Вам также может понравиться

- Economics For Managers GTU MBA Sem 1 Chapter 1Документ14 страницEconomics For Managers GTU MBA Sem 1 Chapter 1Rushabh Vora100% (1)

- 3&4. Ten Principles of EconomicsДокумент22 страницы3&4. Ten Principles of EconomicsJoan KeziaОценок пока нет

- #Bba Microeconomics 10 PrinciplesДокумент31 страница#Bba Microeconomics 10 PrinciplesMadiha Umer UqailiОценок пока нет

- Principles of EconomicsДокумент21 страницаPrinciples of EconomicsJEAN KANTY A. ALVAREZОценок пока нет

- Principles of Economics,: Powerpoint® Lecture PresentationДокумент30 страницPrinciples of Economics,: Powerpoint® Lecture PresentationAhmed ShaanОценок пока нет

- Ch1 - Principles of MacroeconomicsДокумент10 страницCh1 - Principles of MacroeconomicsMai Anh NguyễnОценок пока нет

- TTXXXДокумент29 страницTTXXXSagar ShahОценок пока нет

- Lecture 1 - Introduction To Economics and Economic SystemsДокумент42 страницыLecture 1 - Introduction To Economics and Economic Systemsvillaverdev01Оценок пока нет

- Micro1 Introduction & PrinciplesДокумент46 страницMicro1 Introduction & Principleskshubhanshu02Оценок пока нет

- The Word Economy Comes From A Greek Word For "One Who Manages A Household." - A Household, A Manager and An Economy Face Many DecisionsДокумент26 страницThe Word Economy Comes From A Greek Word For "One Who Manages A Household." - A Household, A Manager and An Economy Face Many DecisionsH.R. RobinОценок пока нет

- Chapter 1 - Ten Principles of EconomicsДокумент22 страницыChapter 1 - Ten Principles of EconomicsLe Trinh Anh (K17 HCM)Оценок пока нет

- Lecture 1Документ24 страницыLecture 1hassanОценок пока нет

- Ten Principles of EconomicsДокумент21 страницаTen Principles of EconomicsThành PhạmОценок пока нет

- Economics Oct 30 - MergedДокумент56 страницEconomics Oct 30 - MergedRamiz Ul HasanОценок пока нет

- Eco 201 Mod 1 Notes CHДокумент8 страницEco 201 Mod 1 Notes CHJohn Mark TabusoОценок пока нет

- Summary of Principles of Economy Chapter 1Документ6 страницSummary of Principles of Economy Chapter 1Arizfa100% (1)

- Chapter One MICROECONOMICSДокумент24 страницыChapter One MICROECONOMICSDek OmarОценок пока нет

- Chapter 1 Introduction in Microeconomics: Dr. ShonДокумент66 страницChapter 1 Introduction in Microeconomics: Dr. ShonШохрух МаджидовОценок пока нет

- Chapter 1 - Macroeconomics Final Exam Compilation - SarahДокумент7 страницChapter 1 - Macroeconomics Final Exam Compilation - SarahSARAH CHRISTINE TAMARIAОценок пока нет

- UTS Ekonomi 3 CombinepptДокумент10 страницUTS Ekonomi 3 Combineppttriaa.wulandОценок пока нет

- Principles of Economics,: Powerpoint® Lecture PresentationДокумент30 страницPrinciples of Economics,: Powerpoint® Lecture PresentationuniqueMyomОценок пока нет

- Prinsip EkonomiДокумент19 страницPrinsip EkonomiDandy Maslow Panungkunan ManurungОценок пока нет

- 01 - Micro - CH - 1 - Ten Principles of EconomicsДокумент30 страниц01 - Micro - CH - 1 - Ten Principles of EconomicsBhaskar KondaОценок пока нет

- Principles of EconomicsДокумент25 страницPrinciples of EconomicsVerinice NañascaОценок пока нет

- Introduction To EconomicsДокумент14 страницIntroduction To EconomicsKemalОценок пока нет

- Introduction To MacroeconomicsДокумент21 страницаIntroduction To MacroeconomicsTariq KilaniОценок пока нет

- Chapter 1 - Ten Principles of EconomicsДокумент29 страницChapter 1 - Ten Principles of Economicstes.max344301Оценок пока нет

- Ten Principles of Economics: ConomicsДокумент29 страницTen Principles of Economics: ConomicsMazen AymanОценок пока нет

- Economic PrinciplesДокумент6 страницEconomic PrinciplesRockacerОценок пока нет

- Introduction To Business Economics - I: Instructor: Prof - Dr.Qaisar Abbas Course Code: ECO 400Документ18 страницIntroduction To Business Economics - I: Instructor: Prof - Dr.Qaisar Abbas Course Code: ECO 400Zohaib AnserОценок пока нет

- Abu Naser Mohammad Saif: Assistant ProfessorДокумент29 страницAbu Naser Mohammad Saif: Assistant ProfessorSH RaihanОценок пока нет

- ECO1104 Microeconomics NotesДокумент26 страницECO1104 Microeconomics NotesPriya Srinivasan100% (1)

- Applied Economics MIDTERM REVIEWERДокумент13 страницApplied Economics MIDTERM REVIEWERKate JavierОценок пока нет

- Chapter 1 Ten Principles of EconomicsДокумент29 страницChapter 1 Ten Principles of EconomicsNika AntelavaОценок пока нет

- Introduction To Business - Topic 1Документ8 страницIntroduction To Business - Topic 1cbhiba98Оценок пока нет

- 10 Principles of EconomicsДокумент18 страниц10 Principles of EconomicsanujjalansОценок пока нет

- Macroeconomi CS Compiled Topics: in Partial Fulfillment For Economics 2A BE 311/8:00-9:00AM/7172Документ81 страницаMacroeconomi CS Compiled Topics: in Partial Fulfillment For Economics 2A BE 311/8:00-9:00AM/7172Carmela Mae Campo DuronОценок пока нет

- Ten Principles of EconomicsДокумент27 страницTen Principles of EconomicsYannah HidalgoОценок пока нет

- Principle of Economics - Gregory Mankiw - Class AssignmentДокумент9 страницPrinciple of Economics - Gregory Mankiw - Class AssignmentChinmayee ParchureОценок пока нет

- Topic 1: Introduction To Microeconomics: Economic ProblemДокумент8 страницTopic 1: Introduction To Microeconomics: Economic ProblemNadine EudelaОценок пока нет

- The Principles of EconomicsДокумент10 страницThe Principles of Economicsileana.alexe399Оценок пока нет

- Hs 101 (S3) - Microeconomics: Conan MukherjeeДокумент49 страницHs 101 (S3) - Microeconomics: Conan MukherjeeSaurabhGuptaОценок пока нет

- Ten Principles of EconomicsДокумент29 страницTen Principles of EconomicschanpeinОценок пока нет

- ECO 533 - Topic 1Документ21 страницаECO 533 - Topic 1Md Taskinur RahmanОценок пока нет

- Engineering Economics & Management: Week 1 Prepared By: Miss. Fatima M. SaleemДокумент34 страницыEngineering Economics & Management: Week 1 Prepared By: Miss. Fatima M. SaleemJehangir VakilОценок пока нет

- CH 1 - Introduction MicroeconomicsДокумент45 страницCH 1 - Introduction MicroeconomicsAchmad TriantoОценок пока нет

- Introductory Economics Lecture1 : - Ten PrinciplesДокумент25 страницIntroductory Economics Lecture1 : - Ten PrinciplesSuper TuberОценок пока нет

- LEC # 2 Ten Principles of Economics. (Mankiw Chapter No. 1)Документ23 страницыLEC # 2 Ten Principles of Economics. (Mankiw Chapter No. 1)drmasood khattakОценок пока нет

- 10 Principles of Economic1Документ3 страницы10 Principles of Economic1rhiza aperinОценок пока нет

- Introduction To Economics: Dr. S.K. Shanthi Chair-Professor Union Bank Center For Banking ExcellenceДокумент12 страницIntroduction To Economics: Dr. S.K. Shanthi Chair-Professor Union Bank Center For Banking ExcellenceAnkit LodhaОценок пока нет

- Ten Principles of Economics: IcroeonomicsДокумент24 страницыTen Principles of Economics: IcroeonomicsDuaa TahirОценок пока нет

- Module 1: Concepts: Chapters 1, 2, 7, 8 & 11:216-222Документ185 страницModule 1: Concepts: Chapters 1, 2, 7, 8 & 11:216-222Bao AnhОценок пока нет

- Chapter 1 - Principles of EconomicsДокумент27 страницChapter 1 - Principles of Economicsdaniel chuaОценок пока нет

- Handout01 2022Документ24 страницыHandout01 2022Uiko JimboОценок пока нет

- CH 01Документ5 страницCH 01nisarg_Оценок пока нет

- General Economics - 1st WeekДокумент33 страницыGeneral Economics - 1st WeekVật Tư Trực TuyếnОценок пока нет

- 10 Principles of EconДокумент9 страниц10 Principles of EconRish DagaragaОценок пока нет

- Chapter 1: Ten Principles of Microeconomics: Economy Households and EconomiesДокумент3 страницыChapter 1: Ten Principles of Microeconomics: Economy Households and EconomiesManel KricheneОценок пока нет

- Econ ReviewerДокумент11 страницEcon ReviewerMark SerranoОценок пока нет

- Its All in the Price: A Business Solution to the EconomyОт EverandIts All in the Price: A Business Solution to the EconomyОценок пока нет

- Porters Five Forces Model - Textile IndustryДокумент3 страницыPorters Five Forces Model - Textile Industrykritiangra60% (10)

- Paper 3Документ6 страницPaper 3Safwan mansuriОценок пока нет

- ABOUTДокумент93 страницыABOUTSafwan mansuriОценок пока нет

- Fundamental AnalysisДокумент6 страницFundamental AnalysisSafwan mansuriОценок пока нет

- Porters Five Forces Model - Textile IndustryДокумент3 страницыPorters Five Forces Model - Textile Industrykritiangra60% (10)

- INVESTOR'S PERCEPTION TOWARDS MUTUAL FUNDS Project ReportДокумент80 страницINVESTOR'S PERCEPTION TOWARDS MUTUAL FUNDS Project ReportRaghavendra yadav KM86% (161)

- 14 AppendixДокумент5 страниц14 AppendixJohn CarpenterОценок пока нет

- Paper 1Документ8 страницPaper 1Safwan mansuriОценок пока нет

- Questionnaire On Mutual Fund InvetmentДокумент4 страницыQuestionnaire On Mutual Fund InvetmentSafwan mansuriОценок пока нет

- Porters Five Forces Model - Textile IndustryДокумент3 страницыPorters Five Forces Model - Textile Industrykritiangra60% (10)

- CottonДокумент4 страницыCottonSafwan mansuriОценок пока нет

- Decision Support SystemsДокумент33 страницыDecision Support SystemsJacton OpiyoОценок пока нет

- Textile Machinery MarketДокумент32 страницыTextile Machinery MarketRonak JoshiОценок пока нет

- Textile SectorДокумент31 страницаTextile SectorSafwan mansuriОценок пока нет

- LiДокумент28 страницLiSafwan mansuriОценок пока нет

- CottonДокумент4 страницыCottonSafwan mansuriОценок пока нет

- 14 AppendixДокумент5 страниц14 AppendixJohn CarpenterОценок пока нет

- Reoprt On "Portfolio Management Services" by Sharekhan Stock Broking LimitedДокумент111 страницReoprt On "Portfolio Management Services" by Sharekhan Stock Broking LimitedAshutosh Rathod91% (22)

- Share KhanДокумент127 страницShare KhanSafwan mansuriОценок пока нет

- Unit 1 Lesson 17: Test For Optimal Solution To A Transportation Problem Learning ObjectiveДокумент10 страницUnit 1 Lesson 17: Test For Optimal Solution To A Transportation Problem Learning ObjectiveMehran M ZargarОценок пока нет

- Assignment Problem: Unbalanced and Maximal Assignment ProblemsДокумент4 страницыAssignment Problem: Unbalanced and Maximal Assignment ProblemsSafwan mansuriОценок пока нет

- Job Application Letter1Документ3 страницыJob Application Letter1Safwan mansuriОценок пока нет

- Duality and Sensitivity: 4.1 Primal Dual FormulationsДокумент19 страницDuality and Sensitivity: 4.1 Primal Dual FormulationsSafwan mansuriОценок пока нет

- 24 Standard Costing and Variance AnalysisДокумент12 страниц24 Standard Costing and Variance AnalysisSafwan mansuriОценок пока нет

- Management Function Monetory and Non-Monetory Motivation Verbal and Non - Varbal Communication Firms in Compititon of Market Financial StatementДокумент3 страницыManagement Function Monetory and Non-Monetory Motivation Verbal and Non - Varbal Communication Firms in Compititon of Market Financial StatementSafwan mansuriОценок пока нет

- Assignment Problem: Unbalanced and Maximal Assignment ProblemsДокумент4 страницыAssignment Problem: Unbalanced and Maximal Assignment ProblemsSafwan mansuriОценок пока нет

- P 4762 ProjectonasianpaintsДокумент58 страницP 4762 Projectonasianpaintsraghuram952Оценок пока нет

- Annual Report 13 14 PDFДокумент180 страницAnnual Report 13 14 PDFSafwan mansuriОценок пока нет

- "Title of The Project": Veer Narmad South Gujarat University (Vnsgu)Документ85 страниц"Title of The Project": Veer Narmad South Gujarat University (Vnsgu)Safwan mansuriОценок пока нет

- New Age Tourism: A Passage For India'S Economic DevelopmentДокумент21 страницаNew Age Tourism: A Passage For India'S Economic Developmentabbi_UandMEОценок пока нет

- ATH AssignmentДокумент5 страницATH AssignmentAnonymous qbVaMYIIZ83% (6)

- DIVERSIFICATIONДокумент72 страницыDIVERSIFICATIONshaRUKHОценок пока нет

- PHD in Economics, Lecturer Professor, "Dimitrie Cantemir" Christian University BraşovДокумент6 страницPHD in Economics, Lecturer Professor, "Dimitrie Cantemir" Christian University BraşovellennaОценок пока нет

- Introduction To Globalization-Contemporary WorldДокумент29 страницIntroduction To Globalization-Contemporary WorldBRILIAN TOMAS0% (1)

- Life of Jay Gould, How He Made His Millions .. (1892)Документ500 страницLife of Jay Gould, How He Made His Millions .. (1892)Jello KokkustiОценок пока нет

- Abhay Project FinalДокумент14 страницAbhay Project FinalAnonymous h95KhDXKjCОценок пока нет

- Eduardo Serrão - Potential Business For Chickens and Pigs and Their Products in Timor-LesteДокумент6 страницEduardo Serrão - Potential Business For Chickens and Pigs and Their Products in Timor-LestePapers and Powerpoints from UNTL-VU Joint Conferenes in DiliОценок пока нет

- 101 Crucial Lessons They Don't Teach You in Business School - Forbes Calls This Book 1 of 6 Books That All Entrepreneurs Must Read Right Now Along With The 7 Habits of Highly Effective PeopleДокумент134 страницы101 Crucial Lessons They Don't Teach You in Business School - Forbes Calls This Book 1 of 6 Books That All Entrepreneurs Must Read Right Now Along With The 7 Habits of Highly Effective Peopleangel episcopeОценок пока нет

- KiksДокумент3 страницыKiksAndrea DeteraОценок пока нет

- 084.anthony Falasca With 'Lusan Pty LTD' and 'Kool Fun Toys (HK) Pty LTD': LinkedinДокумент5 страниц084.anthony Falasca With 'Lusan Pty LTD' and 'Kool Fun Toys (HK) Pty LTD': LinkedinFlinders TrusteesОценок пока нет

- Compensation For Executive and Supervisory Board MembersДокумент2 страницыCompensation For Executive and Supervisory Board MembersProjОценок пока нет

- Mba ProjectДокумент73 страницыMba Projectjaya sai sree harishОценок пока нет

- Sensitivity AnalysisДокумент19 страницSensitivity AnalysisMarcin KotОценок пока нет

- CH 10 Hull Fundamentals 8 The DДокумент20 страницCH 10 Hull Fundamentals 8 The DjlosamОценок пока нет

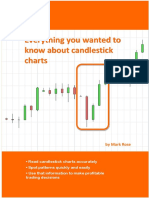

- Candlestick BookДокумент22 страницыCandlestick Bookrajveer40475% (4)

- New Venture Development Process-TruefanДокумент34 страницыNew Venture Development Process-Truefanpowerhanks50% (2)

- Risk Profiles of Islamic BankДокумент31 страницаRisk Profiles of Islamic Bankkadung@gmail.comОценок пока нет

- Allama Iqbal Open University, Islamabad (Department of Business Administration)Документ8 страницAllama Iqbal Open University, Islamabad (Department of Business Administration)apovtigrtОценок пока нет

- Need of InsuranceДокумент4 страницыNeed of InsuranceNAISHADH DESAIОценок пока нет

- Bloom Consulting Country Brand Ranking Trade 2013Документ36 страницBloom Consulting Country Brand Ranking Trade 2013The Santiago TimesОценок пока нет

- RMR 01-02Документ8 страницRMR 01-02matinikkiОценок пока нет

- AXA Unit-Linked Funds 2022 Annual ReportДокумент36 страницAXA Unit-Linked Funds 2022 Annual ReportDiana Mark AndrewОценок пока нет

- Joint Venture: Joint Venture Tecnology and Global Competition Harmandeep SinghДокумент20 страницJoint Venture: Joint Venture Tecnology and Global Competition Harmandeep SinghHarman SidhuОценок пока нет

- Strategy in The Global EnvironmentДокумент28 страницStrategy in The Global EnvironmentjesusaranОценок пока нет

- Entoria Profile PDFДокумент14 страницEntoria Profile PDFAnonymous JD4pStUhОценок пока нет

- Nature of Indian EconomyДокумент4 страницыNature of Indian Economykarthika0% (1)

- Auditing by BeasleyДокумент10 страницAuditing by BeasleyElsa MendozaОценок пока нет

- Investment Project EvaluationДокумент2 страницыInvestment Project EvaluationDare SmithОценок пока нет

- Nekilnojamas TurtasДокумент75 страницNekilnojamas TurtasKarolis BaltrukėnasОценок пока нет