Вам также может понравиться

- Managerial Accounting Concepts and Principles: Irwin/Mcgraw-HillДокумент29 страницManagerial Accounting Concepts and Principles: Irwin/Mcgraw-HillAmrik SinghОценок пока нет

- Bachelor of Accounting ACC731 Cost & Management Accounting 1Документ39 страницBachelor of Accounting ACC731 Cost & Management Accounting 1Gideon SancyОценок пока нет

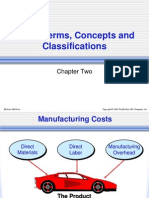

- Costs Terms, Concepts and Classifications: Chapter TwoДокумент78 страницCosts Terms, Concepts and Classifications: Chapter TwoJesus Alberto MarquezОценок пока нет

- Managerial Accounting and Cost ConceptsДокумент85 страницManagerial Accounting and Cost ConceptsCatherine DelRayОценок пока нет

- Chap 018Документ43 страницыChap 018josephselo100% (1)

- Costs Terms, Concepts and Classifications: Chapter TwoДокумент34 страницыCosts Terms, Concepts and Classifications: Chapter TwounobtainableОценок пока нет

- CH 2 - Cost Terms, Concepts, and ClassificationsДокумент78 страницCH 2 - Cost Terms, Concepts, and ClassificationsLimChanpatiya67% (3)

- Industrial Management IPE 481: Tanveer Hossain Bhuiyan Assistant Professor, Dept. of IPE BuetДокумент63 страницыIndustrial Management IPE 481: Tanveer Hossain Bhuiyan Assistant Professor, Dept. of IPE BuetNaimul Hoque ShuvoОценок пока нет

- Basic Cost Management Concepts and Accounting For Mass Customization OperationsДокумент55 страницBasic Cost Management Concepts and Accounting For Mass Customization OperationsBelajar MembacaОценок пока нет

- 110-W2-3-Cost concept-chp02-STДокумент85 страниц110-W2-3-Cost concept-chp02-STmargaret mariaОценок пока нет

- Chap 001Документ67 страницChap 001Scott Baiocchi100% (1)

- Chap 002 Cost ConceptsДокумент85 страницChap 002 Cost ConceptsLata KaushikОценок пока нет

- Managerial Accounting Session 1Документ15 страницManagerial Accounting Session 1cathlenerosetalibgosОценок пока нет

- Introduction To Managerial Accounting and Cost ConceptsДокумент91 страницаIntroduction To Managerial Accounting and Cost ConceptsRithik VisuОценок пока нет

- Chapter 16, MAДокумент54 страницыChapter 16, MAye yintОценок пока нет

- Cost and Managerial Accounting BasicsДокумент59 страницCost and Managerial Accounting BasicsGlenPalmerОценок пока нет

- Cost Classifications and Income StatementДокумент50 страницCost Classifications and Income StatementGovinda Gde Phillips39Оценок пока нет

- Managerial Accounting and Cost Concepts: Solutions To QuestionsДокумент13 страницManagerial Accounting and Cost Concepts: Solutions To QuestionsGera MatsОценок пока нет

- Management Accounting: A Business Partner: Lecture # 2Документ15 страницManagement Accounting: A Business Partner: Lecture # 2amnaОценок пока нет

- Cost Concepts 05032023 095733pmДокумент51 страницаCost Concepts 05032023 095733pmnida amanОценок пока нет

- Cost Management Concepts and ClassificationsДокумент47 страницCost Management Concepts and ClassificationsAmrik SinghОценок пока нет

- Chap 016Документ24 страницыChap 016Amrik SinghОценок пока нет

- CMA - 1-Introduction To CMAДокумент35 страницCMA - 1-Introduction To CMAIrtaza AhsanОценок пока нет

- Product Costing: Job and Process OperationsДокумент62 страницыProduct Costing: Job and Process OperationsJackОценок пока нет

- Managerial Accounting: Tool For Business Decision Making Third EditionДокумент56 страницManagerial Accounting: Tool For Business Decision Making Third Editionএ.বি.এস. আশিকОценок пока нет

- Review ch.1 2Документ21 страницаReview ch.1 2Nguyễn Thị Hồng YếnОценок пока нет

- Colegio de Dagupan: Institute of Graduate SchoolДокумент22 страницыColegio de Dagupan: Institute of Graduate SchoolCampbell HezekiahОценок пока нет

- Chapter 1 - Cost Term, Concept and ClassificationДокумент55 страницChapter 1 - Cost Term, Concept and ClassificationMolla Shoyeb Uddin MithuОценок пока нет

- Cost Control & Cost ReductionsДокумент92 страницыCost Control & Cost ReductionsAniketh Upadrasta100% (3)

- CM017812 Assignment 2Документ6 страницCM017812 Assignment 2Maneejan LeebumrungОценок пока нет

- Chapter Two: Cost Terms, Concepts and ClassificationsДокумент72 страницыChapter Two: Cost Terms, Concepts and ClassificationsYuvaraj SubramaniamОценок пока нет

- Chapter XVII - Operations Management Managing Quality Efficiency and Responsiveness To CustomersДокумент21 страницаChapter XVII - Operations Management Managing Quality Efficiency and Responsiveness To CustomersDrashti DewaniОценок пока нет

- Chap 2 Basic Cost Management Concepts and Accounting For Mass Customization OperationsДокумент15 страницChap 2 Basic Cost Management Concepts and Accounting For Mass Customization OperationsMarklorenz SumpayОценок пока нет

- Cost Accounting: Click To Edit Master Subtitle StyleДокумент34 страницыCost Accounting: Click To Edit Master Subtitle StyleWajiha MansoorОценок пока нет

- Chapter 1 - Introduction To Cost AccountingДокумент6 страницChapter 1 - Introduction To Cost AccountingJaira DiazОценок пока нет

- Cost Concepts and ClassificationsДокумент12 страницCost Concepts and ClassificationsnidaОценок пока нет

- Cost Management Concepts and Accounting for Mass Customization OperationsДокумент4 страницыCost Management Concepts and Accounting for Mass Customization OperationsNalynCasОценок пока нет

- Costs Terms, Concepts and Classifications: Chapter TwoДокумент23 страницыCosts Terms, Concepts and Classifications: Chapter TwokorpseeОценок пока нет

- Managerial Accounting For Managers 2nd Edition Noreen Solutions ManualДокумент25 страницManagerial Accounting For Managers 2nd Edition Noreen Solutions ManualRobertPerkinsqmjk100% (63)

- Actual Costing Excel PDFДокумент35 страницActual Costing Excel PDFJeckaОценок пока нет

- Managerial Accounting: Tool For Business Decision MakingДокумент28 страницManagerial Accounting: Tool For Business Decision MakingKeziah Eldene VilloraОценок пока нет

- Project Accounting and FM ch2Документ31 страницаProject Accounting and FM ch2Nesri YayaОценок пока нет

- Managerial Accounting and CostДокумент19 страницManagerial Accounting and CostIqra MughalОценок пока нет

- Job Order Costing Systems DesignДокумент24 страницыJob Order Costing Systems DesignSonali Jagath100% (1)

- Full Download Managerial Accounting For Managers 2nd Edition Noreen Solutions ManualДокумент35 страницFull Download Managerial Accounting For Managers 2nd Edition Noreen Solutions Manuallinderleafeulah100% (33)

- COST ACCOUNTING AND CONTROL DISCUSSIONДокумент5 страницCOST ACCOUNTING AND CONTROL DISCUSSIONkakimog738Оценок пока нет

- Cost Accounting: Swiss Business SchoolДокумент149 страницCost Accounting: Swiss Business SchoolMyriam Elaoun100% (1)

- Acct 202 Ch1Документ24 страницыAcct 202 Ch1Hieu DamОценок пока нет

- Ch.19 Managerial Accounting: Chapter Learning ObjectiveДокумент11 страницCh.19 Managerial Accounting: Chapter Learning ObjectiveIntan ParamithaОценок пока нет

- Introduction To Management AccountingДокумент51 страницаIntroduction To Management AccountingnikkinikkzОценок пока нет

- Chapter 19Документ51 страницаChapter 19Yasir MehmoodОценок пока нет

- Managerial Accounting and Cost ConceptsДокумент67 страницManagerial Accounting and Cost ConceptsTristan AdrianОценок пока нет

- ACCT 102 Management Accounting Lecture 5, 6 & 7Документ77 страницACCT 102 Management Accounting Lecture 5, 6 & 7ngan321Оценок пока нет

- E. Product Costs Eventually Affect Both The Balance Sheet and The Income Statement. 10Документ5 страницE. Product Costs Eventually Affect Both The Balance Sheet and The Income Statement. 10L LОценок пока нет

- Cost Terms, Concepts, and ClassificationsДокумент33 страницыCost Terms, Concepts, and ClassificationsKlub Matematika SMAОценок пока нет

- Practical Guide To Production Planning & Control [Revised Edition]От EverandPractical Guide To Production Planning & Control [Revised Edition]Рейтинг: 1 из 5 звезд1/5 (1)

- A Study of the Supply Chain and Financial Parameters of a Small BusinessОт EverandA Study of the Supply Chain and Financial Parameters of a Small BusinessОценок пока нет

- Manufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesОт EverandManufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesРейтинг: 4.5 из 5 звезд4.5/5 (3)

- Profit PlanningДокумент32 страницыProfit PlanningSandra LangОценок пока нет

- Style in Technical WritingДокумент30 страницStyle in Technical WritingSandra LangОценок пока нет

- CH 04Документ35 страницCH 04Ferdinand MacolОценок пока нет

- Financial Environments Specifically Institutions: Ronil John GarganianДокумент11 страницFinancial Environments Specifically Institutions: Ronil John GarganianSandra LangОценок пока нет

- Samsung: Company ProfileДокумент2 страницыSamsung: Company ProfileSandra LangОценок пока нет

- Overall Audit Plan and Program - Arens-Beasley-ElderДокумент39 страницOverall Audit Plan and Program - Arens-Beasley-ElderFerdinand MacolОценок пока нет

- Audit Program - Logical SecurityДокумент16 страницAudit Program - Logical SecuritySandra Lang100% (1)

- Overall Audit Plan and Program - Arens-Beasley-ElderДокумент39 страницOverall Audit Plan and Program - Arens-Beasley-ElderFerdinand MacolОценок пока нет

- Audit Program For Fixed AssetДокумент4 страницыAudit Program For Fixed AssetSandra Lang100% (1)

- Pricing Decisions and Cost Management QuestionsДокумент14 страницPricing Decisions and Cost Management QuestionsZaid Al-rakhesОценок пока нет

- Business Economics HomeworkДокумент18 страницBusiness Economics HomeworkFatur Mulya MuisОценок пока нет

- How Understanding Cultural Differences Can Brew Success in ChinaДокумент5 страницHow Understanding Cultural Differences Can Brew Success in Chinakimthoa113Оценок пока нет

- Quiz 4A-CДокумент4 страницыQuiz 4A-CHannah KrishramОценок пока нет

- SynopsisFormat Antra PitchДокумент2 страницыSynopsisFormat Antra PitchKavit ThakkarОценок пока нет

- Illinois IPI (2006 Edition) - 30.10 and 30.11 With Notes On UseДокумент3 страницыIllinois IPI (2006 Edition) - 30.10 and 30.11 With Notes On UseJohn CovertОценок пока нет

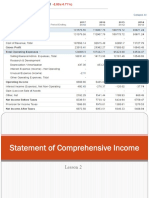

- Lesson 2 Statement of Comprehensive IncomeДокумент23 страницыLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- Jurnal MarketingДокумент25 страницJurnal MarketingDian Octavia HandayaniОценок пока нет

- GHCL Limited - : 1 P - (FaxДокумент30 страницGHCL Limited - : 1 P - (FaxShyam SunderОценок пока нет

- Project Report On Hyundai Santro For MarketingДокумент41 страницаProject Report On Hyundai Santro For MarketingHarshad Patel33% (3)

- TQMДокумент8 страницTQMMeena SinghОценок пока нет

- 2 Sem - 5 UnitДокумент23 страницы2 Sem - 5 Unitmonish bОценок пока нет

- Forex Basics: Participants, Rates, PositionsДокумент13 страницForex Basics: Participants, Rates, PositionsGia KhánhОценок пока нет

- Asia Brewery DescriptionДокумент2 страницыAsia Brewery Descriptionchalyn100% (2)

- Amul Grp2Документ6 страницAmul Grp2Harsha AnkareddyОценок пока нет

- Business Cycles Gp1 by Professor & Lawyer Puttu Guru PrasadДокумент31 страницаBusiness Cycles Gp1 by Professor & Lawyer Puttu Guru PrasadPUTTU GURU PRASAD SENGUNTHA MUDALIARОценок пока нет

- FIB Maths Chapter 6Документ9 страницFIB Maths Chapter 6VerrelyОценок пока нет

- An Introduction To International Economics: Chapter 3: The Standard Trade ModelДокумент30 страницAn Introduction To International Economics: Chapter 3: The Standard Trade ModelJustine Jireh PerezОценок пока нет

- The End of The Bretton Woods SystemДокумент2 страницыThe End of The Bretton Woods SystemSteffie CarvalhoОценок пока нет

- Chapter 6Документ14 страницChapter 6euwilla100% (1)

- Business Level Strategies for Competitive AdvantageДокумент22 страницыBusiness Level Strategies for Competitive Advantagedivyansh varshneyОценок пока нет

- Competitive Analysis of Le Sucre Lab's Chocolate DreamcakeДокумент17 страницCompetitive Analysis of Le Sucre Lab's Chocolate DreamcakeEnzy CremaОценок пока нет

- 6 Asset Pricing ModelsДокумент18 страниц6 Asset Pricing ModelsUtkarsh BhalodeОценок пока нет

- Risk and Return: Past and PrologueДокумент39 страницRisk and Return: Past and ProloguerrОценок пока нет

- RMC 1-2019 PDFДокумент1 страницаRMC 1-2019 PDFJhenny Ann P. SalemОценок пока нет

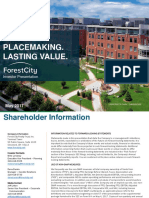

- May 2017 Investor Presentation Forest City Realty TrustДокумент63 страницыMay 2017 Investor Presentation Forest City Realty TrustNorman OderОценок пока нет

- Summary of Chapter 15Документ3 страницыSummary of Chapter 15merlinОценок пока нет

- Test AnswersДокумент9 страницTest AnswersKriti Wadhwa100% (1)

- Bakery Project Start-Up Business PlanДокумент68 страницBakery Project Start-Up Business PlanAbenet Ajeme94% (16)

- Contract Management PDFДокумент332 страницыContract Management PDFtmhoangvna100% (1)

![Practical Guide To Production Planning & Control [Revised Edition]](https://imgv2-2-f.scribdassets.com/img/word_document/235162742/149x198/2a816df8c8/1709920378?v=1)