Вам также может понравиться

- 7 Eleven PhilippinesДокумент435 страниц7 Eleven PhilippinesDataGroup Retailer Analysis81% (16)

- Seligram Summary DetailsДокумент6 страницSeligram Summary DetailsSachin MailareОценок пока нет

- Seligram Case QuestionsДокумент2 страницыSeligram Case QuestionsZain Bharwani100% (1)

- SUBJECT: Analyses and Recommendations For The Different Cost AccountingДокумент4 страницыSUBJECT: Analyses and Recommendations For The Different Cost AccountinglddОценок пока нет

- Vaibhav Maheshwari Merrimack Tractors 2011pgp926Документ3 страницыVaibhav Maheshwari Merrimack Tractors 2011pgp926studvabzОценок пока нет

- Sales Operations PlanningДокумент28 страницSales Operations PlanningHoang PhuОценок пока нет

- Strategic Operation Management (Case Study of Iceland)Документ21 страницаStrategic Operation Management (Case Study of Iceland)Plabon IslamОценок пока нет

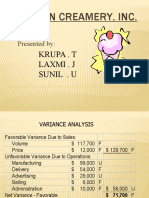

- Boston CreameryДокумент11 страницBoston CreameryJelline Gaza100% (3)

- Mystic SportsДокумент34 страницыMystic SportshelloОценок пока нет

- 05 Wilkerson Company Solution - StudentsДокумент9 страниц05 Wilkerson Company Solution - StudentsVinyabhooshan Bajpai PGP 2022-24 Batch100% (1)

- Polar SportsДокумент9 страницPolar SportsAbhishek RawatОценок пока нет

- MANAC II - Morrissey Forgings CaseДокумент8 страницMANAC II - Morrissey Forgings CaseKaran Oberoi100% (1)

- Singapore Metals LimitedДокумент6 страницSingapore Metals LimitedNarinderОценок пока нет

- Elwy Melina-Sarah MHCДокумент7 страницElwy Melina-Sarah MHCpalak32Оценок пока нет

- EX 1 - WilkersonДокумент8 страницEX 1 - WilkersonDror PazОценок пока нет

- Chromium Plating On Abs PlasticДокумент11 страницChromium Plating On Abs PlasticMohammed Shafi AhmedОценок пока нет

- Industrial Grinders NVДокумент6 страницIndustrial Grinders NVCarrie Stevens100% (1)

- Case SolutionДокумент20 страницCase SolutionKhurram Sadiq (Father Name:Muhammad Sadiq)Оценок пока нет

- Dentin Brass Case Study3Документ13 страницDentin Brass Case Study3Hosein Rahmati100% (2)

- MA Session 5 PDFДокумент35 страницMA Session 5 PDFArkaprabha GhoshОценок пока нет

- At Kenerey Purchasing Chess BoardДокумент20 страницAt Kenerey Purchasing Chess BoardAhsan Ahmad100% (2)

- AJAX OriginalДокумент7 страницAJAX Originalreva_radhakrish1834Оценок пока нет

- Huron Automotive Company ExcelllДокумент6 страницHuron Automotive Company Excelllmaximus0903Оценок пока нет

- Otago MuseumДокумент19 страницOtago MuseumFoamdomeОценок пока нет

- Reichard MaschinenДокумент23 страницыReichard MaschinenAliefiah AZОценок пока нет

- This Study Resource Was: Teaching NoteДокумент8 страницThis Study Resource Was: Teaching NoteSuci NurlaeliОценок пока нет

- Reichard Maschinen DocumentДокумент5 страницReichard Maschinen DocumentLucille Ausborn100% (1)

- Reichard Machinen GMBH - CalculationДокумент4 страницыReichard Machinen GMBH - CalculationKarina RusmanОценок пока нет

- Group 7 - Excel - Destin BrassДокумент9 страницGroup 7 - Excel - Destin BrassSaumya SahaОценок пока нет

- Cafe Monte BiancoДокумент21 страницаCafe Monte BiancoWilliam Torrez OrozcoОценок пока нет

- Otago's MuseumДокумент5 страницOtago's Museumyecika50% (2)

- South Dakota Microbrewery CaseДокумент7 страницSouth Dakota Microbrewery CaseNỏ Mô100% (2)

- Unitron CorporationДокумент7 страницUnitron CorporationERika PratiwiОценок пока нет

- Seligram, IncДокумент5 страницSeligram, IncAto SumartoОценок пока нет

- Fas J1Документ7 страницFas J1anon_839867152Оценок пока нет

- Economic Impact of Oakland Athletics Ballpark at Howard TerminalДокумент13 страницEconomic Impact of Oakland Athletics Ballpark at Howard TerminalZennie AbrahamОценок пока нет

- JHT Case ExcelДокумент4 страницыJHT Case Excelanup akasheОценок пока нет

- Siemens Coma CaseДокумент5 страницSiemens Coma Caseshshank pandeyОценок пока нет

- Stuart DawДокумент3 страницыStuart DawHarsh SoniОценок пока нет

- This Study Resource Was: Forner CarpetДокумент4 страницыThis Study Resource Was: Forner CarpetLi CarinaОценок пока нет

- Boston Creamery CaseДокумент9 страницBoston Creamery Caselion_heart3001100% (1)

- Sharing Sheet Hallstead JewelersДокумент11 страницSharing Sheet Hallstead JewelersHarpreet SinghОценок пока нет

- Anagene Case StudyДокумент1 страницаAnagene Case StudySam Man0% (3)

- Berkshire Toy Case - Calculation Groupe 4 18 FevДокумент9 страницBerkshire Toy Case - Calculation Groupe 4 18 FevchandrakumaranОценок пока нет

- Destin Brass Case AnalysisДокумент1 страницаDestin Brass Case Analysisfelipevwa100% (1)

- Wilkerson Company - Class PracticeДокумент5 страницWilkerson Company - Class PracticeYAKSH DODIAОценок пока нет

- Group 7 - Morrissey ForgingsДокумент10 страницGroup 7 - Morrissey ForgingsVishal AgarwalОценок пока нет

- Color ScopeДокумент10 страницColor Scopedharti_thakare100% (1)

- South Dakota Microbrewery CaseДокумент6 страницSouth Dakota Microbrewery Casecuruaxitin60% (5)

- Skyview Manor CaseДокумент3 страницыSkyview Manor CaseNisa SasyaОценок пока нет

- Case - SunAir Boat Builders Part - 2Документ3 страницыCase - SunAir Boat Builders Part - 2dhakar_ravi1Оценок пока нет

- A Case Analysis: Baldwin Bicycle CompanyДокумент12 страницA Case Analysis: Baldwin Bicycle CompanySamrat KaushikОценок пока нет

- Accounting Seligram CaseДокумент2 страницыAccounting Seligram CaseNadia Iqbal100% (1)

- Classic Pen Company: Syndicate 101Документ4 страницыClassic Pen Company: Syndicate 101Silvia WongОценок пока нет

- Case Case:: Colorscope, Colorscope, Inc. IncДокумент4 страницыCase Case:: Colorscope, Colorscope, Inc. IncBalvinder SinghОценок пока нет

- MANAC-II Assignment: by Abhinav Prusty - B19001 Hari Sankar S - B19018 Soham Ghosh - B19052Документ6 страницMANAC-II Assignment: by Abhinav Prusty - B19001 Hari Sankar S - B19018 Soham Ghosh - B19052harisankar sureshОценок пока нет

- ALKO Case StudyДокумент42 страницыALKO Case StudySuryakant KaushikОценок пока нет

- Sure Cut SheersДокумент7 страницSure Cut SheersEdward Marcell Basia67% (3)

- Sneaker Excel Sheet For Risk AnalysisДокумент11 страницSneaker Excel Sheet For Risk AnalysisSuperGuyОценок пока нет

- Reichard Maschinen, GMBHДокумент23 страницыReichard Maschinen, GMBHSasisomWilaiwanОценок пока нет

- 11 05 12 2022 Industrial Grinder ConclusionДокумент9 страниц11 05 12 2022 Industrial Grinder ConclusionPragathi SundarОценок пока нет

- Piston ManufacturingДокумент26 страницPiston Manufacturingrajeevigowda1720Оценок пока нет

- Industrial Grinders N VДокумент9 страницIndustrial Grinders N Vapi-250891173100% (3)

- Pwicase 170705202102Документ12 страницPwicase 170705202102Cristhian Gabriel Lizama ReynaОценок пока нет

- The Qualitative Descriptive ApproachДокумент4 страницыThe Qualitative Descriptive ApproachDesiSelviaОценок пока нет

- Markets For Factor InputsДокумент87 страницMarkets For Factor InputsDesiSelviaОценок пока нет

- Capitalization of R&D Costs and Earnings ManagementДокумент22 страницыCapitalization of R&D Costs and Earnings ManagementDesiSelviaОценок пока нет

- Case 1 Papa GinoДокумент2 страницыCase 1 Papa GinoDesiSelviaОценок пока нет

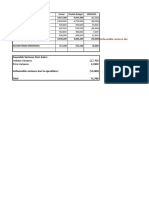

- Favorable Variance From Sales:: Volume Variance 117,700 Price Variance 12,000 (58,000)Документ2 страницыFavorable Variance From Sales:: Volume Variance 117,700 Price Variance 12,000 (58,000)DesiSelviaОценок пока нет

- Desi Selvia Nadhira Nayunda Yance Alexander: Kelompok 2Документ1 страницаDesi Selvia Nadhira Nayunda Yance Alexander: Kelompok 2DesiSelviaОценок пока нет

- Mnagement Control SystemsДокумент5 страницMnagement Control SystemsDesiSelviaОценок пока нет

- Case Chadwick QuestionsДокумент1 страницаCase Chadwick QuestionsDesiSelvia0% (1)

- Ma Lesson 04 Overhead CostДокумент23 страницыMa Lesson 04 Overhead CostDamith SarangaОценок пока нет

- Lecture 14 Audit of Specialised Industries 1 .Pptx-1Документ10 страницLecture 14 Audit of Specialised Industries 1 .Pptx-1cpale1filesОценок пока нет

- Ashutosh Dash: Management Accounting - An OverviewДокумент45 страницAshutosh Dash: Management Accounting - An OverviewRaghavendra NaduvinamaniОценок пока нет

- Estimating The Effect of Government Programs On Youth Entrepreneurship in The PhilippinesДокумент9 страницEstimating The Effect of Government Programs On Youth Entrepreneurship in The PhilippinesLovesickbut PrettysavageОценок пока нет

- Entrepreneurship Skills Question BankДокумент6 страницEntrepreneurship Skills Question BankNot LaffОценок пока нет

- BL 2 - Quiz On Corp.Документ2 страницыBL 2 - Quiz On Corp.Janna Mari FriasОценок пока нет

- Case 6Документ24 страницыCase 6Bella TjendriawanОценок пока нет

- MARICO Industries (Case Study)Документ15 страницMARICO Industries (Case Study)RajatОценок пока нет

- SERVICE SIMULATION - AirAsia-LatestДокумент32 страницыSERVICE SIMULATION - AirAsia-LatestSyed Muhd AmriОценок пока нет

- Banyan Tree Case StudyДокумент21 страницаBanyan Tree Case StudySarun ThitavasantaОценок пока нет

- Chapter 5Документ109 страницChapter 5JaiThra T JamesОценок пока нет

- Branding & Brand Management - Week1Документ20 страницBranding & Brand Management - Week1EvakzОценок пока нет

- The Concept of Business Environment, Significance andДокумент27 страницThe Concept of Business Environment, Significance andBhartendu Chaturvedi67% (9)

- Hul Sales and DistrubutionДокумент23 страницыHul Sales and DistrubutionKrishna Praveen PuliОценок пока нет

- Liquidation of CorporationДокумент15 страницLiquidation of CorporationMacie MenesesОценок пока нет

- Business EnviornmentДокумент55 страницBusiness EnviornmentAmit KumarОценок пока нет

- Chapter 5-Marketing Mix ElementsДокумент29 страницChapter 5-Marketing Mix Elementstemesgen yohannesОценок пока нет

- Customer Relationship Management (CRM) in HOTELДокумент22 страницыCustomer Relationship Management (CRM) in HOTELPritam Pritiman JenaОценок пока нет

- Ratio Analysis ParticipantsДокумент17 страницRatio Analysis ParticipantsDeepu MannatilОценок пока нет

- Fixed AssetДокумент11 страницFixed AssetmithafaramitaОценок пока нет

- Supplier PartnershipДокумент19 страницSupplier PartnershipMian Roshaan WasimОценок пока нет

- NETWORKSДокумент4 страницыNETWORKSCelestial Nicole VergañoОценок пока нет

- Management Advisory Services QuestionnaireДокумент12 страницManagement Advisory Services QuestionnaireSteven Mark MananguОценок пока нет

- Silage Final DPR 2023Документ24 страницыSilage Final DPR 2023K N GUPTAОценок пока нет

- Matching Internal Audit Talent To Organizational NeedsДокумент20 страницMatching Internal Audit Talent To Organizational NeedsEuglena Verde100% (1)

- A Study of Financial Derivatives (Futures and Options)Документ128 страницA Study of Financial Derivatives (Futures and Options)tanvirОценок пока нет