Вам также может понравиться

- Auditing Revenue CycleДокумент29 страницAuditing Revenue CycleDaniel Tadeja100% (1)

- Ch09 - Auditing Revenue CycleДокумент29 страницCh09 - Auditing Revenue CyclerclagunaОценок пока нет

- Audit The Revenue CycleДокумент26 страницAudit The Revenue CycleJosephine CristajuneОценок пока нет

- Chapter 9 Audit of Revenue CycleДокумент29 страницChapter 9 Audit of Revenue CycleRizel C. MontanteОценок пока нет

- Auditing The Revenue Cycle: IT Auditing & Assurance, 2e, Hall & SingletonДокумент29 страницAuditing The Revenue Cycle: IT Auditing & Assurance, 2e, Hall & SingletonKath OОценок пока нет

- Script COMACДокумент3 страницыScript COMACRany Meldrenz FloresОценок пока нет

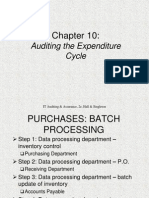

- Auditing The Expenditure Cycle: IT Auditing & Assurance, 2e, Hall & SingletonДокумент26 страницAuditing The Expenditure Cycle: IT Auditing & Assurance, 2e, Hall & SingletonrclagunaОценок пока нет

- Chapter 10 SummaryДокумент12 страницChapter 10 SummaryWendelyn TutorОценок пока нет

- Test of Controls in The Expenditure or DisbursementДокумент16 страницTest of Controls in The Expenditure or DisbursementDebbie Cervancia DimapilisОценок пока нет

- Auditing in A ComputerДокумент4 страницыAuditing in A Computerkevior2Оценок пока нет

- CH 04Документ44 страницыCH 04Winoah HubaldeОценок пока нет

- Procure To PayДокумент14 страницProcure To PaymeegunОценок пока нет

- Accounting Information System CH10 Lecture NoteДокумент20 страницAccounting Information System CH10 Lecture NoteJiaxin ChenОценок пока нет

- SCM - Proses PemesananДокумент44 страницыSCM - Proses PemesananArief HidayatОценок пока нет

- Audit of The Inventory and Warehousing CycleДокумент59 страницAudit of The Inventory and Warehousing CycleSweet EmmeОценок пока нет

- Module 05 - Accounting and Information SystemsДокумент6 страницModule 05 - Accounting and Information SystemsKaye BabadillaОценок пока нет

- Accounting Information Systems, 6: Edition James A. HallДокумент40 страницAccounting Information Systems, 6: Edition James A. HallDianne NolascoОценок пока нет

- Auditing The Expenditure CycleДокумент20 страницAuditing The Expenditure CycleClarice Ilustre GuintibanoОценок пока нет

- The Revenue Cycle: Group 1Документ43 страницыThe Revenue Cycle: Group 1Ratih PratiwiОценок пока нет

- The Revenue Cycle: Accounts Receivable DR Sales CR Cost of Goods Sold DR Inventory CR Cash DR Accounts Receivable CRДокумент26 страницThe Revenue Cycle: Accounts Receivable DR Sales CR Cost of Goods Sold DR Inventory CR Cash DR Accounts Receivable CRJyle Mareinette ManiagoОценок пока нет

- Auditing in A Computer-Based EnvironmentДокумент4 страницыAuditing in A Computer-Based Environmentshahzad arshadОценок пока нет

- Chapter 6-Application Controls NotesДокумент5 страницChapter 6-Application Controls NotesDaisy ContinenteОценок пока нет

- Fi ApДокумент91 страницаFi Aprohitmandhania100% (1)

- The Revenue CycleДокумент44 страницыThe Revenue CycleColeen Mae Rapanut ParaynoОценок пока нет

- Chapter 5 PPT (AIS - James Hall)Документ10 страницChapter 5 PPT (AIS - James Hall)Nur-aima Mortaba50% (2)

- Audit - System Audit - CIS Audit - IT AuditДокумент5 страницAudit - System Audit - CIS Audit - IT AuditBHAVYAN AGARWALОценок пока нет

- Financial AccountingДокумент4 страницыFinancial Accountinggaurang_12Оценок пока нет

- Application ControlsДокумент34 страницыApplication Controlsteacup21Оценок пока нет

- Sap Fi Accounts PayableДокумент91 страницаSap Fi Accounts PayableAnonymous 2AYQKfPn5oОценок пока нет

- 10 Naw To Be Material AccountingДокумент24 страницы10 Naw To Be Material AccountingsivasivasapОценок пока нет

- Ch10 - Auditing Expenditure CycleДокумент21 страницаCh10 - Auditing Expenditure CycleRizka FurqorinaОценок пока нет

- Auditing The Revenue CycleДокумент9 страницAuditing The Revenue CycleWendelyn TutorОценок пока нет

- Empowering Users With Self-Service: March 7, 2005Документ81 страницаEmpowering Users With Self-Service: March 7, 2005hanharinОценок пока нет

- Auditing Expenditure CycleДокумент21 страницаAuditing Expenditure Cycleerny2412Оценок пока нет

- SAP Accounts Payable AP003Документ70 страницSAP Accounts Payable AP003venkidas100% (2)

- AIS6e.ab - Az ch04Документ46 страницAIS6e.ab - Az ch04Francis Ryan PorquezОценок пока нет

- Audit II CH 4 Nov 2020Документ10 страницAudit II CH 4 Nov 2020padmОценок пока нет

- PRIORITY Short DescriptionДокумент5 страницPRIORITY Short DescriptionLuiza HudeaОценок пока нет

- Auditing The Revenue CycleДокумент7 страницAuditing The Revenue CycleJECEL CABGRIGAОценок пока нет

- Prof BullinaДокумент2 страницыProf Bullinamjc24Оценок пока нет

- Business Activities AND Transaction ProcessingДокумент45 страницBusiness Activities AND Transaction ProcessingMuhammad Syahir Mat SharifОценок пока нет

- Sales Order Management Process For Sap Terp10Документ1 страницаSales Order Management Process For Sap Terp10pbtg100% (1)

- Revenue CycleДокумент46 страницRevenue CycleConstantine TandayuОценок пока нет

- Auditing The Expenditure Cycle SummaryДокумент7 страницAuditing The Expenditure Cycle SummaryHimaya Sa KalipayОценок пока нет

- Procurement GlossaryДокумент12 страницProcurement GlossaryMichael Schmitt100% (2)

- Types of Business Information SystemsДокумент24 страницыTypes of Business Information Systemsvinit PatidarОценок пока нет

- CH 02Документ39 страницCH 02enamislamОценок пока нет

- Evaluate and Authorize Payment Requests ModuleДокумент28 страницEvaluate and Authorize Payment Requests ModuleTegene Tesfaye100% (1)

- Dextserv Focus ProfileДокумент17 страницDextserv Focus ProfileMerwin NaveenОценок пока нет

- Bestow ERP General 2Документ14 страницBestow ERP General 2M. MUBASHARОценок пока нет

- MGT 1272 Management Information System Mid-Term NotesДокумент10 страницMGT 1272 Management Information System Mid-Term NotesYvonne ChenОценок пока нет

- CH 08Документ37 страницCH 08France SerdeniaОценок пока нет

- Chapter 5 Expenditure Cycle Part 1Документ33 страницыChapter 5 Expenditure Cycle Part 1KRIS ANNE SAMUDIO100% (1)

- AP Process Automation WP 2284450Документ10 страницAP Process Automation WP 2284450HeroanОценок пока нет

- Auditing Expenditure CycleДокумент7 страницAuditing Expenditure CycleHannaj May De GuzmanОценок пока нет

- Substantive Tests of Expenditure Cycle Accounts Substantive TestsДокумент3 страницыSubstantive Tests of Expenditure Cycle Accounts Substantive TestsJuvelyn RedutaОценок пока нет

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsОт EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsРейтинг: 5 из 5 звезд5/5 (1)

- The Controller's Function: The Work of the Managerial AccountantОт EverandThe Controller's Function: The Work of the Managerial AccountantОценок пока нет

- Alarm Clock ManualДокумент7 страницAlarm Clock ManualjОценок пока нет

- Dca 101 (Fundamentals of Computer)Документ29 страницDca 101 (Fundamentals of Computer)LalfakzualaОценок пока нет

- Updated Schedule Even Semester - Utu 2010-2011Документ41 страницаUpdated Schedule Even Semester - Utu 2010-2011Utkarsh PalОценок пока нет

- Pizza Management SystemДокумент9 страницPizza Management SystemZafer AhmedОценок пока нет

- Operating SystemsДокумент18 страницOperating SystemspksstejaОценок пока нет

- Essay Prompt: "Today's Engineers Face The Same Challenges As Those of Previous Generations." Do You Agree? If So Why? If Not, Why NotДокумент3 страницыEssay Prompt: "Today's Engineers Face The Same Challenges As Those of Previous Generations." Do You Agree? If So Why? If Not, Why NotJaypeeCañizaresGatmaitanIIОценок пока нет

- COMPUTEK Company ProfileДокумент6 страницCOMPUTEK Company ProfileAhmed hafezОценок пока нет

- The Discussion Over Artificial IntelligenceДокумент2 страницыThe Discussion Over Artificial IntelligenceEmmy LoversОценок пока нет

- Ktu B.Tech Cse S4 Note: Operating SystemsДокумент18 страницKtu B.Tech Cse S4 Note: Operating SystemsDfgОценок пока нет

- DCA SyllabusДокумент8 страницDCA SyllabusTheRHKapadiaCollege50% (2)

- Computer Skills: SoftwareДокумент13 страницComputer Skills: Softwaresmart centerОценок пока нет

- 2.high Level Language and Low Level LanguageДокумент14 страниц2.high Level Language and Low Level LanguagekshitijbiОценок пока нет

- Empowerment Technologies Module 1Документ24 страницыEmpowerment Technologies Module 1Krestel Meriam OvilleОценок пока нет

- The DREAM 6800 Computer: Australia Personal ComputersДокумент1 страницаThe DREAM 6800 Computer: Australia Personal ComputersHernan BenitesОценок пока нет

- Edited Sop DeepДокумент2 страницыEdited Sop Deepjayraj daveОценок пока нет

- Big CPU Big DataДокумент424 страницыBig CPU Big DataKountОценок пока нет

- 20461C Setup GuideДокумент17 страниц20461C Setup Guidejediael.pj0% (1)

- William Cooper - Behold A Pale Horse - CitationДокумент2 страницыWilliam Cooper - Behold A Pale Horse - CitationGodIsTruth67% (3)

- Samar Colleges In1Документ9 страницSamar Colleges In1Jonathan CayatОценок пока нет

- Navman5500 ManualДокумент42 страницыNavman5500 ManualMaryam232Оценок пока нет

- Computer Repair and MaintenanceДокумент24 страницыComputer Repair and MaintenanceWilma Arenas Montes100% (1)

- Lecture 1 - CSE - Microprocessor and Assembly LanguageДокумент21 страницаLecture 1 - CSE - Microprocessor and Assembly LanguagefaridulОценок пока нет

- TESDA-OP-CO-01-F11 TESDA-OP-CO-01-F11 (Rev. No. 00-03/08/17) (Rev. No. 00-03/08/17)Документ31 страницаTESDA-OP-CO-01-F11 TESDA-OP-CO-01-F11 (Rev. No. 00-03/08/17) (Rev. No. 00-03/08/17)Erika Mae SatunaОценок пока нет

- Philippine Identification System Act Republic Act No 11055Документ4 страницыPhilippine Identification System Act Republic Act No 11055Joey Cereno100% (1)

- Full Unit 1 Notes-KCS-102Документ44 страницыFull Unit 1 Notes-KCS-102Sonu zehen001Оценок пока нет

- Computer Skills For Resume 2018Документ6 страницComputer Skills For Resume 2018idyuurvcf100% (2)

- Olimpiada de Limba Engleza Pentru GimnaziuДокумент4 страницыOlimpiada de Limba Engleza Pentru GimnaziuAnonymous 8D1IlUM5Y100% (1)

- ComputerДокумент6 страницComputerredix pereiraОценок пока нет

- ST2195 Programming For Data ScienceДокумент11 страницST2195 Programming For Data Sciencenatali tedjojuwonoОценок пока нет

- JmusicДокумент9 страницJmusicjesdayОценок пока нет