Вам также может понравиться

- Accounting 1 Review QuizДокумент6 страницAccounting 1 Review QuizAikalyn MangubatОценок пока нет

- Materials ManagementДокумент41 страницаMaterials ManagementDarshak Gowda100% (1)

- CH 4 Materials ManagementДокумент67 страницCH 4 Materials ManagementSolomon Dufera67% (3)

- 5 Psychological Theories of Motivation To Increase ProductivityДокумент15 страниц5 Psychological Theories of Motivation To Increase ProductivityNaveen Jacob JohnОценок пока нет

- Sara - Stitch Fix BrochureДокумент2 страницыSara - Stitch Fix Brochureapi-456333887Оценок пока нет

- Integrated Materials Management: Dr. D.T.Manwani Professor & HeadДокумент34 страницыIntegrated Materials Management: Dr. D.T.Manwani Professor & HeadAmitsinh ViholОценок пока нет

- Materials Management Short NoteДокумент4 страницыMaterials Management Short NoteWorku Chanie Abey100% (1)

- Lesson 4 - Material ManagementДокумент31 страницаLesson 4 - Material ManagementRose DetaloОценок пока нет

- Integrated Material Management - CondensedДокумент34 страницыIntegrated Material Management - CondensedPravin TambeОценок пока нет

- Meaning of Purchasing ManagementДокумент10 страницMeaning of Purchasing ManagementZAKAYO NJONYОценок пока нет

- Chapter 4 - Material ManagementДокумент15 страницChapter 4 - Material ManagementRohit BadgujarОценок пока нет

- Unit-Iv: The Sourcing DecisionsДокумент31 страницаUnit-Iv: The Sourcing DecisionsGangadhara Rao100% (1)

- 4_5918246878398387080Документ4 страницы4_5918246878398387080oromiamammitoo444Оценок пока нет

- Materials Management: Dr. K. K. Saju Professor Division of Mechanical Engineering Soe, CusatДокумент78 страницMaterials Management: Dr. K. K. Saju Professor Division of Mechanical Engineering Soe, CusatRitwik AravindОценок пока нет

- MLM 0001Документ52 страницыMLM 0001amit01dubeyОценок пока нет

- PurchasingmanagementДокумент20 страницPurchasingmanagementlalitha kandikaОценок пока нет

- Unit 3.1 - Materials ManagementДокумент58 страницUnit 3.1 - Materials Managementlamao123Оценок пока нет

- Material and Store Management:: Introduction, Objectives and FunctionsДокумент21 страницаMaterial and Store Management:: Introduction, Objectives and FunctionsStephane chisebweОценок пока нет

- Chapter IV Material ManagementДокумент22 страницыChapter IV Material ManagementFiraaОценок пока нет

- Unit V: Materials Management-ObjectivesДокумент8 страницUnit V: Materials Management-ObjectivesSunkeswaram Deva PrasadОценок пока нет

- Pharmaceutical Industry Management GuideДокумент38 страницPharmaceutical Industry Management GuideUmair MazharОценок пока нет

- MATERIAL MANAGEMENT SEMINARДокумент75 страницMATERIAL MANAGEMENT SEMINARvinnu kalyanОценок пока нет

- Module 2Документ19 страницModule 2sarojkumardasbsetОценок пока нет

- PRE572 OgbeideДокумент22 страницыPRE572 OgbeideChukwudi DesmondОценок пока нет

- Construction Materials Management TechniquesДокумент146 страницConstruction Materials Management Techniquesmatrixworld20Оценок пока нет

- Unit-4 Material ManagementДокумент27 страницUnit-4 Material ManagementMubin Shaikh NooruОценок пока нет

- Principles of Procurement notesДокумент58 страницPrinciples of Procurement notesvincent nemadzivaОценок пока нет

- Supply Chain Management T1-T4Документ8 страницSupply Chain Management T1-T4Krystelle MayaОценок пока нет

- Seminar On Material Management: Mrs. Harpreet Kaur, MSC Nursing 2 Year Nims College of Nursing Nims University, JaipurДокумент72 страницыSeminar On Material Management: Mrs. Harpreet Kaur, MSC Nursing 2 Year Nims College of Nursing Nims University, JaipurihbrusansuharshОценок пока нет

- Material ManagementДокумент34 страницыMaterial ManagementQurat Ul Ain NaqviОценок пока нет

- Materials Management WeekДокумент41 страницаMaterials Management WeekVaishnavi KrushakthiОценок пока нет

- Bba PM 4 BДокумент20 страницBba PM 4 BJyoti SinghОценок пока нет

- Material Management Scope and Functions Explained in 40 CharactersДокумент8 страницMaterial Management Scope and Functions Explained in 40 CharactersNavjot SinghОценок пока нет

- Unit III - Materials ManagementДокумент55 страницUnit III - Materials ManagementSumiksh ManhasОценок пока нет

- Topic 1 Purchasing and Supplies ManagementДокумент13 страницTopic 1 Purchasing and Supplies Managementtashabriana86Оценок пока нет

- Chapter - 7Документ33 страницыChapter - 7Arifur Rahman MSquareОценок пока нет

- Chap .1 PurchasingДокумент39 страницChap .1 Purchasingakshay jadhavОценок пока нет

- Company's $50k purchase processДокумент14 страницCompany's $50k purchase processNoman KhanОценок пока нет

- Materials Management Two MarksДокумент7 страницMaterials Management Two Marksmarimuthu96Оценок пока нет

- Chapter 4Документ57 страницChapter 4mОценок пока нет

- SCM (U5)Документ15 страницSCM (U5)Badal RoyОценок пока нет

- Operations Management 2Документ39 страницOperations Management 2BalujagadishОценок пока нет

- Supply Chain Operations: Planning and Sourcing: Chapter - 2Документ20 страницSupply Chain Operations: Planning and Sourcing: Chapter - 2Vinay VarmaОценок пока нет

- Man L6Документ34 страницыMan L6Vaibhav GoleОценок пока нет

- Unit Iv Materials ManagementДокумент4 страницыUnit Iv Materials ManagementmkddanОценок пока нет

- Chapter 4 BMAD - Purchasing 2018Документ30 страницChapter 4 BMAD - Purchasing 2018zina minaОценок пока нет

- MATERIALS MANAGEMENT OVERVIEWДокумент55 страницMATERIALS MANAGEMENT OVERVIEWKEVIN MUTURIОценок пока нет

- Materials Management Unit 5ert (3) 567 (1) 2343Документ59 страницMaterials Management Unit 5ert (3) 567 (1) 2343Mohammed AneesОценок пока нет

- Materials Management Chapter 4 Key ConceptsДокумент36 страницMaterials Management Chapter 4 Key ConceptsEftaОценок пока нет

- Materials ManagementДокумент52 страницыMaterials ManagementakulavarshiniОценок пока нет

- SCM ch05Документ84 страницыSCM ch05Hasan RazaОценок пока нет

- Debritu AssignДокумент5 страницDebritu Assigngetamesay assefaОценок пока нет

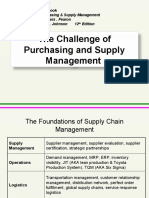

- The Challenge of Purchasing and Supply ManagementДокумент48 страницThe Challenge of Purchasing and Supply ManagementWaseem Ahmed HingorjoОценок пока нет

- Material Managemnt: From The Management Point of View, The Key Objectives of MM AreДокумент11 страницMaterial Managemnt: From The Management Point of View, The Key Objectives of MM ArejoeyОценок пока нет

- Materials Management: SyllabusДокумент10 страницMaterials Management: SyllabusEmerald InnovatesОценок пока нет

- Purchasing and Vendor Management Lecture 6Документ34 страницыPurchasing and Vendor Management Lecture 6dinesh9936115534100% (4)

- AssignmentДокумент5 страницAssignmentibraheemumarОценок пока нет

- Materials ManagementДокумент12 страницMaterials ManagementNitin danuОценок пока нет

- Material Management PDFДокумент76 страницMaterial Management PDFMohammedNaveenОценок пока нет

- Supply Chain and Procurement Quick Reference: How to navigate and be successful in structured organizationsОт EverandSupply Chain and Procurement Quick Reference: How to navigate and be successful in structured organizationsОценок пока нет

- Classification of Entrepreneurs According To The Type of Busines1Документ25 страницClassification of Entrepreneurs According To The Type of Busines1Naveen Jacob John100% (1)

- Commerce Degree Program Covers Business, Accounting & Computer SkillsДокумент54 страницыCommerce Degree Program Covers Business, Accounting & Computer SkillsNaveen Jacob JohnОценок пока нет

- Answer All Questions. Each Carries 1 Mark: Section AДокумент2 страницыAnswer All Questions. Each Carries 1 Mark: Section ANaveen Jacob JohnОценок пока нет

- Foreign ExchangeДокумент18 страницForeign ExchangeNaveen Jacob JohnОценок пока нет

- Economic Order Quantity (EOQ) - Encyclopedia - Business Terms - IncДокумент2 страницыEconomic Order Quantity (EOQ) - Encyclopedia - Business Terms - IncNaveen Jacob JohnОценок пока нет

- My QuestionnaireДокумент4 страницыMy QuestionnaireNaveen Jacob JohnОценок пока нет

- 1 2econ IntegrДокумент2 страницы1 2econ IntegrNaveen Jacob JohnОценок пока нет

- Exchange Rate Regime Article - Final (With Comments) (2) DraftДокумент3 страницыExchange Rate Regime Article - Final (With Comments) (2) DraftNaveen Jacob JohnОценок пока нет

- ASEAN-Integration, Internal Dynamics External RelationsДокумент25 страницASEAN-Integration, Internal Dynamics External RelationsKrizea Marie DuronОценок пока нет

- Module 5Документ5 страницModule 5Naveen Jacob JohnОценок пока нет

- Your Order IDДокумент1 страницаYour Order IDNaveen Jacob JohnОценок пока нет

- International Business Environment PDFДокумент298 страницInternational Business Environment PDFHarmeet AnandОценок пока нет

- Framework For Analysing International Business EnvironmentДокумент15 страницFramework For Analysing International Business EnvironmentNaveen Jacob JohnОценок пока нет

- EntrepreneurshipДокумент87 страницEntrepreneurshipvinodyadav043Оценок пока нет

- Characteristics of Small and Medium Enterprise InnovativenessДокумент16 страницCharacteristics of Small and Medium Enterprise InnovativenessNaveen Jacob JohnОценок пока нет

- Types of EntrepreneursДокумент2 страницыTypes of EntrepreneursHamadОценок пока нет

- Economic Integration TheoryДокумент32 страницыEconomic Integration TheoryNaveen Jacob JohnОценок пока нет

- Calculating Compound Interest by HandДокумент3 страницыCalculating Compound Interest by HandNaveen Jacob JohnОценок пока нет

- Economic Integration Is An Agreement Among Countries in A Geographic Region To Reduce and Ultimately RemoveДокумент2 страницыEconomic Integration Is An Agreement Among Countries in A Geographic Region To Reduce and Ultimately RemoveNaveen Jacob JohnОценок пока нет

- Introduction To Materials Management: Chapter 4 - Material Requirements PlanningДокумент33 страницыIntroduction To Materials Management: Chapter 4 - Material Requirements PlanningNaveen Jacob JohnОценок пока нет

- ASEAN-Integration, Internal Dynamics External RelationsДокумент25 страницASEAN-Integration, Internal Dynamics External RelationsKrizea Marie DuronОценок пока нет

- Module 5Документ8 страницModule 5Naveen Jacob JohnОценок пока нет

- Department of Commerce, Mar Thoma College of Science & Technology, AyurДокумент7 страницDepartment of Commerce, Mar Thoma College of Science & Technology, AyurNaveen Jacob JohnОценок пока нет

- Career Options after 12th Commerce, what to do after 12th Commerce, Career_ educational chart, career planning, Career Options after +2_ plus two_ intermediate with Commerce, career opportunities after 12thДокумент3 страницыCareer Options after 12th Commerce, what to do after 12th Commerce, Career_ educational chart, career planning, Career Options after +2_ plus two_ intermediate with Commerce, career opportunities after 12thNaveen Jacob JohnОценок пока нет

- Business EnvironmentДокумент20 страницBusiness EnvironmentNaveen Jacob JohnОценок пока нет

- Materials Management Systems: Physical DistributionДокумент17 страницMaterials Management Systems: Physical DistributionNaveen Jacob JohnОценок пока нет

- Classical and Modern Management Approaches and Techniques in Public Administration - Patterns and TrendsInternational Review of Administrative Sciences - Faqir Muhammad, 1978Документ3 страницыClassical and Modern Management Approaches and Techniques in Public Administration - Patterns and TrendsInternational Review of Administrative Sciences - Faqir Muhammad, 1978Naveen Jacob JohnОценок пока нет

- Functions of National Small Industries Corporation (NSIC)Документ14 страницFunctions of National Small Industries Corporation (NSIC)Naveen Jacob JohnОценок пока нет

- Capital Market Multiple Choice Questions and Answers ListДокумент3 страницыCapital Market Multiple Choice Questions and Answers Listskills9tanish0% (1)

- Dev Academy of Science and Commerce March Examination 12 EconomicsДокумент2 страницыDev Academy of Science and Commerce March Examination 12 Economicsरजत जाँगडाОценок пока нет

- Analyzing Uber's Profitability with Porter's Five ForcesДокумент2 страницыAnalyzing Uber's Profitability with Porter's Five ForcesMikey ChuaОценок пока нет

- Martin Jones & Nancy Cartwright (Eds. 2005) - Idealization Xii - Correcting The Model - Idealization and AbstractionДокумент305 страницMartin Jones & Nancy Cartwright (Eds. 2005) - Idealization Xii - Correcting The Model - Idealization and Abstractionmilutin1987100% (2)

- Inventory KPI - SAP TransactionsДокумент3 страницыInventory KPI - SAP TransactionsGabrielОценок пока нет

- SIBM Bangalore Retail ManagementДокумент4 страницыSIBM Bangalore Retail ManagementPrateek AryaОценок пока нет

- Economy Questions in Upsc Prelims 2022 88Документ6 страницEconomy Questions in Upsc Prelims 2022 88RamdulariОценок пока нет

- Parle G Commands 65% Market Share in India's Rs 15 Billion Glucose Biscuits CategoryДокумент6 страницParle G Commands 65% Market Share in India's Rs 15 Billion Glucose Biscuits CategoryMithil Kotwal100% (1)

- Impact of GST on Indian FMCG SectorДокумент42 страницыImpact of GST on Indian FMCG SectorManthanОценок пока нет

- Practice Bonds and Stocks ProblemsДокумент6 страницPractice Bonds and Stocks ProblemsKevin DayanОценок пока нет

- Apr Form No. 02Документ4 страницыApr Form No. 02Bobbie KasandraОценок пока нет

- Strategic Entrepreneurship in Emerging Market Multinationals-Marco Polo MarineДокумент14 страницStrategic Entrepreneurship in Emerging Market Multinationals-Marco Polo MarineIftekhar KhanОценок пока нет

- Dokumen - Tips 128057344 Chapter 2Документ70 страницDokumen - Tips 128057344 Chapter 2GianJoshuaDayritОценок пока нет

- IS-LM Model ExplainedДокумент36 страницIS-LM Model ExplainedSyed Ali Zain100% (1)

- NestleДокумент60 страницNestlesara24391Оценок пока нет

- The New Normal Case Study TFC ScribdДокумент2 страницыThe New Normal Case Study TFC ScribdTasneemОценок пока нет

- Producer's Equilibrium ExplainedДокумент14 страницProducer's Equilibrium Explainedrohitbatra100% (1)

- Unit - 3 Trade CycleДокумент9 страницUnit - 3 Trade CycleTARAL PATELОценок пока нет

- Ishfaq Data Analysis and InterpretationДокумент25 страницIshfaq Data Analysis and InterpretationJamie Price100% (2)

- TCS Recruitment Previous Year Pattern Questions Set-9Документ2 страницыTCS Recruitment Previous Year Pattern Questions Set-9QUANT ADDAОценок пока нет

- This Study Resource Was: PAS 2 InventoriesДокумент3 страницыThis Study Resource Was: PAS 2 Inventorieshsjhs100% (1)

- National Highways Authority of ... Vs Patel KNR (JV) On 14 May, 2018Документ14 страницNational Highways Authority of ... Vs Patel KNR (JV) On 14 May, 2018SarinОценок пока нет

- Chapter 9 SolutionsДокумент7 страницChapter 9 SolutionsRose McMahon50% (2)

- Business Blue PrintДокумент65 страницBusiness Blue PrintImtiaz KhanОценок пока нет

- Role of Insurance in Bangladesh's EconomyДокумент4 страницыRole of Insurance in Bangladesh's EconomyAsim Mandal60% (5)

- Competition Law Critical AnalysisДокумент6 страницCompetition Law Critical AnalysisGeetika AnandОценок пока нет

- Manage Inventory Costs with EOQ ModelsДокумент30 страницManage Inventory Costs with EOQ ModelsGopi SОценок пока нет

- Budget and B Udgetary C OntrolДокумент6 страницBudget and B Udgetary C OntrolKanika DahiyaОценок пока нет