокумент21 страницаArticles of AssociationsakshiОценок пока нет

- 3a. Financial - Sector - ReformsДокумент23 страницы3a. Financial - Sector - ReformssakshiОценок пока нет

- Tire Repair-Shop-Business-Plan-ExampleДокумент30 страницTire Repair-Shop-Business-Plan-ExampleEstherlee ThompsonОценок пока нет

- BS As On 23-09-2023Документ28 страницBS As On 23-09-2023Farooq MaqboolОценок пока нет

- Rec Center News Sun City West Dec 2009Документ27 страницRec Center News Sun City West Dec 2009Del Webb Sun Cities MuseumОценок пока нет

- Ican SyllabusДокумент82 страницыIcan SyllabusOlufunso EkundayoОценок пока нет

- Andritz Financial Report 2019 en DataДокумент173 страницыAndritz Financial Report 2019 en DatamОценок пока нет

- Global Corporation TCWДокумент6 страницGlobal Corporation TCWFred WilsonОценок пока нет

- Summer Internship Programme 2018-19: National Aluminum Company Limited NalcoДокумент59 страницSummer Internship Programme 2018-19: National Aluminum Company Limited Nalcoanon_849519161Оценок пока нет

- Tally Ledger List in Excel Format - Teachoo PDFДокумент6 страницTally Ledger List in Excel Format - Teachoo PDFAMIT KUMAR DUTTA100% (1)

- Accounting Changes - IFRS 16Документ17 страницAccounting Changes - IFRS 16imranОценок пока нет

- LG HH - Ir Presentation 2012 - 1Q - EngДокумент8 страницLG HH - Ir Presentation 2012 - 1Q - EngSam_Ha_Оценок пока нет

- Intermacc Depreciation, Depletion, Revaluation, and Impairment Prelec WaДокумент1 страницаIntermacc Depreciation, Depletion, Revaluation, and Impairment Prelec WaClarice Awa-aoОценок пока нет

- 1 Financial Detective Berau FinalДокумент4 страницы1 Financial Detective Berau Finalal ajiОценок пока нет

- C35 - MFRS 138 IntangiblesДокумент28 страницC35 - MFRS 138 IntangibleskkОценок пока нет

- Lease (Lessee)Документ7 страницLease (Lessee)Angel Queen Marino SamoragaОценок пока нет

- Financial Analysis Honda Atlas Cars Pakistan 1Документ6 страницFinancial Analysis Honda Atlas Cars Pakistan 126342634Оценок пока нет

- Income Statement CDE, Inc. For The Year Ended December 31, 2021Документ3 страницыIncome Statement CDE, Inc. For The Year Ended December 31, 2021Ma. Lou Erika BALITEОценок пока нет

- Corporate Finance I176 Xid-3384732 1Документ8 страницCorporate Finance I176 Xid-3384732 1kashualОценок пока нет

- Zbornik M2016 PDFДокумент354 страницыZbornik M2016 PDFPredrag PetrovicОценок пока нет

- Depreciation (Chapter 27) : - Lies On Type of Assets InvolvedДокумент4 страницыDepreciation (Chapter 27) : - Lies On Type of Assets InvolvedaaaОценок пока нет

- MGT101 - Financial Accounting - UnSolved - MID Term Paper - 02Документ7 страницMGT101 - Financial Accounting - UnSolved - MID Term Paper - 02osamaОценок пока нет

- Accounts Assignment 2Документ12 страницAccounts Assignment 2shoaiba167% (3)

- Intermediate Accounting 2 Syllabus 2015Документ5 страницIntermediate Accounting 2 Syllabus 2015Altea ZaimanОценок пока нет

- Audited Financial Results March 31, 2019 Reliance Jio Infocomm LimitedДокумент9 страницAudited Financial Results March 31, 2019 Reliance Jio Infocomm LimitedKajal Gupta0% (1)

- Unit - II - Analysis of Financial StatementsДокумент54 страницыUnit - II - Analysis of Financial StatementsPRERNA PANDEYОценок пока нет

- Charts of AccountsДокумент2 страницыCharts of AccountsNur ika PratiwiОценок пока нет

- Cash Management ProjectДокумент32 страницыCash Management ProjectGaurav Rane100% (1)

- Chapter 1 Business Combinations - Part 1Документ22 страницыChapter 1 Business Combinations - Part 1Jane GavinoОценок пока нет

- Q2 18 19Документ4 страницыQ2 18 19Surya SudheerОценок пока нет

- Its Earning That Count SummaryДокумент115 страницIts Earning That Count SummaryTheda VeldaОценок пока нет

- Chap 003Документ38 страницChap 003MichaelFraserОценок пока нет