Вам также может понравиться

- ACCT1111 Chapter 7 LectureДокумент62 страницыACCT1111 Chapter 7 LectureWky JimОценок пока нет

- AFM Chapter 7 Depreciation MergeДокумент99 страницAFM Chapter 7 Depreciation MergeSarah Shahnaz IlmaОценок пока нет

- Class 8Документ48 страницClass 8NkОценок пока нет

- Week 7 Ch10 Plant Assets Natural Resources and Intangible AssetsДокумент67 страницWeek 7 Ch10 Plant Assets Natural Resources and Intangible Assetspegagus98Оценок пока нет

- ACCO ch10Документ80 страницACCO ch10Samar BarakehОценок пока нет

- Financial Accounting 4Th Edition Kemp Solutions Manual Full Chapter PDFДокумент68 страницFinancial Accounting 4Th Edition Kemp Solutions Manual Full Chapter PDFhauesperanzad0ybz100% (9)

- Introduction To Financial Accounting: Long-Lived AssetsДокумент58 страницIntroduction To Financial Accounting: Long-Lived AssetsShubham Kaushik100% (1)

- AccHor 7e CH 01Документ32 страницыAccHor 7e CH 01Muh BilalОценок пока нет

- CH 10Документ80 страницCH 10BayaderОценок пока нет

- Chapter 10 1Документ63 страницыChapter 10 1HEM CHEAОценок пока нет

- Plant Assets, Natural Assets, Intangible Asset (Chapter 9)Документ73 страницыPlant Assets, Natural Assets, Intangible Asset (Chapter 9)Tio Suyanto100% (1)

- Non-Current Assets (PPE & Intangible Assets & Financial Investments)Документ67 страницNon-Current Assets (PPE & Intangible Assets & Financial Investments)Andreea Cristina DiaconuОценок пока нет

- Slide ACT102 ACT102 Slide 01Документ33 страницыSlide ACT102 ACT102 Slide 01Muhammad ArdiansyahОценок пока нет

- Financial Accounting Chapter 09Документ74 страницыFinancial Accounting Chapter 09Rakhma RamadhaniОценок пока нет

- Financial Accounting MBA Depreciation)Документ41 страницаFinancial Accounting MBA Depreciation)Ehtisham Zafar Bhatti100% (2)

- AccHor 7e CH 18Документ22 страницыAccHor 7e CH 18Muh BilalОценок пока нет

- Plant Assets, Natural Resources, and Intangible Assets: Accounting Principles, Ninth EditionДокумент26 страницPlant Assets, Natural Resources, and Intangible Assets: Accounting Principles, Ninth EditionJ PОценок пока нет

- Slide Chương 8Документ80 страницSlide Chương 8anhtuand.hrcneuОценок пока нет

- Chapter 10Документ50 страницChapter 10duy blaОценок пока нет

- Plant Assets Natural Resources and Intangible AsДокумент59 страницPlant Assets Natural Resources and Intangible AsxunaidОценок пока нет

- CH 10Документ63 страницыCH 10Baby NinjaОценок пока нет

- Chapter 10 Week 5Документ35 страницChapter 10 Week 5jadogОценок пока нет

- Intermediate Accounting Vol 1 Canadian 3rd Edition Lo Solutions ManualДокумент45 страницIntermediate Accounting Vol 1 Canadian 3rd Edition Lo Solutions Manualconatusimploded.bi6q100% (22)

- 3310-Ch 8-End of Chapter solutions-STДокумент35 страниц3310-Ch 8-End of Chapter solutions-STArvind ManoОценок пока нет

- Engineering Economics Lecture 8 PDFДокумент45 страницEngineering Economics Lecture 8 PDFNavinPaudelОценок пока нет

- Roperty, Lant, ND Quipment: P P A EДокумент70 страницRoperty, Lant, ND Quipment: P P A ETrek ApostolОценок пока нет

- CH 10Документ64 страницыCH 10anmonegamingОценок пока нет

- Finance and Budgeting For MaintenanceДокумент51 страницаFinance and Budgeting For Maintenanceapi-3732848100% (1)

- 2023 Chapter Two Accounting For Plant AssetДокумент59 страниц2023 Chapter Two Accounting For Plant Assetwudnehkassahun97Оценок пока нет

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeДокумент98 страницPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegeBertoniОценок пока нет

- Fixed Assets and Intangible Assets 10: Click To Edit Master Title StyleДокумент32 страницыFixed Assets and Intangible Assets 10: Click To Edit Master Title Stylerina.asmara asmaraОценок пока нет

- Calculating Changeovers High CostДокумент24 страницыCalculating Changeovers High Costjohnrhenry100% (4)

- Financial Accounting: Fixed & Intangible AssetsДокумент26 страницFinancial Accounting: Fixed & Intangible AssetsAstri RirinОценок пока нет

- 157 35295 EY121 2013 1 2 1 Chap010Документ46 страниц157 35295 EY121 2013 1 2 1 Chap010alaamabood6Оценок пока нет

- Capital Investment Decisions and The Time Value of MoneyДокумент63 страницыCapital Investment Decisions and The Time Value of MoneyAwoke AdaneОценок пока нет

- Corporations: Retained Earnings and The Income StatementДокумент40 страницCorporations: Retained Earnings and The Income Statementmustafa_33Оценок пока нет

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeДокумент54 страницыPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegePetersonОценок пока нет

- Aktiva Tetap-DepresiasiДокумент49 страницAktiva Tetap-DepresiasiAmmy IskandarОценок пока нет

- Bab10 Pengantar AkuntansiДокумент101 страницаBab10 Pengantar AkuntansiRonald SajutiОценок пока нет

- CH 10Документ55 страницCH 10KHANH Du NgocОценок пока нет

- CH 10Документ81 страницаCH 10Putu DenyОценок пока нет

- CH 10Документ83 страницыCH 10Thư TrầnОценок пока нет

- Bab 9 IndonesiaДокумент31 страницаBab 9 IndonesiaMarco PangerapanОценок пока нет

- Accounting For DepreciationДокумент55 страницAccounting For DepreciationraghavОценок пока нет

- PPE and Intangible Assets: Acquisition and Disposition: Student Learning OutcomesДокумент10 страницPPE and Intangible Assets: Acquisition and Disposition: Student Learning OutcomesElie DiabОценок пока нет

- Long Lived AssetsДокумент51 страницаLong Lived AssetsAshraf GeorgeОценок пока нет

- Chapter 10 PPTДокумент48 страницChapter 10 PPTkjw 2Оценок пока нет

- Chapter TwoДокумент48 страницChapter Twonewaybeyene5Оценок пока нет

- AccHor 7e CH 14Документ22 страницыAccHor 7e CH 14Muh BilalОценок пока нет

- Financial Accounting Session on Depreciation of Property, Plant and Equipment (PPEДокумент33 страницыFinancial Accounting Session on Depreciation of Property, Plant and Equipment (PPEJohn DoeОценок пока нет

- Week 12 - Capex and DepreciationДокумент55 страницWeek 12 - Capex and DepreciationajenggОценок пока нет

- AC Chapter 9Документ19 страницAC Chapter 9Minh AnhОценок пока нет

- Plant Assets, Natural Resources, and Intangible Assets: Accounting Principles, Ninth EditionДокумент21 страницаPlant Assets, Natural Resources, and Intangible Assets: Accounting Principles, Ninth EditionMehedi HasanОценок пока нет

- Plant Assets, Natural Resources, and Intangible AssetsДокумент92 страницыPlant Assets, Natural Resources, and Intangible AssetsKabeer QureshiОценок пока нет

- ACT 201 Chapter 10Документ56 страницACT 201 Chapter 10Lutfun Nesa Aysha 1831892630Оценок пока нет

- Plant Assets, Natural Resources, and IntangiblesДокумент16 страницPlant Assets, Natural Resources, and IntangiblesEla PelariОценок пока нет

- Handout 3 - Plant Assets, Natural Resources, and Intangible AssetsДокумент81 страницаHandout 3 - Plant Assets, Natural Resources, and Intangible Assetsyoussef abdellatifОценок пока нет

- Long-Term Assets Skyline College Lecture NotesДокумент54 страницыLong-Term Assets Skyline College Lecture Noteskalley minogОценок пока нет

- Plant Assets, Natural Resources, Intangible AssetsДокумент80 страницPlant Assets, Natural Resources, Intangible Assetsaderagaming 2719Оценок пока нет

- Financial Accounting: Naveed AnjumДокумент15 страницFinancial Accounting: Naveed Anjummustafa_33Оценок пока нет

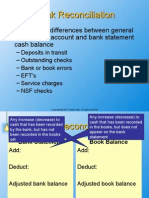

- Bank Reconciliation Bank ReconciliationДокумент9 страницBank Reconciliation Bank Reconciliationmustafa_33Оценок пока нет

- PartnershipДокумент63 страницыPartnershipmustafa_33100% (1)

- Thinking About Communication: Chapter#1Документ20 страницThinking About Communication: Chapter#1mustafa_33Оценок пока нет

- Corporations: Retained Earnings and The Income StatementДокумент40 страницCorporations: Retained Earnings and The Income Statementmustafa_33Оценок пока нет

- Financial Analysis of Reliance Industries Limited: Arindam BarmanДокумент109 страницFinancial Analysis of Reliance Industries Limited: Arindam Barmananon_645298319100% (1)

- Divine Aura Final Project 12Документ20 страницDivine Aura Final Project 12Usva SaleemОценок пока нет

- Feltham 1995Документ44 страницыFeltham 1995vickyzaoОценок пока нет

- Tata Steel financial analysisДокумент12 страницTata Steel financial analysisSubhasish mahapatraОценок пока нет

- Quiz On FUNDA ABM 2Документ2 страницыQuiz On FUNDA ABM 2Baby Irish Estares Marcelo100% (1)

- Small Business ManagementДокумент30 страницSmall Business ManagementVinamra PatilОценок пока нет

- BritanniaДокумент4 страницыBritanniaHiral JoshiОценок пока нет

- Prelim - PART 2Документ6 страницPrelim - PART 2Dan RyanОценок пока нет

- Marketing Plan for Carrot Pasta RestaurantДокумент31 страницаMarketing Plan for Carrot Pasta RestaurantTed BeroyaОценок пока нет

- Horizontal Groups (2021)Документ5 страницHorizontal Groups (2021)Tawanda Tatenda HerbertОценок пока нет

- Unit 4 Cash Flow StatementДокумент26 страницUnit 4 Cash Flow Statementjatin4verma-2Оценок пока нет

- Basics of Accounting Till Balance SheetДокумент39 страницBasics of Accounting Till Balance Sheetjayti desaiОценок пока нет

- KPMG 2018 Banks IfsДокумент221 страницаKPMG 2018 Banks Ifschakas100% (1)

- Word Note The Body Shop International PLC 2001: An Introduction To Financial ModelingДокумент9 страницWord Note The Body Shop International PLC 2001: An Introduction To Financial Modelingalka murarka100% (2)

- Course: Advanced Accounting: Chapter 2: Partnership Liquidation and IncorporationДокумент4 страницыCourse: Advanced Accounting: Chapter 2: Partnership Liquidation and Incorporationmohamed dahir AbdirahmaanОценок пока нет

- Cash Flow FormulaДокумент2 страницыCash Flow FormulaSubhas ChettriОценок пока нет

- Corporate Liquidation Answer SheetДокумент4 страницыCorporate Liquidation Answer SheetsatyaОценок пока нет

- Solution Manufacturing Prob. GRT ManufacturingДокумент15 страницSolution Manufacturing Prob. GRT ManufacturingCarmi FeceroОценок пока нет

- Intermediate Accounting 17th Edition Kieso Solutions ManualДокумент22 страницыIntermediate Accounting 17th Edition Kieso Solutions Manualdilysiristtes5100% (29)

- Kohls Balance Sheet 2015Документ2 страницыKohls Balance Sheet 2015Mathew VisarraОценок пока нет

- WCM Toyota STДокумент18 страницWCM Toyota STferoz khanОценок пока нет

- 04 IFRS FinancialStatementsДокумент88 страниц04 IFRS FinancialStatementsVinay SinghОценок пока нет

- KIP REAL ESTATE 1Q2022 INTERIM REPORTДокумент17 страницKIP REAL ESTATE 1Q2022 INTERIM REPORTseeme55runОценок пока нет

- A Levels Accounting Notes PDFДокумент207 страницA Levels Accounting Notes PDFLeanne Teh100% (4)

- P1 Part4.2Документ8 страницP1 Part4.2Minie KimОценок пока нет

- Leveraged Buyout LBO Model For Private Equity FirmsДокумент22 страницыLeveraged Buyout LBO Model For Private Equity Firmsgesona4324Оценок пока нет

- IFRS16 - Lease Standard SAP Solution Through Real Estate Management - SAP BlogsДокумент12 страницIFRS16 - Lease Standard SAP Solution Through Real Estate Management - SAP BlogsFranki Giassi MeurerОценок пока нет

- Answer Sheet: Mindanao State UniversityДокумент14 страницAnswer Sheet: Mindanao State UniversityNermeen C. AlapaОценок пока нет

- ACCT2014 Final Exam 2021-2022 - K.Ashman v2Документ9 страницACCT2014 Final Exam 2021-2022 - K.Ashman v2Christina StephensonОценок пока нет

- Accounting Assignment Sample SolutionsДокумент20 страницAccounting Assignment Sample SolutionsHebrew JohnsonОценок пока нет