Вам также может понравиться

- With Both Members and Non-MembersДокумент2 страницыWith Both Members and Non-MembersJing SagittariusОценок пока нет

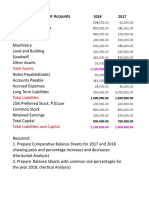

- Balance Sheet Accounts: Total AssetsДокумент4 страницыBalance Sheet Accounts: Total AssetsJing SagittariusОценок пока нет

- Philippine Financial Reporting FrameworkДокумент18 страницPhilippine Financial Reporting FrameworkJing SagittariusОценок пока нет

- Coop Pesos FormulaДокумент60 страницCoop Pesos FormulaJing Sagittarius80% (5)

- Cda Memorandum Circular 2015-09Документ32 страницыCda Memorandum Circular 2015-09Jing Sagittarius100% (2)

- VILLANUEVA-CASTRO COMMERCIAL LAW - New PDFДокумент40 страницVILLANUEVA-CASTRO COMMERCIAL LAW - New PDFJing Sagittarius100% (4)

- UP Civil Law Quizzer PDFДокумент116 страницUP Civil Law Quizzer PDFJing SagittariusОценок пока нет

- Ethics in Accounting For PrintingДокумент10 страницEthics in Accounting For PrintingJing SagittariusОценок пока нет

- Introduction To Statistical Thinking For Decision MakingДокумент13 страницIntroduction To Statistical Thinking For Decision MakingJing Sagittarius100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Renatus Bulletin 1.15.12Документ4 страницыRenatus Bulletin 1.15.12Donyetta JenkinsОценок пока нет

- Notes - MortgagesДокумент107 страницNotes - MortgagesadolfomoraisОценок пока нет

- Loans and AdvancesДокумент49 страницLoans and Advancesravi kangneОценок пока нет

- Rural BankingДокумент25 страницRural BankingAamit KumarОценок пока нет

- Saurav Aryal - M.E - Monetary Policy ReviewДокумент3 страницыSaurav Aryal - M.E - Monetary Policy Reviewaswin adhikariОценок пока нет

- Meaning of Business: Art. 1767, New Civil Code of The Philippines Sec.2 B.P. 68 or Corporation Code of The PhilippinesДокумент25 страницMeaning of Business: Art. 1767, New Civil Code of The Philippines Sec.2 B.P. 68 or Corporation Code of The PhilippinesAnali BarbonОценок пока нет

- Chapter Ii PDFДокумент30 страницChapter Ii PDFSharanuОценок пока нет

- Guide To Understanding Financial Statements PDFДокумент96 страницGuide To Understanding Financial Statements PDFyarokОценок пока нет

- Buy or Sell ANY Property in The 518 Area CodeДокумент16 страницBuy or Sell ANY Property in The 518 Area Code518list100% (3)

- Exclusive Right of Sale Listing Agreement: Florida Association of RealtorsДокумент5 страницExclusive Right of Sale Listing Agreement: Florida Association of RealtorsNorbert WaldenmayerОценок пока нет

- TutorialДокумент9 страницTutorialNaailah نائلة MaudarunОценок пока нет

- Schedule HДокумент26 страницSchedule HHaris SalОценок пока нет

- National Electrification Administration Vs CAДокумент2 страницыNational Electrification Administration Vs CAAnonymous 5MiN6I78I0Оценок пока нет

- Deficiency, Also Called A Working Capital DeficitДокумент66 страницDeficiency, Also Called A Working Capital DeficitBalakrishna ChakaliОценок пока нет

- Feven Engdawork Final PDFДокумент57 страницFeven Engdawork Final PDFNigussie BerhanuОценок пока нет

- Research Report On Loans and Advance SystemДокумент16 страницResearch Report On Loans and Advance SystemRavi DhudiyaОценок пока нет

- 099-Nidc vs. Aquino 163 Scra 153Документ12 страниц099-Nidc vs. Aquino 163 Scra 153wewОценок пока нет

- Student Loans FinalДокумент14 страницStudent Loans Finalapi-338640468Оценок пока нет

- RFBT FinalsДокумент7 страницRFBT FinalsSophia ManglicmotОценок пока нет

- Access To Finance of SMEs in Mauritius - Group DissertationДокумент23 страницыAccess To Finance of SMEs in Mauritius - Group Dissertationashairways100% (4)

- KIM Cum Appln Form Reliance Fixed Horizon Fund XXXX Series 15 PDFДокумент24 страницыKIM Cum Appln Form Reliance Fixed Horizon Fund XXXX Series 15 PDFarvind gaikwadОценок пока нет

- Empowering Women RMK WayДокумент74 страницыEmpowering Women RMK WayBiplav EvolvesОценок пока нет

- Petition For Temporary Restraining Order Against Bank of AmericaДокумент13 страницPetition For Temporary Restraining Order Against Bank of AmericaJanet and James100% (2)

- Chapter 3 Central BankДокумент34 страницыChapter 3 Central Bankandrei cajayonОценок пока нет

- Authority To Mortgage and Does Not Bind The Grantor Personally To Other Obligations Contracted by The Grantee."Документ1 страницаAuthority To Mortgage and Does Not Bind The Grantor Personally To Other Obligations Contracted by The Grantee."k santosОценок пока нет

- Standard Tender DocumentsДокумент115 страницStandard Tender DocumentsAnushke Hennayake100% (1)

- Case Digests-By AntsДокумент12 страницCase Digests-By AntsRose GeeОценок пока нет

- Meredith Corporation Employees Fund For Better Government - 6099 - DR2 - SummaryДокумент1 страницаMeredith Corporation Employees Fund For Better Government - 6099 - DR2 - SummaryZach EdwardsОценок пока нет

- 3 Republic Vs GrijaldoДокумент3 страницы3 Republic Vs GrijaldoHector Mayel MacapagalОценок пока нет

- Acme V CaДокумент2 страницыAcme V Cadot_rocksОценок пока нет