Вам также может понравиться

- Home Budget TemplateДокумент2 страницыHome Budget TemplatemanojОценок пока нет

- Monthly Budget Template: Sheet1Документ2 страницыMonthly Budget Template: Sheet1Rufino Gerard Moreno IIIОценок пока нет

- Guia de Prevencion FodДокумент16 страницGuia de Prevencion FodMibal Mibal MibalОценок пока нет

- Zero TouchДокумент1 страницаZero TouchDelilah Murao MorlaОценок пока нет

- Visitor Safety and Agreement 20121Документ20 страницVisitor Safety and Agreement 20121Rahmat BudimanОценок пока нет

- 1-Quality ConceptsДокумент9 страниц1-Quality ConceptsSehabom GeberhiwotОценок пока нет

- Badger Knowledge Base Metal Bellows Expansion Joint HandbookДокумент24 страницыBadger Knowledge Base Metal Bellows Expansion Joint Handbookli100% (1)

- Accountable Plan - Excel TemplateДокумент9 страницAccountable Plan - Excel Templateelnara safronovaОценок пока нет

- Presentation On Lean Manufacturing: Course Title: Ergonomics and Productivity Engineering Sessional Course Code: IPE 3202Документ26 страницPresentation On Lean Manufacturing: Course Title: Ergonomics and Productivity Engineering Sessional Course Code: IPE 3202Ayman Sajjad AkashОценок пока нет

- God of AllДокумент9 страницGod of AllRaphael Dean Vitug DesturaОценок пока нет

- Liquid or Liquidity or Acid Test or Quick RatioДокумент2 страницыLiquid or Liquidity or Acid Test or Quick RatioJohn LoukrakpamОценок пока нет

- Be Advised, The Template Workbooks and Worksheets Are Not Protected. Overtyping Any Data May Remove ItДокумент6 страницBe Advised, The Template Workbooks and Worksheets Are Not Protected. Overtyping Any Data May Remove ItSalman KhalidОценок пока нет

- Personal Budget SpreadsheetДокумент8 страницPersonal Budget SpreadsheetWahyudi SantosoОценок пока нет

- Behavioral ScienceДокумент38 страницBehavioral ScienceAyushGuptaОценок пока нет

- Activity Completion Report TemplateДокумент13 страницActivity Completion Report TemplateMa Nida Ada BaldelobarОценок пока нет

- Quality AwardsДокумент8 страницQuality AwardsManoj BansiwalОценок пока нет

- Two Examples of TQM: - Texas TelecomДокумент11 страницTwo Examples of TQM: - Texas Telecomshru_87Оценок пока нет

- Theory of Production CostДокумент17 страницTheory of Production CostDherya AgarwalОценок пока нет

- Procedure TemplateДокумент3 страницыProcedure TemplateBoby SaputraОценок пока нет

- JIT at Oak HillsДокумент2 страницыJIT at Oak HillsKyle Sims0% (1)

- Introduction To Quality: Teaching NotesДокумент29 страницIntroduction To Quality: Teaching NotesKlarence Tan100% (1)

- Capital Structure of FMCG, IT, Power and TelecomДокумент20 страницCapital Structure of FMCG, IT, Power and TelecomPayal Homagni Mondal0% (1)

- Credit and Torts 1Документ22 страницыCredit and Torts 1chrisОценок пока нет

- Example of Business PlanДокумент15 страницExample of Business PlanDexter CudiamatОценок пока нет

- 7qc Tools ExplanationДокумент64 страницы7qc Tools ExplanationRajОценок пока нет

- Personal Budget SpreadsheetДокумент5 страницPersonal Budget SpreadsheetpareshbaldotaОценок пока нет

- HousekeepingДокумент25 страницHousekeepingFrancis ToonОценок пока нет

- FMEA With NotationsДокумент2 страницыFMEA With Notationstcalhoun1285100% (2)

- Pareto Chart Exercise1Документ6 страницPareto Chart Exercise1Walt PrystajОценок пока нет

- Linear Programming ApplicationДокумент8 страницLinear Programming ApplicationMartin AndreanОценок пока нет

- Thus The Objectives of Production Management Are Reflected inДокумент4 страницыThus The Objectives of Production Management Are Reflected inCubeОценок пока нет

- Manufacturing - Quiz WeygantДокумент26 страницManufacturing - Quiz WeygantAlta SophiaОценок пока нет

- Impact of Storage Devices On The EnviromentДокумент4 страницыImpact of Storage Devices On The Enviromentalfredsamsele2100% (1)

- Principle of Economics LU3: ElasticityДокумент47 страницPrinciple of Economics LU3: ElasticitySHOBANA96Оценок пока нет

- Hazard RecognitionДокумент27 страницHazard RecognitiondoremiredoОценок пока нет

- Analytical Tools For Quality, Six Sigma and Continuous ImprovementДокумент25 страницAnalytical Tools For Quality, Six Sigma and Continuous ImprovementHajiMasthanSabОценок пока нет

- Fyp Feasibility Study: 1.1. Types of Feasibilty StudyДокумент3 страницыFyp Feasibility Study: 1.1. Types of Feasibilty StudyAli IqbalОценок пока нет

- Market FeasibilityДокумент73 страницыMarket FeasibilityNiloy SarkarОценок пока нет

- Transportation Chapter 3Документ17 страницTransportation Chapter 3Tuan NguyenОценок пока нет

- Total Productivity and Quality ManagementДокумент30 страницTotal Productivity and Quality ManagementNirmalОценок пока нет

- Certification ProcessДокумент1 страницаCertification ProcessAnonymous 1GK9Hxp5YKОценок пока нет

- Problem Solving With QC Tools: AspireДокумент54 страницыProblem Solving With QC Tools: AspireRajib ChatterjeeОценок пока нет

- 6 Feasibility Assessment ToolДокумент5 страниц6 Feasibility Assessment Toolalibaba1888Оценок пока нет

- You Exec - Root Cause Analysis FreeДокумент6 страницYou Exec - Root Cause Analysis FreeOlivier RachoinОценок пока нет

- Evolution of Quality ManagementДокумент2 страницыEvolution of Quality ManagementHussain Aparambil100% (1)

- Break-Even Analysis PDFДокумент4 страницыBreak-Even Analysis PDFirvin5de5los5riosОценок пока нет

- 5s (Workplace Organization) Implementation: Confidential and Proprietary - © 2008 Kellogg Na CompanyДокумент33 страницы5s (Workplace Organization) Implementation: Confidential and Proprietary - © 2008 Kellogg Na CompanyAko Lang PohОценок пока нет

- Swot Analysis of The PubДокумент1 страницаSwot Analysis of The PubNg Kah WeeОценок пока нет

- Hisrich Entrepreneurship 11e Chap010Документ11 страницHisrich Entrepreneurship 11e Chap010swapnilОценок пока нет

- Lean in Automobile ServiceДокумент9 страницLean in Automobile ServiceRovil KumarОценок пока нет

- Home Affordability Calculator: IncomeДокумент5 страницHome Affordability Calculator: IncomeRomi RobertoОценок пока нет

- Feasibility Analysis: The Beauty ClubДокумент15 страницFeasibility Analysis: The Beauty ClubGwyneth Ü ElipanioОценок пока нет

- Operations ManagementДокумент44 страницыOperations Managementnonu dhimanОценок пока нет

- Welding Safety TrainingДокумент23 страницыWelding Safety TrainingTinna Puspita Marita SariОценок пока нет

- Wages and Salary AdministrationДокумент47 страницWages and Salary Administrationsaha apurvaОценок пока нет

- Tactical Decision MakingДокумент2 страницыTactical Decision MakingMay AugustusОценок пока нет

- Mortgage BasicsДокумент111 страницMortgage Basicsmercury820Оценок пока нет

- Real Estate Finance and Investments: Weeks 10-11 Mortgages IДокумент50 страницReal Estate Finance and Investments: Weeks 10-11 Mortgages IJiayu JinОценок пока нет

- Definition of Estate: General Warranty DeedДокумент5 страницDefinition of Estate: General Warranty DeedMamun RashidОценок пока нет

- Essay On MortgagesДокумент2 страницыEssay On MortgagesViorel Mihai Mitrana100% (1)

- Jahangir AlamДокумент2 страницыJahangir AlamMohammad ImranОценок пока нет

- Curriculum Vita of Md. Jowel Miah: Mailing AddressДокумент3 страницыCurriculum Vita of Md. Jowel Miah: Mailing AddressMohammad ImranОценок пока нет

- Resume OF Md. Monowar Hossain: Contact AddressДокумент2 страницыResume OF Md. Monowar Hossain: Contact AddressMohammad ImranОценок пока нет

- IMPACT Whats in AnameДокумент5 страницIMPACT Whats in AnameMohammad ImranОценок пока нет

- CPA Australia: Helping Filipinos Build Exceptional Finance CareersДокумент3 страницыCPA Australia: Helping Filipinos Build Exceptional Finance CareersHazzelle DumaleОценок пока нет

- Sap C TSCM62 64 PDFДокумент24 страницыSap C TSCM62 64 PDFjpcupcupin23100% (2)

- Metrobank v. Rural Bank of Gerona (2010)Документ8 страницMetrobank v. Rural Bank of Gerona (2010)Karina GarciaОценок пока нет

- JVC AP BR100 v0.1Документ71 страницаJVC AP BR100 v0.1Gopalakrishna DevulapalliОценок пока нет

- GBLДокумент33 страницыGBLTonton ReyesОценок пока нет

- Dissertation Report FormatДокумент53 страницыDissertation Report FormatSonal ThakurОценок пока нет

- Midterm Exam Global Stumble PDFДокумент2 страницыMidterm Exam Global Stumble PDFBim BimОценок пока нет

- (Claim Signature Form) : Business Name of EmployerДокумент2 страницы(Claim Signature Form) : Business Name of EmployerVirgilioОценок пока нет

- Audit of ReceivablesДокумент9 страницAudit of Receivablesmissy100% (2)

- Bizmanualz Accounting Policies and Procedures SampleДокумент10 страницBizmanualz Accounting Policies and Procedures Sampleallukazoldyck100% (1)

- Declaration of TrustДокумент2 страницыDeclaration of Trustkyra_kae100% (15)

- Foreign CurrencyДокумент4 страницыForeign CurrencyDyheeОценок пока нет

- Blueprint of Banking SectorДокумент33 страницыBlueprint of Banking SectormayankОценок пока нет

- Sadiq Hoi PDFДокумент2 страницыSadiq Hoi PDFHafiz Shoaib MaqsoodОценок пока нет

- PNB Annual Report 2017-18Документ176 страницPNB Annual Report 2017-18robinvrgs88Оценок пока нет

- Self-Registers Bank Account @cashout - KingdomДокумент16 страницSelf-Registers Bank Account @cashout - Kingdomradohi6352100% (1)

- The ScribeДокумент6 страницThe ScribesrilaksvelacheryОценок пока нет

- 33 KVДокумент258 страниц33 KVAMOL HIRULKARОценок пока нет

- The Memo'Документ2 страницыThe Memo'Anonymous GZ9IDkОценок пока нет

- Chyna's Dreamland Chase SeptemberДокумент5 страницChyna's Dreamland Chase SeptemberJonathan Seagull LivingstonОценок пока нет

- PRESENTATION On Merchant BankingДокумент12 страницPRESENTATION On Merchant Bankingsarthak1826Оценок пока нет

- Project Report Submitted in Partial Fulfillment of The Requirement For The Award of The Degree of 3 SemesterДокумент116 страницProject Report Submitted in Partial Fulfillment of The Requirement For The Award of The Degree of 3 SemesterMayank PalОценок пока нет

- Multi Page PDFДокумент164 страницыMulti Page PDFAung Zaw HtweОценок пока нет

- GST Challan PDFДокумент2 страницыGST Challan PDFSmarttОценок пока нет

- Hedge YeДокумент25 страницHedge YeZerohedgeОценок пока нет

- Case Study Grameen BankДокумент7 страницCase Study Grameen BankkatnavОценок пока нет

- Final Project 2017-18Документ3 страницыFinal Project 2017-18Monali rautОценок пока нет

- Banking Industry in The Age of FraudДокумент9 страницBanking Industry in The Age of FraudShailendra Nath GodsoraОценок пока нет

- Landmark Cases in The Law of Contract Order FormДокумент4 страницыLandmark Cases in The Law of Contract Order Formshahbaz_malbari_bballb13Оценок пока нет

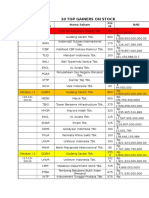

- 10 Top Gainers On Stock: Bulan/Min Ggu Kode Saham Nama Saham Poi NT NABДокумент6 страниц10 Top Gainers On Stock: Bulan/Min Ggu Kode Saham Nama Saham Poi NT NABFajRin WiCaksonoОценок пока нет