Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

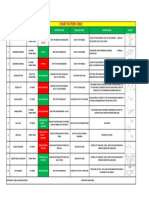

- Chart Pattern Table: S.No Types of Chart Pattern Found Trend Pattern Interpretation Measure Target Identification SymbolДокумент1 страницаChart Pattern Table: S.No Types of Chart Pattern Found Trend Pattern Interpretation Measure Target Identification SymbolGoogleuser googleОценок пока нет

- AmeranthДокумент42 страницыAmeranthSaucebg1Оценок пока нет

- FIN331-101 2010 Fall Exam2 AnswersДокумент7 страницFIN331-101 2010 Fall Exam2 Answersdaliaol100% (1)

- Forex Trading Strategies-Om Krishna UpretyДокумент70 страницForex Trading Strategies-Om Krishna UpretykosurugОценок пока нет

- Email Marketing and AutomationДокумент40 страницEmail Marketing and AutomationAMAN SОценок пока нет

- Sales Plan TemplateДокумент17 страницSales Plan TemplaterameshОценок пока нет

- This Study Resource Was: MPO FenêtresДокумент4 страницыThis Study Resource Was: MPO FenêtresRana HassanОценок пока нет

- Strategic Marketing Chapter 7Документ12 страницStrategic Marketing Chapter 7Äädï ShëïkhОценок пока нет

- Bic Product Life CycleДокумент4 страницыBic Product Life Cycleapi-505775092Оценок пока нет

- Venture Capital Funds and NBFCsДокумент5 страницVenture Capital Funds and NBFCsHari BalasubramanianОценок пока нет

- 1.1 Company Background: (CITATION Sho19 /L 1033)Документ14 страниц1.1 Company Background: (CITATION Sho19 /L 1033)Ena Popovska83% (6)

- Cournot OligopolyДокумент30 страницCournot OligopolyHarleen KaurОценок пока нет

- Mechanical EngineeringДокумент11 страницMechanical EngineeringUtkarsh ChoudharyОценок пока нет

- Earnings Momentum Composite - ModelDefinitionДокумент1 страницаEarnings Momentum Composite - ModelDefinitionUtkarsh ChoudharyОценок пока нет

- Capturing Factor Premia: September 2015Документ10 страницCapturing Factor Premia: September 2015Utkarsh ChoudharyОценок пока нет

- Multiple Regression Real Estate Example PDFДокумент6 страницMultiple Regression Real Estate Example PDFUtkarsh ChoudharyОценок пока нет

- ML Concepts: 1. Parametric Vs Non-Parametric Models:: Examples: Linear, Logistic, SVMДокумент34 страницыML Concepts: 1. Parametric Vs Non-Parametric Models:: Examples: Linear, Logistic, SVMUtkarsh ChoudharyОценок пока нет

- Assignment 6Документ14 страницAssignment 6Utkarsh ChoudharyОценок пока нет

- FMTZДокумент6 страницFMTZUtkarsh ChoudharyОценок пока нет

- RiskДокумент4 страницыRiskUtkarsh ChoudharyОценок пока нет

- Moshi Home Electricity Bill PDFДокумент2 страницыMoshi Home Electricity Bill PDFUtkarsh ChoudharyОценок пока нет

- Currency 2018 PDFДокумент3 страницыCurrency 2018 PDFUtkarsh ChoudharyОценок пока нет

- Subject: Permission To Students For Project WorkДокумент1 страницаSubject: Permission To Students For Project WorkUtkarsh ChoudharyОценок пока нет

- Riyaz Ahmed: Education DetailsДокумент2 страницыRiyaz Ahmed: Education DetailsUtkarsh ChoudharyОценок пока нет

- AdityaДокумент75 страницAdityaUtkarsh Choudhary0% (2)

- A Study of Organized Retail Outlet Marketing Practices: Ashwani Sethi, Parveen Kumar GargДокумент6 страницA Study of Organized Retail Outlet Marketing Practices: Ashwani Sethi, Parveen Kumar GarggsОценок пока нет

- TCW Prelim ReviewerДокумент6 страницTCW Prelim ReviewerCharlotteОценок пока нет

- Valuation of Joina City MallДокумент5 страницValuation of Joina City MallrudolfОценок пока нет

- Case Study 2 HW 4 BRICS CountriesДокумент6 страницCase Study 2 HW 4 BRICS CountriesmilagrosОценок пока нет

- Understanding Consumer Behavior: Hoyer - Macinnis - PietersДокумент12 страницUnderstanding Consumer Behavior: Hoyer - Macinnis - PietersAngelo P. NuevaОценок пока нет

- ACC 401 Week 7 QuizДокумент8 страницACC 401 Week 7 QuizEMLОценок пока нет

- The Contemporary World Week 1Документ25 страницThe Contemporary World Week 1Julius MacaballugОценок пока нет

- HO 10 Inventories IAS 2Документ7 страницHO 10 Inventories IAS 2rhailОценок пока нет

- BBA-302 Business Policy & Strategy (I. P.University)Документ39 страницBBA-302 Business Policy & Strategy (I. P.University)Dipesh TekchandaniОценок пока нет

- 1576847379CDM - Introduction To Digital Marketing Module 1 - Sessions 2Документ84 страницы1576847379CDM - Introduction To Digital Marketing Module 1 - Sessions 2withanage gayashaniОценок пока нет

- JURNAL Manajemen PemasaranДокумент11 страницJURNAL Manajemen PemasaranZakiya AudinaОценок пока нет

- Case Analysis (Cisco)Документ9 страницCase Analysis (Cisco)Faisal SunnyОценок пока нет

- SEBI Portfolio - Feb 2020Документ347 страницSEBI Portfolio - Feb 2020Tapan LahaОценок пока нет

- Sample MidTerm Multiple Choice Spring 2018Документ3 страницыSample MidTerm Multiple Choice Spring 2018Barbie LCОценок пока нет

- CVP Analysis and Break Even Point AnalysisДокумент16 страницCVP Analysis and Break Even Point AnalysisKirito Uzumaki100% (1)

- Great Eastern Shipping Company Limited (Case Study) : Submitted To:-Submitted ByДокумент6 страницGreat Eastern Shipping Company Limited (Case Study) : Submitted To:-Submitted ByAbhishek ChaurasiaОценок пока нет

- Chapter Twelve QuestionsДокумент3 страницыChapter Twelve QuestionsabguyОценок пока нет

- Compunding Machine PortfolioДокумент1 страницаCompunding Machine PortfolioManmohan ToshniwalОценок пока нет