Вам также может понравиться

- Diminishing MusharakahДокумент19 страницDiminishing MusharakahKhalid WaheedОценок пока нет

- Islamic Modes For Agricultural Financing: PRODUCTS - Diminishing MusharakahДокумент19 страницIslamic Modes For Agricultural Financing: PRODUCTS - Diminishing MusharakahAlHuda Centre of Islamic Banking & Economics (CIBE)Оценок пока нет

- Lecture-3-Mudaraba As A Mode of Islamic FinanceДокумент38 страницLecture-3-Mudaraba As A Mode of Islamic FinanceJaved AnwarОценок пока нет

- Musharaka Mode of Islamic BankingДокумент25 страницMusharaka Mode of Islamic BankingNaveed SaeedОценок пока нет

- Mudarba & MusharkaДокумент27 страницMudarba & Musharkakamranp1100% (1)

- Problems and Their Solution in MudarabahДокумент43 страницыProblems and Their Solution in Mudarabahatiqa tanveerОценок пока нет

- FSA 4 Financing ActivitiesДокумент51 страницаFSA 4 Financing Activitiessubhrodeep chowdhuryОценок пока нет

- 05 Islamic Banking - DepositsДокумент20 страниц05 Islamic Banking - DepositsAmirah ShukriОценок пока нет

- Chapter 6Документ21 страницаChapter 6Abdiwahab AbdikadirОценок пока нет

- Financial Instrument v.03Документ49 страницFinancial Instrument v.03ashaheen2704Оценок пока нет

- MudarabahДокумент25 страницMudarabahDanish Riaz Shaikh100% (1)

- Islamic Modes of Finance: Theory and Key Shariah PrinciplesДокумент40 страницIslamic Modes of Finance: Theory and Key Shariah PrinciplesnuasyamОценок пока нет

- Depositaries and Mutual Funds: MBA III Semester Finance Elective Merchant Banking and Financial Services Ranjani JДокумент36 страницDepositaries and Mutual Funds: MBA III Semester Finance Elective Merchant Banking and Financial Services Ranjani Jwelcome2jungleОценок пока нет

- Mudarabah and Its Application in Islamic BankingДокумент26 страницMudarabah and Its Application in Islamic Bankingsaif khanОценок пока нет

- KUPres 7 Nov 2010Документ63 страницыKUPres 7 Nov 2010Hasan Irfan SiddiquiОценок пока нет

- Assignment 2 - FIN 545Документ7 страницAssignment 2 - FIN 545tuna100% (3)

- Working Capital ManagementДокумент36 страницWorking Capital ManagementManjunath LeoОценок пока нет

- MF IntroductionДокумент21 страницаMF Introductionutsav mandalОценок пока нет

- What Is Relationship Banking?Документ36 страницWhat Is Relationship Banking?llllkkkkОценок пока нет

- Mudharabah FinancingДокумент4 страницыMudharabah FinancingHisyamОценок пока нет

- BAW 4614 Advanced Financial Accounting ReportingДокумент52 страницыBAW 4614 Advanced Financial Accounting ReportingTEE YAN YING UnknownОценок пока нет

- 7SOGSS FM LECTURE 7 Sources of Finance 1Документ60 страниц7SOGSS FM LECTURE 7 Sources of Finance 1Right Karl-Maccoy HattohОценок пока нет

- Syllabus Summary Course: Financial Statement Analysis and Valuation (F-401)Документ8 страницSyllabus Summary Course: Financial Statement Analysis and Valuation (F-401)Md Ohidur RahmanОценок пока нет

- Financial Appraisal: - Adequacy of Rate of Return - Financing PatternДокумент26 страницFinancial Appraisal: - Adequacy of Rate of Return - Financing PatternTibebu MerideОценок пока нет

- Mutual Fund: An OverviewДокумент54 страницыMutual Fund: An Overviewnikitashah14Оценок пока нет

- Hassan Faraz - 27th July 2021Документ48 страницHassan Faraz - 27th July 2021shah zaibОценок пока нет

- Reporting and Analysing LiabilitiesДокумент52 страницыReporting and Analysing LiabilitiesSuptoОценок пока нет

- Off Balance Sheet Transactions For Islamic BanksДокумент25 страницOff Balance Sheet Transactions For Islamic BanksSyed MohiuddinОценок пока нет

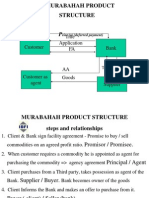

- Murabahah Product Structure: Title Application FAДокумент26 страницMurabahah Product Structure: Title Application FAUmair UddinОценок пока нет

- Features of An Islamic BankДокумент17 страницFeatures of An Islamic BankHafsa MemonОценок пока нет

- Rehmanwaheed - 3180 - 17836 - 2 - 11. MudarabahДокумент21 страницаRehmanwaheed - 3180 - 17836 - 2 - 11. MudarabahSadia AbidОценок пока нет

- MusharakaДокумент34 страницыMusharakaAbdul HafeezОценок пока нет

- BTLPДокумент282 страницыBTLPBijay PoudelОценок пока нет

- Islamic Banking Lecture 5 & 6Документ33 страницыIslamic Banking Lecture 5 & 6Soban MamoonОценок пока нет

- Welcome To The Presentation: Sanzida Begum ID: 17002Документ11 страницWelcome To The Presentation: Sanzida Begum ID: 17002Sanzida BegumОценок пока нет

- Lecture Notes - Due DiligenceДокумент9 страницLecture Notes - Due DiligenceHimanshu DuttaОценок пока нет

- Capital and Its Types: Name: Saroop Cms:42529 Section: B Semester: 6 Assignment:2Документ9 страницCapital and Its Types: Name: Saroop Cms:42529 Section: B Semester: 6 Assignment:2Sanjna ChimnaniОценок пока нет

- Features of An Islamic Bank.Документ15 страницFeatures of An Islamic Bank.atifkhan8905722Оценок пока нет

- Forms of Islamic BankingДокумент55 страницForms of Islamic BankingMuhammad Talha KhanОценок пока нет

- Apply Principles of Professional Practice To Work in The Financial Services IndustryДокумент46 страницApply Principles of Professional Practice To Work in The Financial Services Industryd.achmarОценок пока нет

- MudarabahДокумент21 страницаMudarabahAli Raza0% (1)

- Pt7 - Lending To Business CustomersДокумент38 страницPt7 - Lending To Business Customerssavira andayaniОценок пока нет

- CF Unit 2Документ30 страницCF Unit 2Saravanan ShanmugamОценок пока нет

- Commercial Banking Lending Policies of BanksДокумент47 страницCommercial Banking Lending Policies of Banksrahul8909Оценок пока нет

- Long Term Sources of FundsДокумент63 страницыLong Term Sources of FundsAnonymous 9YyCbPAОценок пока нет

- 20773d1259766411 Financial Services M y Khan Ppts CH 1 NBFC M.y.khanДокумент54 страницы20773d1259766411 Financial Services M y Khan Ppts CH 1 NBFC M.y.khanPriyanka VashistОценок пока нет

- Financial Accounting: Session - 17: Accounting For DebtДокумент11 страницFinancial Accounting: Session - 17: Accounting For DebtSuraj KumarОценок пока нет

- Islamic Modes For Agricultural Financing: PRODUCTS - Diminishing MusharakahДокумент15 страницIslamic Modes For Agricultural Financing: PRODUCTS - Diminishing MusharakahAlHuda Centre of Islamic Banking & Economics (CIBE)Оценок пока нет

- Advocates and Partnership NotesДокумент5 страницAdvocates and Partnership Notespauline1988Оценок пока нет

- DYBSAAgn313 - Accounting For Government & Non-Profit Organizations (SEMI-FINAL MODULE)Документ14 страницDYBSAAgn313 - Accounting For Government & Non-Profit Organizations (SEMI-FINAL MODULE)Jonnafe Almendralejo IntanoОценок пока нет

- Insolvency and Bankruptcy CodeДокумент18 страницInsolvency and Bankruptcy CodeSudip Issac SamОценок пока нет

- Chapter 10 Investments in Debt SecuritiesДокумент24 страницыChapter 10 Investments in Debt SecuritiesChristian Jade Lumasag NavaОценок пока нет

- Practical Application of Mudarabah and MusharakahДокумент7 страницPractical Application of Mudarabah and MusharakahFaizan Ch50% (2)

- Financial MGTДокумент1 страницаFinancial MGTtuhin khanОценок пока нет

- 10 - Overview of Financing ChoicesДокумент11 страниц10 - Overview of Financing ChoicesAmarnath JvОценок пока нет

- WK 5 - 6 Company AccountsДокумент41 страницаWK 5 - 6 Company AccountsmensahshadrachnyarkoОценок пока нет

- Chapter4. BankingДокумент38 страницChapter4. BankingdhitalkhushiОценок пока нет

- Accounting For Companies-1Документ50 страницAccounting For Companies-1daniel.maina2005Оценок пока нет

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingОт EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingОценок пока нет

- Analysis of Coupled Microstrip Lines With DGS UWB PDFДокумент5 страницAnalysis of Coupled Microstrip Lines With DGS UWB PDFaleenaaaОценок пока нет

- Analysis of Coupled Microstrip Lines With DGS UWB Printed FilterДокумент5 страницAnalysis of Coupled Microstrip Lines With DGS UWB Printed FilteraleenaaaОценок пока нет

- LogoДокумент2 страницыLogoaleenaaaОценок пока нет

- Taming Control Flow: A Structured Approach To Eliminating Goto StatementsДокумент12 страницTaming Control Flow: A Structured Approach To Eliminating Goto StatementsaleenaaaОценок пока нет

- Commercial and Investment Banking: by Asiya SohailДокумент14 страницCommercial and Investment Banking: by Asiya SohailaleenaaaОценок пока нет

- Statement For Contract # 1003901674: Muhammad JavedДокумент15 страницStatement For Contract # 1003901674: Muhammad JavedaleenaaaОценок пока нет

- Presented By: Helical and Cavity Backed Helical AntennaДокумент12 страницPresented By: Helical and Cavity Backed Helical AntennaaleenaaaОценок пока нет

- Lecture 10,11Документ46 страницLecture 10,11aleenaaaОценок пока нет

- C C C C C C C C C CДокумент5 страницC C C C C C C C C CaleenaaaОценок пока нет

- Bridge Rectifiers: Presented To: Sir Abbas Presented By: Shabana HafeezДокумент23 страницыBridge Rectifiers: Presented To: Sir Abbas Presented By: Shabana HafeezaleenaaaОценок пока нет

- Puppet Demo Aim A 05Документ8 страницPuppet Demo Aim A 05aleenaaaОценок пока нет

- Financial Reporting Strathmore University Notes and Revision KitДокумент551 страницаFinancial Reporting Strathmore University Notes and Revision KitLazarus AmaniОценок пока нет

- Word Bank Impact PPPДокумент23 страницыWord Bank Impact PPPdewangga04radenОценок пока нет

- Gym Business Plan ExampleДокумент36 страницGym Business Plan ExamplecobbymarkОценок пока нет

- Chapter 4 Measuring Financial PerformanceДокумент4 страницыChapter 4 Measuring Financial Performanceabdiqani abdulaahi100% (1)

- Project Report PDFДокумент73 страницыProject Report PDFAkhilaSedimbi100% (1)

- KPMG Ind As Illustrattive Financial Statements 2019Документ217 страницKPMG Ind As Illustrattive Financial Statements 2019Utsav HiraniОценок пока нет

- Instructions:: Question Paper Booklet CodeДокумент20 страницInstructions:: Question Paper Booklet CodeadiОценок пока нет

- FM Rocks Book by CA Swapnil PatniДокумент124 страницыFM Rocks Book by CA Swapnil Patniraj bawaОценок пока нет

- 2020 BF - BS - BEC - HRM 120 Sessional ExamДокумент19 страниц2020 BF - BS - BEC - HRM 120 Sessional Examisaiahsinkala101Оценок пока нет

- AgriPinay Simple Business PlanДокумент6 страницAgriPinay Simple Business PlanKristy Dela PeñaОценок пока нет

- Case MDPK Pertemuan 2Документ15 страницCase MDPK Pertemuan 2anggi anythingОценок пока нет

- Goods and Services Tax (GST) in IndiaДокумент30 страницGoods and Services Tax (GST) in IndiarupalОценок пока нет

- Pacific Airlines Operated Both An Airline and Several Rental CarДокумент1 страницаPacific Airlines Operated Both An Airline and Several Rental CarAmit PandeyОценок пока нет

- Fundamentals of Accountancy Lesson 1Документ6 страницFundamentals of Accountancy Lesson 1Rojane L. AlcantaraОценок пока нет

- Department of Education: Caraga Region Schools Division of Surigao Del SurДокумент2 страницыDepartment of Education: Caraga Region Schools Division of Surigao Del SurSim BelsondraОценок пока нет

- 3271010Документ4 страницы3271010mohitgaba19Оценок пока нет

- Detailed Lesson Plan in Fundamentals of AccountancyДокумент5 страницDetailed Lesson Plan in Fundamentals of AccountancyKrisha Joy CofinoОценок пока нет

- Sip Report AuditДокумент23 страницыSip Report AuditDhiraj singhОценок пока нет

- Foreign Exchange Exercise SP2017!3!1 2Документ5 страницForeign Exchange Exercise SP2017!3!1 2Stephen Ondiek0% (2)

- Hul Annual Report 2017 18 - tcm1255 523195 - enДокумент184 страницыHul Annual Report 2017 18 - tcm1255 523195 - enArnav ChakrabortyОценок пока нет

- Numerical Reasoning Formulas PDFДокумент7 страницNumerical Reasoning Formulas PDFandreea_zgrОценок пока нет

- Waterways Continuous ProblemДокумент18 страницWaterways Continuous ProblemAboi Boboi60% (5)

- Capital Structure of TCSДокумент36 страницCapital Structure of TCSpassinikunj50% (2)

- Taxation Ans AnsДокумент10 страницTaxation Ans AnsTebashiniОценок пока нет

- LESSON 3 PAS 8, 10, and 24Документ46 страницLESSON 3 PAS 8, 10, and 24Beatriz Jade TicobayОценок пока нет

- New Personal Salary Loan Application: (Last Name) (First Name) (Middle Initial) (Suffix)Документ2 страницыNew Personal Salary Loan Application: (Last Name) (First Name) (Middle Initial) (Suffix)En-en FrioОценок пока нет

- Disposable Plastic SyringesДокумент1 страницаDisposable Plastic Syringeseiribooks0% (2)

- Topic 3-DeprДокумент28 страницTopic 3-DeprMichael.land65Оценок пока нет