Вам также может понравиться

- Contact Center NG BayanДокумент7 страницContact Center NG BayanSulong Pinas JRОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Spin SellingДокумент45 страницSpin SellingKammie100% (15)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Standard Costing ProblemsДокумент16 страницStandard Costing ProblemsSanket PanwalkarОценок пока нет

- TMC Car Rental ProposalДокумент16 страницTMC Car Rental ProposalMazlan Mp100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Accounting-2009 Resit ExamДокумент18 страницAccounting-2009 Resit ExammasterURОценок пока нет

- Deferred COGS Accounting in R12Документ3 страницыDeferred COGS Accounting in R12Ramesh GarikapatiОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- MKT 558 (Section 2) : Pricing Strategies: Eastman Kodak Company: Funtime FilmДокумент7 страницMKT 558 (Section 2) : Pricing Strategies: Eastman Kodak Company: Funtime FilmShreeraj PawarОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Research Methodology For Impulse Buying BehaviorДокумент3 страницыResearch Methodology For Impulse Buying Behaviorkunalatwork89Оценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Distance ModeДокумент152 страницыDistance Modevaidykarthik100% (3)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- MMBC-Group 7Документ12 страницMMBC-Group 7Shashank BaranwalОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Sales.07.Nietes V CAДокумент3 страницыSales.07.Nietes V CAQuina IgnacioОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Bhogadi Road Near Birihundi Yesh Valley View LAYOUT - MysoreДокумент3 страницыBhogadi Road Near Birihundi Yesh Valley View LAYOUT - MysoreRanjan Patali JanardhanaОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Swot SoftДокумент33 страницыSwot Softpurva_pitre100% (1)

- Presentation MerchandiserДокумент11 страницPresentation MerchandisersujanОценок пока нет

- A Comparative Analysis of Sport and Business OrganizationsДокумент17 страницA Comparative Analysis of Sport and Business OrganizationsRonnieОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- TOP 20 Method To Make Money OnlineДокумент24 страницыTOP 20 Method To Make Money Onlinekatet82% (11)

- Economics TestДокумент52 страницыEconomics TestWarwick PangilinanОценок пока нет

- Operations ExecutionДокумент18 страницOperations ExecutionFrank Viale100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- MarkatingДокумент220 страницMarkatingchuchu100% (1)

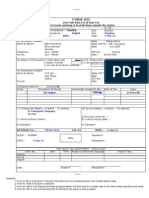

- Form 403 of Gujarat VAT For Goods Purchased Outside State and Brining in To GujaratДокумент1 страницаForm 403 of Gujarat VAT For Goods Purchased Outside State and Brining in To GujaratVeer Patel100% (1)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Price List For CAREДокумент2 страницыPrice List For CARESaurabh SrivastavaОценок пока нет

- Enquiry and Its Reply !Документ5 страницEnquiry and Its Reply !Mohammed Amine DoudouzОценок пока нет

- Consumer Buying Behaviour in Automobile Industry-A Consumer Perception-LibreДокумент50 страницConsumer Buying Behaviour in Automobile Industry-A Consumer Perception-LibreManish Manjhi69% (13)

- GMAT Prep ProblemsДокумент45 страницGMAT Prep ProblemsAli BhattiОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Warehouse Receipt LawДокумент25 страницWarehouse Receipt LawFaye Cience BoholОценок пока нет

- Omron - MK0607-1189905Документ11 страницOmron - MK0607-1189905Pedro Tavares MurakameОценок пока нет

- Chapter 20 - VATДокумент14 страницChapter 20 - VATrottelosОценок пока нет

- MDM4U Binomial Distributions WorksheetДокумент10 страницMDM4U Binomial Distributions WorksheetGqn GanОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- ProductДокумент65 страницProductMarielou Cruz ManglicmotОценок пока нет

- Body ShopДокумент7 страницBody ShopBani KaneОценок пока нет