Вам также может понравиться

- Bank DetailsДокумент3 страницыBank DetailsHuỳnh Hồng Hanh0% (1)

- Nielsen Esports Playbook For Brands 2019Документ28 страницNielsen Esports Playbook For Brands 2019Jean-Louis ManzonОценок пока нет

- Construction Measures - Key Performance IndicatorsДокумент21 страницаConstruction Measures - Key Performance IndicatorsBusi_Selesho100% (1)

- ISO 9001 QuizДокумент4 страницыISO 9001 QuizGVS Rao0% (1)

- Financial Statements and Ratio Analysis NEWДокумент108 страницFinancial Statements and Ratio Analysis NEWDina Adel DawoodОценок пока нет

- Ratio-Analysis of ITCДокумент56 страницRatio-Analysis of ITCVinod71% (7)

- Jewelry ManufacturingДокумент18 страницJewelry ManufacturingHuỳnh Hồng HanhОценок пока нет

- Intro To LodgingДокумент63 страницыIntro To LodgingjaevendОценок пока нет

- History of Architecture VI: Unit 1Документ20 страницHistory of Architecture VI: Unit 1Srehari100% (1)

- Court Documents From Toronto Police Project Brazen - Investigation of Alexander "Sandro" Lisi and Toronto Mayor Rob FordДокумент474 страницыCourt Documents From Toronto Police Project Brazen - Investigation of Alexander "Sandro" Lisi and Toronto Mayor Rob Fordanna_mehler_papernyОценок пока нет

- Floating PonttonДокумент9 страницFloating PonttonToniОценок пока нет

- Lecture 10 Life Cycle CostingДокумент46 страницLecture 10 Life Cycle CostingKHAIRIEL IZZAT AZMANОценок пока нет

- The Nation State and Global Order A Historical Introduction To ContemporaryДокумент195 страницThe Nation State and Global Order A Historical Introduction To Contemporaryrizwan.mughal1997100% (1)

- Internal Control of Fixed Assets: A Controller and Auditor's GuideОт EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideРейтинг: 4 из 5 звезд4/5 (1)

- Chapter 2Документ49 страницChapter 2Võ Thị Mỹ DuyênОценок пока нет

- Chapter 2 - 1Документ49 страницChapter 2 - 1trịnh thị quỳnhОценок пока нет

- PrelimДокумент8 страницPrelimEllah MaeОценок пока нет

- Chapter 16 Working Capital ManagementДокумент11 страницChapter 16 Working Capital ManagementAnaОценок пока нет

- (FMDFINA) Bridging Blaze FMDFINA ReviewerДокумент24 страницы(FMDFINA) Bridging Blaze FMDFINA Reviewerseokyung2021Оценок пока нет

- Session 2 Chapter 3 Working With Financial StatementДокумент23 страницыSession 2 Chapter 3 Working With Financial StatementOkura TsukikoОценок пока нет

- CH5 - Understanding Balance SheetДокумент39 страницCH5 - Understanding Balance SheetStudent Sokha ChanchesdaОценок пока нет

- Bab 5 Analisis Laporan KeuanganДокумент54 страницыBab 5 Analisis Laporan KeuanganBenedict MihoyoОценок пока нет

- Lecture 6 - Working Capital Management 1Документ19 страницLecture 6 - Working Capital Management 1Gaba RieleОценок пока нет

- Unit-V Ratio Analysis: Financial Analysis and InterpretationДокумент21 страницаUnit-V Ratio Analysis: Financial Analysis and InterpretationAnusha EnigallaОценок пока нет

- Group 2 - Final Report On Working Capital ManagementДокумент47 страницGroup 2 - Final Report On Working Capital ManagementNaia SОценок пока нет

- Finance PDFДокумент136 страницFinance PDFjariyarasheedОценок пока нет

- Chapter 5 - Balance SheetДокумент37 страницChapter 5 - Balance SheethuguesОценок пока нет

- LECTURE 15 N 16 WORKING CAPITAL MANAGEMENTДокумент31 страницаLECTURE 15 N 16 WORKING CAPITAL MANAGEMENTVishal AmbadОценок пока нет

- Interpretation of Accounts.: Analysis of Financial Statements Ratio Analysis Cash Flow Statement FRS-1Документ7 страницInterpretation of Accounts.: Analysis of Financial Statements Ratio Analysis Cash Flow Statement FRS-1zulpukarovaОценок пока нет

- Topic Financial RatioДокумент14 страницTopic Financial RatioБота ОмароваОценок пока нет

- Due Diligence Considerations For Nonprofit Investment FiduciariesДокумент55 страницDue Diligence Considerations For Nonprofit Investment FiduciariesMichael YurkovichОценок пока нет

- Chapter 10 Interpretation of Financial Statements (S)Документ9 страницChapter 10 Interpretation of Financial Statements (S)khoagoku147Оценок пока нет

- Hero Honda Motors: Submitted To: Professor Seema DograДокумент19 страницHero Honda Motors: Submitted To: Professor Seema Dograpriyankagrawal7Оценок пока нет

- ACCY 111 Spring 2019 Week 12 Lecture Powerpoint PresentationДокумент33 страницыACCY 111 Spring 2019 Week 12 Lecture Powerpoint PresentationStephanie BuiОценок пока нет

- Unit-2 Working Capital ManagementДокумент47 страницUnit-2 Working Capital ManagementAbin VargheseОценок пока нет

- Understanding Financial Statements: Dr. Charles Suresh DavidДокумент19 страницUnderstanding Financial Statements: Dr. Charles Suresh DavidS.Abinith NarayananОценок пока нет

- Working Capital Management Working Capital Management (Unit-IV) (Unit-IV)Документ31 страницаWorking Capital Management Working Capital Management (Unit-IV) (Unit-IV)Muskan NarulaОценок пока нет

- Chapter 4 - FIN3004 - 2022Документ64 страницыChapter 4 - FIN3004 - 2022Lê Cẩm TúОценок пока нет

- Security Analysis and Portfolio Management: Rahul KumarДокумент28 страницSecurity Analysis and Portfolio Management: Rahul KumarDhruv MishraОценок пока нет

- Accounting For Managerial Decision Making: Working Capital EstimationДокумент32 страницыAccounting For Managerial Decision Making: Working Capital EstimationHaresh MbaОценок пока нет

- Lecture 01Документ50 страницLecture 01Anon sonОценок пока нет

- WCMДокумент36 страницWCMOsman Bin SaifОценок пока нет

- The Fundamentals of Alternative Investments: Laney Sanders, CFA Assistant Chief Investment Officer LasersДокумент47 страницThe Fundamentals of Alternative Investments: Laney Sanders, CFA Assistant Chief Investment Officer LasersRayane M Raba'aОценок пока нет

- Financial Management Lecture1Документ21 страницаFinancial Management Lecture1Sasha SGОценок пока нет

- NAT .FSA. E. C5. Analysis TechniquesДокумент33 страницыNAT .FSA. E. C5. Analysis TechniquesNguyễn Hoàng DươngОценок пока нет

- Financial Analysiis TenchniquesДокумент24 страницыFinancial Analysiis TenchniquesShreya GuptaОценок пока нет

- Chap 2 - Ratio AnalysisДокумент24 страницыChap 2 - Ratio AnalysisZubairBalochJatoi100% (1)

- Working Capital Management HeritageДокумент61 страницаWorking Capital Management Heritagedr btОценок пока нет

- Ratio Analysis: RatiosДокумент18 страницRatio Analysis: RatiosPhanishayan Kaniyar SampathОценок пока нет

- Unit 2 Ratio 2021Документ76 страницUnit 2 Ratio 2021Raju NagarОценок пока нет

- Fin QuestionsДокумент22 страницыFin Questionsvikki2point9Оценок пока нет

- Financial Statement AnalysisДокумент32 страницыFinancial Statement AnalysisRAKESH SINGHОценок пока нет

- Chapter 2 Balance SheetДокумент14 страницChapter 2 Balance SheetLuu Nhat MinhОценок пока нет

- Capital Structure PDFДокумент45 страницCapital Structure PDFperiОценок пока нет

- The Financial Plan Informal Risk Capital, Venture Capital, and Ratio Analysis - MSMEДокумент15 страницThe Financial Plan Informal Risk Capital, Venture Capital, and Ratio Analysis - MSMESupanut KaewumpaiОценок пока нет

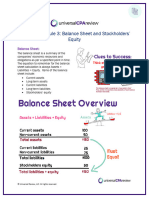

- Chapter 1 Module 3: Balance Sheet and Stockholders' EquityДокумент6 страницChapter 1 Module 3: Balance Sheet and Stockholders' Equityhmaz.roid91Оценок пока нет

- Comparison and Analysis ofДокумент25 страницComparison and Analysis ofGaurav JainОценок пока нет

- Lecture 4 - Bank's Assets and Liability ManagementДокумент16 страницLecture 4 - Bank's Assets and Liability ManagementLeyli MelikovaОценок пока нет

- Master in Management: Fundamentals of Finance - Session 1Документ446 страницMaster in Management: Fundamentals of Finance - Session 1Leonardo MercuriОценок пока нет

- Goals and Functions of Financial ManagementДокумент30 страницGoals and Functions of Financial ManagementskОценок пока нет

- Essentials of Financial Statement AnalysisДокумент30 страницEssentials of Financial Statement AnalysisChristina KarakatsaniОценок пока нет

- Ratio Analysis: Interpreting Financial StatementsДокумент7 страницRatio Analysis: Interpreting Financial StatementsKiran maruОценок пока нет

- ACCOUNTING PROCESS and CLASSIFICATIONДокумент26 страницACCOUNTING PROCESS and CLASSIFICATIONvdhanyamrajuОценок пока нет

- A Presentation On Credit AnalysisДокумент36 страницA Presentation On Credit Analysiszainahmedrajput224Оценок пока нет

- BA2088 - Lecture 3 Corporate Credit II - Corporate Credit Analysis Using Financial Statements & RatiosДокумент52 страницыBA2088 - Lecture 3 Corporate Credit II - Corporate Credit Analysis Using Financial Statements & RatioskeuqОценок пока нет

- Presentation On Working CapitalДокумент124 страницыPresentation On Working Capitalbeboliya100% (1)

- Unit 5Документ52 страницыUnit 5davidОценок пока нет

- Pertanyaan Pendadaran Dan Jawaban (Eng)Документ24 страницыPertanyaan Pendadaran Dan Jawaban (Eng)Siti NurfauziahОценок пока нет

- Ratio AnalysisДокумент28 страницRatio Analysispatel_bhoomi_1989Оценок пока нет

- Question Bank Test 1 With AnswersДокумент9 страницQuestion Bank Test 1 With AnswersUlugbek BayboboevОценок пока нет

- Authorisation LetterДокумент1 страницаAuthorisation LetterHuỳnh Hồng HanhОценок пока нет

- HNCD Business Unit Book Resource ListДокумент25 страницHNCD Business Unit Book Resource ListHuỳnh Hồng HanhОценок пока нет

- Sow Eap Sud11 June 2012Документ2 страницыSow Eap Sud11 June 2012tuibidienОценок пока нет

- Btec Progression and Recognition PDFДокумент17 страницBtec Progression and Recognition PDFHuỳnh Hồng HanhОценок пока нет

- Revised Maste Plan OC LCMДокумент11 страницRevised Maste Plan OC LCMHuỳnh Hồng HanhОценок пока нет

- Huynh Thi Hong Hanh MA 1 2.2 2.3Документ3 страницыHuynh Thi Hong Hanh MA 1 2.2 2.3Huỳnh Hồng HanhОценок пока нет

- Slide 4Документ43 страницыSlide 4Huỳnh Hồng HanhОценок пока нет

- ACNB ActivityДокумент1 страницаACNB ActivityHuỳnh Hồng HanhОценок пока нет

- Chuc Mung Giang SinhДокумент1 страницаChuc Mung Giang SinhHuỳnh Hồng HanhОценок пока нет

- Making Difficult Choices - Vietnam in TransitionДокумент104 страницыMaking Difficult Choices - Vietnam in TransitionIchiwayОценок пока нет

- Phrasal Verb ListДокумент10 страницPhrasal Verb ListIsrael Estevan BravoОценок пока нет

- Giao Trinh ExcelДокумент100 страницGiao Trinh ExcelHuỳnh Hồng HanhОценок пока нет

- Presentation 1Документ26 страницPresentation 1Huỳnh Hồng HanhОценок пока нет

- MF 2 Capital Budgeting DecisionsДокумент71 страницаMF 2 Capital Budgeting Decisionsarun yadavОценок пока нет

- Federal Ombudsman of Pakistan Complaints Resolution Mechanism For Overseas PakistanisДокумент41 страницаFederal Ombudsman of Pakistan Complaints Resolution Mechanism For Overseas PakistanisWaseem KhanОценок пока нет

- All-India rWnMYexДокумент89 страницAll-India rWnMYexketan kanameОценок пока нет

- 008 Supply and Delivery of Grocery ItemsДокумент6 страниц008 Supply and Delivery of Grocery Itemsaldrin pabilonaОценок пока нет

- 11-03-25 PRESS RELEASE: The Riddle of Citizens United V Federal Election Commission... The Missing February 22, 2010 Judgment...Документ2 страницы11-03-25 PRESS RELEASE: The Riddle of Citizens United V Federal Election Commission... The Missing February 22, 2010 Judgment...Human Rights Alert - NGO (RA)Оценок пока нет

- STAG-4 QBOX, QNEXT, STAG-300 QMAX - Manual - Ver1 - 7 - 8 (30-09-2016) - EN PDFДокумент63 страницыSTAG-4 QBOX, QNEXT, STAG-300 QMAX - Manual - Ver1 - 7 - 8 (30-09-2016) - EN PDFIonut Dacian MihalachiОценок пока нет

- Ode To The West Wind Text and AnalysisДокумент7 страницOde To The West Wind Text and AnalysisAbdullah HamzaОценок пока нет

- The Relationship Between Law and MoralityДокумент12 страницThe Relationship Between Law and MoralityAnthony JosephОценок пока нет

- Coaching Manual RTC 8Документ1 страницаCoaching Manual RTC 8You fitОценок пока нет

- Public Versus Private Education - A Comparative Case Study of A P PDFДокумент275 страницPublic Versus Private Education - A Comparative Case Study of A P PDFCindy DiotayОценок пока нет

- FAR REview. DinkieДокумент10 страницFAR REview. DinkieJollibee JollibeeeОценок пока нет

- AN6001-G16 Optical Line Terminal Equipment Product Overview Version AДокумент74 страницыAN6001-G16 Optical Line Terminal Equipment Product Overview Version AAdriano CostaОценок пока нет

- Ppivspiandpi G.R. No. 167715 November 17, 2010 Petitioner Respondents: Pfizer, Inc. and Pfizer (Phil.) Inc., TopicДокумент26 страницPpivspiandpi G.R. No. 167715 November 17, 2010 Petitioner Respondents: Pfizer, Inc. and Pfizer (Phil.) Inc., TopicMc Whin CobainОценок пока нет

- Chapter 12 Financial Management and Financial Objectives: Answer 1Документ9 страницChapter 12 Financial Management and Financial Objectives: Answer 1PmОценок пока нет

- SAi Sankata Nivarana StotraДокумент3 страницыSAi Sankata Nivarana Stotrageetai897Оценок пока нет

- Developmental PsychologyДокумент2 страницыDevelopmental PsychologyPatricia Xandra AurelioОценок пока нет

- Chapter 2 Demand (ECO415)Документ28 страницChapter 2 Demand (ECO415)hurin inaniОценок пока нет

- 5 L&D Challenges in 2024Документ7 страниц5 L&D Challenges in 2024vishuОценок пока нет

- 09 - Arithmetic Progressions - 16 PDFДокумент16 страниц09 - Arithmetic Progressions - 16 PDFShah RukhОценок пока нет

- Bahaa CVДокумент3 страницыBahaa CVbahaa ahmedОценок пока нет

- Composition PsychologyДокумент1 страницаComposition PsychologymiguelbragadiazОценок пока нет

- Pentagram Business PlanДокумент13 страницPentagram Business PlantroubledsoulОценок пока нет

- English Solution2 - Class 10 EnglishДокумент34 страницыEnglish Solution2 - Class 10 EnglishTaqi ShahОценок пока нет