Вам также может понравиться

- NDT HandBook Volume 10 (NDT Overview)Документ600 страницNDT HandBook Volume 10 (NDT Overview)mahesh95% (19)

- Problem - PROFORMA BALANCE SHEET WITH CHOICE OF FINANCINGДокумент6 страницProblem - PROFORMA BALANCE SHEET WITH CHOICE OF FINANCINGJohn Richard Bonilla100% (4)

- Applied Group Fin Reporting-Changes in Group Structure PDFДокумент25 страницApplied Group Fin Reporting-Changes in Group Structure PDFObey SitholeОценок пока нет

- 1ST Term J1 Fine Art-1Документ22 страницы1ST Term J1 Fine Art-1Peter Omovigho Dugbo100% (1)

- A Sample Script For Public SpeakingДокумент2 страницыA Sample Script For Public Speakingalmasodi100% (2)

- Consolidation of Less-Than-Wholly Owned Subsidiaries: Mcgraw-Hill/IrwinДокумент40 страницConsolidation of Less-Than-Wholly Owned Subsidiaries: Mcgraw-Hill/IrwinahmedОценок пока нет

- Akl1 CH09Документ41 страницаAkl1 CH09Candini NoviantiОценок пока нет

- Online Ass Advance Acc NEWДокумент6 страницOnline Ass Advance Acc NEWRara Rarara30Оценок пока нет

- Principles of Consolidated Financial Statements Test Your Understanding 1Документ17 страницPrinciples of Consolidated Financial Statements Test Your Understanding 1sandeep gyawaliОценок пока нет

- C6-Intercompany Inventory Transactions PDFДокумент43 страницыC6-Intercompany Inventory Transactions PDFVico JulendiОценок пока нет

- Mid Year AcqusitionДокумент4 страницыMid Year AcqusitionOmolaja IbukunОценок пока нет

- Chapter FIVEДокумент14 страницChapter FIVEannisaОценок пока нет

- Chapter 5Документ17 страницChapter 5Belay MekonenОценок пока нет

- Study Unit Three Activity Ratios and Special IssuesДокумент11 страницStudy Unit Three Activity Ratios and Special IssuessimarjeetОценок пока нет

- Dave Chapter 9Документ11 страницDave Chapter 9Mark Dave SambranoОценок пока нет

- Review of Financial Statements and Its Analysis: Rheena B. Delos Santos BSBA-1A (FM2)Документ12 страницReview of Financial Statements and Its Analysis: Rheena B. Delos Santos BSBA-1A (FM2)RHIAN B.Оценок пока нет

- CorpoДокумент16 страницCorpoErica JoannaОценок пока нет

- Advanced ACCT PROJECT II FINAL DRAFTДокумент3 страницыAdvanced ACCT PROJECT II FINAL DRAFTnoureen sohailОценок пока нет

- Consolidation BasicsДокумент5 страницConsolidation Basicspoonamemrith22Оценок пока нет

- MGMT AssignmentДокумент79 страницMGMT AssignmentLuleseged Gebre100% (1)

- Introduction To GroupsДокумент15 страницIntroduction To GroupsTHOMAS ANSAHОценок пока нет

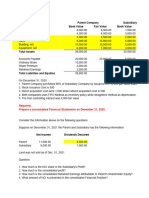

- Jan. 1, 20x1 Abc Co. XYZ, Inc.: Total Assets 670,000 160,000Документ5 страницJan. 1, 20x1 Abc Co. XYZ, Inc.: Total Assets 670,000 160,000Nathaniel IgotОценок пока нет

- Final RequirementДокумент18 страницFinal RequirementZandra GonzalesОценок пока нет

- Lecture 4-PostДокумент40 страницLecture 4-PostcoolirlbbОценок пока нет

- AcFN 3151 CH, 5 CONSOLIDATED FINANCIAL STATEMENTS IFRS 10Документ41 страницаAcFN 3151 CH, 5 CONSOLIDATED FINANCIAL STATEMENTS IFRS 10BethelhemОценок пока нет

- Assignment 1Документ5 страницAssignment 1Loveness MphandeОценок пока нет

- Chapter 3 - Consolidated Statements: Subsequent To AcquisitionДокумент36 страницChapter 3 - Consolidated Statements: Subsequent To AcquisitionJean De GuzmanОценок пока нет

- Sample Financial Management ProblemsДокумент8 страницSample Financial Management ProblemsJasper Andrew AdjaraniОценок пока нет

- Dewi Nabilah Anwar - Akl1 Week 2Документ3 страницыDewi Nabilah Anwar - Akl1 Week 2Soe BagyoОценок пока нет

- Unit 3Документ13 страницUnit 3hassan19951996hОценок пока нет

- Consolidation PartBДокумент29 страницConsolidation PartBHuzaifa AhmedОценок пока нет

- GEN4Документ7 страницGEN4Mylene HeragaОценок пока нет

- Study Unit Eight Activity Measures and FinancingДокумент15 страницStudy Unit Eight Activity Measures and FinancingPaul LteifОценок пока нет

- Chapter 12 ProblemsДокумент40 страницChapter 12 ProblemsInciaОценок пока нет

- Corporate Finance Practice Problems: Jeter Corporation Income Statement For The Year Ended 31, 2001Документ9 страницCorporate Finance Practice Problems: Jeter Corporation Income Statement For The Year Ended 31, 2001Eunice NanaОценок пока нет

- Buscom - Subsequent-To-The-Date-Of-Acquisition - Cost MethodДокумент46 страницBuscom - Subsequent-To-The-Date-Of-Acquisition - Cost MethodJohn Stephen PendonОценок пока нет

- Accounting 2 - Chapter 14 - Notes - MiuДокумент4 страницыAccounting 2 - Chapter 14 - Notes - MiuAhmad Osama MashalyОценок пока нет

- Akl Soal 3 Kelompok 2Документ9 страницAkl Soal 3 Kelompok 2dikaОценок пока нет

- Akl Soal 3 - Kelompok 2Документ9 страницAkl Soal 3 - Kelompok 2M KhairiОценок пока нет

- Exercise For Financial Statement Analysis and RatiosДокумент15 страницExercise For Financial Statement Analysis and RatiosViren JoshiОценок пока нет

- Intercompany Profit Transactions - InventoriesДокумент35 страницIntercompany Profit Transactions - InventorieseferemОценок пока нет

- HW5.FT222004.Archit KumarДокумент7 страницHW5.FT222004.Archit KumarARCHIT KUMARОценок пока нет

- Purchase Price and Implied Value Less: Book Value of Equity Acquired: Difference Beetwen Implied and Book Value Record New Goodwil BalanceДокумент14 страницPurchase Price and Implied Value Less: Book Value of Equity Acquired: Difference Beetwen Implied and Book Value Record New Goodwil BalancesallyОценок пока нет

- Tutorial 6 With Solutions-Long-Term Debt-Paying Ability and ProfitabilityДокумент5 страницTutorial 6 With Solutions-Long-Term Debt-Paying Ability and ProfitabilityGing freexОценок пока нет

- Acca110 Adorable Ac21 As03Документ6 страницAcca110 Adorable Ac21 As03Shaneen AdorableОценок пока нет

- Comprehensive Illustration of Consolidated Financial Statements - Intercompany Sale of Inventories PDFДокумент9 страницComprehensive Illustration of Consolidated Financial Statements - Intercompany Sale of Inventories PDFamie honnagОценок пока нет

- Lape - ACP312 - ULOa - Let's Analyze Week6Документ3 страницыLape - ACP312 - ULOa - Let's Analyze Week6Bryle Jay LapeОценок пока нет

- Beams9esm Ch01Документ13 страницBeams9esm Ch01zandra SumbarОценок пока нет

- Kelompok 6 - UTS AKMДокумент18 страницKelompok 6 - UTS AKM21-010 Desi MailaniОценок пока нет

- Practice ProblemsДокумент7 страницPractice ProblemsJOJKOОценок пока нет

- Chapter 4 - Consolidated Financial Statements (Part 1)Документ32 страницыChapter 4 - Consolidated Financial Statements (Part 1)Philip RososОценок пока нет

- RATIO QuestionsДокумент5 страницRATIO QuestionsikkaОценок пока нет

- 1130 - 89 - Tugas Pribadi Akl Pertemuan 9 Dan 11Документ9 страниц1130 - 89 - Tugas Pribadi Akl Pertemuan 9 Dan 11Maulana AmriОценок пока нет

- Additional Consolidation Reporting IssuesДокумент61 страницаAdditional Consolidation Reporting IssuesDifaОценок пока нет

- Cash Flow Analysis: Mcgraw-Hill/Irwin © 2004 The Mcgraw-Hill Companies, Inc., All Rights ReservedДокумент27 страницCash Flow Analysis: Mcgraw-Hill/Irwin © 2004 The Mcgraw-Hill Companies, Inc., All Rights Reservedmabkhan_25Оценок пока нет

- FS Consolidation at The Date of Acquisition v2Документ16 страницFS Consolidation at The Date of Acquisition v2Pagatpat, Apple Grace C.Оценок пока нет

- Buscom Subsequent MeasurementДокумент6 страницBuscom Subsequent MeasurementCarmela BautistaОценок пока нет

- 1 - Advanced Financial Accounting Individual Assignment IДокумент6 страниц1 - Advanced Financial Accounting Individual Assignment IEyasuОценок пока нет

- Single Entry MethodДокумент6 страницSingle Entry MethodNhel AlvaroОценок пока нет

- Solution Manual For Advanced Accounting 11th Edition by Beams 3 PDF FreeДокумент14 страницSolution Manual For Advanced Accounting 11th Edition by Beams 3 PDF Freeluxion bot100% (1)

- F7.2 - Mock Test 1Документ5 страницF7.2 - Mock Test 1huusinh2402Оценок пока нет

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsОт EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsОценок пока нет

- CHP 3Документ8 страницCHP 3richelledelgadoОценок пока нет

- Chapter 15Документ17 страницChapter 15richelledelgadoОценок пока нет

- Chap 2 Tax Admin2013Документ10 страницChap 2 Tax Admin2013Quennie Jane Siblos100% (1)

- Chap 1 Gen. Prin 2013Документ3 страницыChap 1 Gen. Prin 2013Quennie Jane Siblos100% (6)

- Reviewer Endterm Rizal Chapters 19 To 25Документ9 страницReviewer Endterm Rizal Chapters 19 To 25Diana Lyn SinfuegoОценок пока нет

- Working Capital FinanceДокумент12 страницWorking Capital FinanceYeoh Mae100% (4)

- Chap 4 Gross Income2013Документ11 страницChap 4 Gross Income2013Quennie Jane Siblos89% (9)

- Group 2.. Business Ethics...Документ22 страницыGroup 2.. Business Ethics...richelledelgado50% (2)

- Feasibility StudyДокумент17 страницFeasibility StudyHazelle CarmeloОценок пока нет

- Chapter 2Документ25 страницChapter 2Ronalyn EscamillasОценок пока нет

- Chapter 2Документ25 страницChapter 2Ronalyn EscamillasОценок пока нет

- Chapter 2Документ25 страницChapter 2Ronalyn EscamillasОценок пока нет

- Wholly Owned REPORTДокумент46 страницWholly Owned REPORTrichelledelgadoОценок пока нет

- Advanced Accounting 2 Consolidated Fs - MY ReportДокумент52 страницыAdvanced Accounting 2 Consolidated Fs - MY ReportrichelledelgadoОценок пока нет

- Advanced Accounting 2 Consolidated Fs - MY ReportДокумент52 страницыAdvanced Accounting 2 Consolidated Fs - MY ReportrichelledelgadoОценок пока нет

- Consolidated FS Subsequent To Date of Purchase TypeДокумент158 страницConsolidated FS Subsequent To Date of Purchase TypeSassy OcampoОценок пока нет

- Rresearch PPPPPДокумент9 страницRresearch PPPPPAiza DelgadoОценок пока нет

- Wholly Owned REPORTДокумент46 страницWholly Owned REPORTrichelledelgadoОценок пока нет

- Rresearch PPPPPДокумент9 страницRresearch PPPPPAiza DelgadoОценок пока нет

- Less Than Wholly Owned REPORTДокумент40 страницLess Than Wholly Owned REPORTrichelledelgadoОценок пока нет

- Advanced Accounting 2 Consolidated FsДокумент90 страницAdvanced Accounting 2 Consolidated FsrichelledelgadoОценок пока нет

- CHAPTER 2..ritchelle DelgadoДокумент34 страницыCHAPTER 2..ritchelle DelgadorichelledelgadoОценок пока нет

- CHAPTER 2..ritchelle Delgado.1Документ39 страницCHAPTER 2..ritchelle Delgado.1richelledelgadoОценок пока нет

- Chapter 2Документ25 страницChapter 2Ronalyn EscamillasОценок пока нет

- 5 CompaniesДокумент24 страницы5 CompaniesrichelledelgadoОценок пока нет

- Advanced Accounting 2 Consolidated Fs - MY ReportДокумент52 страницыAdvanced Accounting 2 Consolidated Fs - MY ReportrichelledelgadoОценок пока нет

- 07 Intro ERP Using GBI Case Study FI (Letter) en v2.11Документ17 страниц07 Intro ERP Using GBI Case Study FI (Letter) en v2.11richelledelgadoОценок пока нет

- 15 Toughest Interview Questions and Answers!: 1. Why Do You Want To Work in This Industry?Документ8 страниц15 Toughest Interview Questions and Answers!: 1. Why Do You Want To Work in This Industry?johnlemОценок пока нет

- 07 Intro ERP Using GBI Case Study FI (Letter) en v2.11Документ17 страниц07 Intro ERP Using GBI Case Study FI (Letter) en v2.11richelledelgadoОценок пока нет

- Genie PDFДокумент264 страницыGenie PDFjohanaОценок пока нет

- TV Antenna Tower CollapseДокумент4 страницыTV Antenna Tower CollapseImdaad ChuubbОценок пока нет

- Balinghasay V CastilloДокумент1 страницаBalinghasay V CastilloMirella100% (3)

- Portfolio Write-UpДокумент4 страницыPortfolio Write-UpJonFromingsОценок пока нет

- EC105Документ14 страницEC105api-3853441Оценок пока нет

- Operation of A CRT MonitorДокумент8 страницOperation of A CRT MonitorHarry W. HadelichОценок пока нет

- MFD16I003 FinalДокумент16 страницMFD16I003 FinalAditya KumarОценок пока нет

- O Repensar Da Fonoaudiologia Na Epistemologia CienДокумент5 страницO Repensar Da Fonoaudiologia Na Epistemologia CienClaudilla L.Оценок пока нет

- 3.2.1 The Role of Market Research and Methods UsedДокумент42 страницы3.2.1 The Role of Market Research and Methods Usedsana jaleelОценок пока нет

- API IND DS2 en Excel v2 10081834Документ462 страницыAPI IND DS2 en Excel v2 10081834Suvam PatelОценок пока нет

- Basic Knowledge About WDM Principle AДокумент92 страницыBasic Knowledge About WDM Principle AJosé LópezОценок пока нет

- USA Nozzle 01Документ2 страницыUSA Nozzle 01Justin MercadoОценок пока нет

- Encapsulation of Objects and Methods in C++Документ46 страницEncapsulation of Objects and Methods in C++Scott StanleyОценок пока нет

- Pell (2017) - Trends in Real-Time Traffic SimulationДокумент8 страницPell (2017) - Trends in Real-Time Traffic SimulationJorge OchoaОценок пока нет

- Blank FacebookДокумент2 страницыBlank Facebookapi-355481535Оценок пока нет

- CAMEL Model With Detailed Explanations and Proper FormulasДокумент4 страницыCAMEL Model With Detailed Explanations and Proper FormulasHarsh AgarwalОценок пока нет

- ERP22006Документ1 страницаERP22006Ady Surya LesmanaОценок пока нет

- Acc 106 Account ReceivablesДокумент40 страницAcc 106 Account ReceivablesAmirah NordinОценок пока нет

- I. Objectives:: Semi-Detailed Lesson Plan in Reading and Writing (Grade 11)Документ5 страницI. Objectives:: Semi-Detailed Lesson Plan in Reading and Writing (Grade 11)Shelton Lyndon CemanesОценок пока нет

- Practical Applications of Electrical ConductorsДокумент12 страницPractical Applications of Electrical ConductorsHans De Keulenaer100% (5)

- Credit Risk ManagementДокумент64 страницыCredit Risk Managementcherry_nu100% (12)

- Intergard 475HS - Part B - EVA046 - GBR - ENG PDFДокумент10 страницIntergard 475HS - Part B - EVA046 - GBR - ENG PDFMohamed NouzerОценок пока нет

- Javascript NotesДокумент5 страницJavascript NotesRajashekar PrasadОценок пока нет

- Gothic ArchitectureДокумент6 страницGothic ArchitectureleeОценок пока нет

- Session 1: Strategic Marketing - Introduction & ScopeДокумент38 страницSession 1: Strategic Marketing - Introduction & ScopeImrul Hasan ChowdhuryОценок пока нет

- M.T Nautica Batu Pahat: Clean Product Tanker 4,497 BHPДокумент1 страницаM.T Nautica Batu Pahat: Clean Product Tanker 4,497 BHPSuper 247Оценок пока нет

- Cutler Hammer Dry Type TransformerДокумент220 страницCutler Hammer Dry Type TransformernprajanОценок пока нет