Вам также может понравиться

- Underwriting in LICДокумент42 страницыUnderwriting in LICKanishk Gupta100% (1)

- Nilgai Foods-Case On Territory Allocation and DesignДокумент2 страницыNilgai Foods-Case On Territory Allocation and Designsupraket sahayОценок пока нет

- Kiran Mazumdar Shaw - EthosДокумент9 страницKiran Mazumdar Shaw - EthosSiddesh AttavarОценок пока нет

- Cadbury Brand Study Group 10Документ14 страницCadbury Brand Study Group 10Vaibhav WadhwaОценок пока нет

- The Quid Pro QuoДокумент5 страницThe Quid Pro QuoNadella HemanthОценок пока нет

- Imc FinalДокумент43 страницыImc Finalmanoj_yadav_9100% (1)

- Mouth WashДокумент7 страницMouth WashHana HarisОценок пока нет

- Testbank: Chapter 12 Global Strategy and The Multinational CorporationДокумент7 страницTestbank: Chapter 12 Global Strategy and The Multinational CorporationSanket Sourav BalОценок пока нет

- Vertu: Nokia's Luxury Mobile Phone For The Urban RichДокумент6 страницVertu: Nokia's Luxury Mobile Phone For The Urban RichSHAHJAHAN KHATOON Student, Jaipuria LucknowОценок пока нет

- Icici Lombard General InsuranceДокумент86 страницIcici Lombard General InsuranceNik AroraОценок пока нет

- Listerine Mouthwash: By, Group 5Документ12 страницListerine Mouthwash: By, Group 5tinkigtytyuyОценок пока нет

- Varun Nagar PresentationДокумент12 страницVarun Nagar Presentationug8Оценок пока нет

- Optimize supply chain management for Wills LifestyleДокумент7 страницOptimize supply chain management for Wills LifestyleagarwalharshalОценок пока нет

- Intelligent Automation: - A Boon For The Insurance IndustryДокумент13 страницIntelligent Automation: - A Boon For The Insurance IndustryRudolf MonterrОценок пока нет

- ITC Market AnalysisДокумент8 страницITC Market AnalysisAshish Dung Dung100% (1)

- ICICI Lombard Project ReportДокумент92 страницыICICI Lombard Project ReportShweta SawantОценок пока нет

- Ceipal MarqueДокумент4 страницыCeipal MarqueAman PandeyОценок пока нет

- Itc LTDДокумент56 страницItc LTDRakesh Kolasani Naidu100% (1)

- Vodafone-Hutch M & AДокумент12 страницVodafone-Hutch M & AKapil BhagavatulaОценок пока нет

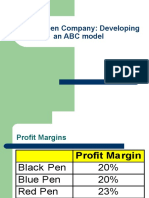

- Classic Pen Company: Developing An ABC ModelДокумент22 страницыClassic Pen Company: Developing An ABC Modeljk kumarОценок пока нет

- Whole Foods Market Case 2009Документ28 страницWhole Foods Market Case 2009Uqaila MirzaОценок пока нет

- Cottle Taylor PresenationДокумент10 страницCottle Taylor PresenationDipesh JainОценок пока нет

- Ar09 BioconДокумент153 страницыAr09 Bioconchandra12345678Оценок пока нет

- Interrobang Season 6 Case Challenge - Defining B Natural's Brand Strategy & PositioningДокумент9 страницInterrobang Season 6 Case Challenge - Defining B Natural's Brand Strategy & PositioningNaveen TegarОценок пока нет

- Case AnalysisДокумент3 страницыCase AnalysissrirockОценок пока нет

- SDM Assignment 2 Vishal 1262Документ2 страницыSDM Assignment 2 Vishal 1262MANAS OLIОценок пока нет

- ITC Ltd. Economic-Industry-Company Analysis ReportДокумент14 страницITC Ltd. Economic-Industry-Company Analysis Reportkirti sabranОценок пока нет

- Types of Interdental Aids and Cleaning MethodsДокумент160 страницTypes of Interdental Aids and Cleaning MethodsDeepeka PrabhakarОценок пока нет

- Complete Insurance Icici Lombard ProjectДокумент59 страницComplete Insurance Icici Lombard ProjectOmkar ChavanОценок пока нет

- Recession in IndiaДокумент16 страницRecession in Indiasonuka98% (63)

- Koito Case UploadДокумент11 страницKoito Case UploadJurjen van der WerfОценок пока нет

- Summer Internship Project-Sudhanshu Sharma (PGDM 2009-11,40103)Документ62 страницыSummer Internship Project-Sudhanshu Sharma (PGDM 2009-11,40103)subhashghosh72Оценок пока нет

- ITC Interrobang Season 9 HR Case Challenge - The Changing ParadigmДокумент6 страницITC Interrobang Season 9 HR Case Challenge - The Changing ParadigmVaibhavОценок пока нет

- Wills Lifestyle - Group 3Документ5 страницWills Lifestyle - Group 3Utkarsh PrasadОценок пока нет

- Service Triangle of ByjusДокумент1 страницаService Triangle of ByjusVircio FintechОценок пока нет

- Comparative Profit & Loss and Balance Sheet Analysis of BioconДокумент12 страницComparative Profit & Loss and Balance Sheet Analysis of BioconNipun KothariОценок пока нет

- ITC Interrobang Season 4 SCM Case Challenge BrochureДокумент7 страницITC Interrobang Season 4 SCM Case Challenge BrochureDurai BalajiОценок пока нет

- Determining Pay RaiseДокумент3 страницыDetermining Pay Raiseakash mohanОценок пока нет

- ITC Interrobang Case Challenge 2011 - Bingo! Mad AnglesДокумент8 страницITC Interrobang Case Challenge 2011 - Bingo! Mad AnglesSourav NandiОценок пока нет

- Target Niche Market for Clean Edge Razor LaunchДокумент7 страницTarget Niche Market for Clean Edge Razor LaunchRyan SheikhОценок пока нет

- Understanding Derivatives MarketsДокумент92 страницыUnderstanding Derivatives MarketsSauravОценок пока нет

- Icici Scam CGДокумент6 страницIcici Scam CG201812058 imtnagОценок пока нет

- CH 2ansДокумент3 страницыCH 2ansab khОценок пока нет

- Tata Motors Annual Report AnalysisДокумент55 страницTata Motors Annual Report AnalysisPrathibha TiwariОценок пока нет

- Entrepreneurship Project: Biocon: Submitted To-Submitted by - Dr. Abha Aman Bajaj 237/15 Bcom LLB (Hons.)Документ20 страницEntrepreneurship Project: Biocon: Submitted To-Submitted by - Dr. Abha Aman Bajaj 237/15 Bcom LLB (Hons.)Aman BajajОценок пока нет

- Universal - Health - Coverage - in - India - A Long Road AheadДокумент8 страницUniversal - Health - Coverage - in - India - A Long Road AheadrenjithОценок пока нет

- Replacing El Poderoso - Guiding QuestionsДокумент1 страницаReplacing El Poderoso - Guiding QuestionsAmir GhasdiОценок пока нет

- Biocon:: Launching A New Cancer Drug in IndiaДокумент10 страницBiocon:: Launching A New Cancer Drug in IndiaDeepak Jangid0% (1)

- SIPДокумент49 страницSIPdeeОценок пока нет

- Nestle 4Ps Challenger 2019 PDFДокумент12 страницNestle 4Ps Challenger 2019 PDFSHASHANK CHOUDHARY 22Оценок пока нет

- ITC Interrobang Season 2 Case Challenge - Bingo! Mad AnglesДокумент8 страницITC Interrobang Season 2 Case Challenge - Bingo! Mad AnglesAshish JainОценок пока нет

- Sales and Distribution Channel of ITC SA PDFДокумент12 страницSales and Distribution Channel of ITC SA PDFRomil SailotОценок пока нет

- SectionA Group 3 RAOBDA ReportДокумент7 страницSectionA Group 3 RAOBDA ReportIsha ChaudharyОценок пока нет

- Sun Life Financial and Indian Economic Surge: Case Analysis - International BusinessДокумент9 страницSun Life Financial and Indian Economic Surge: Case Analysis - International Businessgurubhai24Оценок пока нет

- ENSR InternationalДокумент9 страницENSR Internationalashwin100% (1)

- Bhartiya Samruddhi Investments and Consulting Services LTD.: BasixДокумент28 страницBhartiya Samruddhi Investments and Consulting Services LTD.: BasixAarif FaridiОценок пока нет

- Underwriting 140428035900 Phpapp01Документ42 страницыUnderwriting 140428035900 Phpapp01Jenifer HallОценок пока нет

- Insurance Risk2003Документ7 страницInsurance Risk2003Shaheen MahmudОценок пока нет

- Life Insurance: Nitesh SudanДокумент68 страницLife Insurance: Nitesh SudanNitesh SudanОценок пока нет

- 11-Rural and Social SectorsДокумент13 страниц11-Rural and Social SectorsShiv PratapОценок пока нет

- India Tryst With 5GДокумент10 страницIndia Tryst With 5GShiv PratapОценок пока нет

- Group Insurance ExplainedДокумент37 страницGroup Insurance ExplainedShiv PratapОценок пока нет

- LPGДокумент10 страницLPGShiv PratapОценок пока нет

- Liberalization of India (Gaurav Patel)Документ11 страницLiberalization of India (Gaurav Patel)Gaurav PatelОценок пока нет

- MarketingДокумент90 страницMarketingViveak MishraОценок пока нет

- Industrial RelationsДокумент59 страницIndustrial RelationsShiv PratapОценок пока нет

- Consumer Awareness On TataskyДокумент95 страницConsumer Awareness On TataskyShiv PratapОценок пока нет

- Reviewer in Intermediate Accounting IДокумент9 страницReviewer in Intermediate Accounting ICzarhiena SantiagoОценок пока нет

- Metatron AustraliaДокумент11 страницMetatron AustraliaMetatron AustraliaОценок пока нет

- Self Respect MovementДокумент2 страницыSelf Respect MovementJananee RajagopalanОценок пока нет

- Compatibility Testing: Week 5Документ33 страницыCompatibility Testing: Week 5Bridgette100% (1)

- A Story Behind..: Dimas Budi Satria Wibisana Mario Alexander Industrial Engineering 5Документ24 страницыA Story Behind..: Dimas Budi Satria Wibisana Mario Alexander Industrial Engineering 5Owais AwanОценок пока нет

- All Over AgainДокумент583 страницыAll Over AgainJamie Kris MendozaОценок пока нет

- Global Finance - Introduction AДокумент268 страницGlobal Finance - Introduction AfirebirdshockwaveОценок пока нет

- Role of Islamic Crypto Currency in Supporting Malaysia's Economic GrowthДокумент6 страницRole of Islamic Crypto Currency in Supporting Malaysia's Economic GrowthMarco MallamaciОценок пока нет

- 15-8377 - 3521 Calandria Communications L. Rivera PDFДокумент20 страниц15-8377 - 3521 Calandria Communications L. Rivera PDFRecordTrac - City of OaklandОценок пока нет

- Marketing Strategy of Singapore AirlinesДокумент48 страницMarketing Strategy of Singapore Airlinesi_sonet96% (49)

- Talking About Your Home, Furniture and Your Personal Belongings - Third TemДокумент4 страницыTalking About Your Home, Furniture and Your Personal Belongings - Third TemTony Cañate100% (1)

- 20 Reasons Composers Fail 2019 Reprint PDFДокумент30 страниц20 Reasons Composers Fail 2019 Reprint PDFAlejandroОценок пока нет

- International Waiver Attestation FormДокумент1 страницаInternational Waiver Attestation FormJiabao ZhengОценок пока нет

- Performance Requirements For Organic Coatings Applied To Under Hood and Chassis ComponentsДокумент31 страницаPerformance Requirements For Organic Coatings Applied To Under Hood and Chassis ComponentsIBR100% (2)

- PAPC - Internal Notes PDFДокумент4 страницыPAPC - Internal Notes PDFHrushi Km GowdaОценок пока нет

- Corporate Process Management (CPM) & Control-EsДокумент458 страницCorporate Process Management (CPM) & Control-EsKent LysellОценок пока нет

- Chapter 018Документ12 страницChapter 018api-281340024Оценок пока нет

- Toyota TPMДокумент23 страницыToyota TPMchteo1976Оценок пока нет

- MASM Tutorial PDFДокумент10 страницMASM Tutorial PDFShashankDwivediОценок пока нет

- Intertrigo and Secondary Skin InfectionsДокумент5 страницIntertrigo and Secondary Skin Infectionskhalizamaulina100% (1)

- Chapter 2 Review of Related Lit - 1Документ83 страницыChapter 2 Review of Related Lit - 1CathyОценок пока нет

- Fundamentals of Accounting - I FinallДокумент124 страницыFundamentals of Accounting - I Finallyitbarek MОценок пока нет

- Alvin - Goldman - and - Dennis - Whitcomb (Eds) - Social - Epistemology - Essential - Readings - 2011 PDFДокумент368 страницAlvin - Goldman - and - Dennis - Whitcomb (Eds) - Social - Epistemology - Essential - Readings - 2011 PDFOvejaNegra100% (2)

- Lesson 1 Intro - LatinДокумент11 страницLesson 1 Intro - LatinJohnny NguyenОценок пока нет

- Pilar College of Zamboanga City, IncДокумент14 страницPilar College of Zamboanga City, IncIvy VillalobosОценок пока нет

- Fact-Sheet Pupils With Asperger SyndromeДокумент4 страницыFact-Sheet Pupils With Asperger SyndromeAnonymous Pj6OdjОценок пока нет

- Cub Cadet 1650 PDFДокумент46 страницCub Cadet 1650 PDFkbrckac33% (3)

- 14.marifosque v. People 435 SCRA 332 PDFДокумент8 страниц14.marifosque v. People 435 SCRA 332 PDFaspiringlawyer1234Оценок пока нет

- PersonalDevelopment Q1 Module 2Документ7 страницPersonalDevelopment Q1 Module 2Stephanie DilloОценок пока нет

- Unit-2 Fourier Series & Integral: 2130002 - Advanced Engineering MathematicsДокумент143 страницыUnit-2 Fourier Series & Integral: 2130002 - Advanced Engineering MathematicsDarji DhrutiОценок пока нет